Abstract

The paper entitled “Attempt to Extend the Knowledge of Decision Support Systems for Small and Medium-Sized Enterprises” [1] presented a prototype of an intelligent business forecasting system based on the real option approach to the prospective financial assessment of Small and Medium-Sized Enterprises (SME). This prototype integrates real options, financial knowledge, and predictive models. The content of the knowledge is focused on essential financial concepts and relationships connected with risk assessment, taking into consideration internal and external economic and financial information. In this project, the ontology is used to create the necessary financial knowledge model. The aim of this paper is to present the application of ontology in financial assessment based on real options approach to support financial assessment in an Early Warning System. In the paper, the process of creating a financial assessment ontology is described. The use created ontology in financial assessment based on the real options approach is discussed.

1 Introduction

Small and Medium-Sized Enterprises (SMEs) are forced to operate under the constraints and pressures of the rapidly changing and highly volatile market, which adds to the uncertainty of their everyday activities. Under such conditions, the manager can be seen as a future-oriented process of making informed decisions. From a manager’s viewpoint, making decisions in business is a process of identifying and selecting a course of action to solve a specific problem or to make good use of a business opportunity. The SME’s manager needs innovative methods combined with advanced financial analysis tools, which are required to correctly assess the economic situation of their company as well as the required investments.

In general, an enterprise works better on the competitive space if it tries to identify development opportunities and threats of disruption to its leading activity. This requires the implementation of prospective financial assessment in a SME. Examination of most of the future changes provides the signals (so-called weak signals) that facilitate anticipating their approach. However, the main hurdle is connected with choosing and properly identifying the relationships between them. Moreover, the moment in which they are identified constitutes critical information.

Most of SME managers are not skilled enough to understand and respond to threats coming from the business environment. Proper integration of signals coming from the environment with the performance achieved by an enterprise constitutes the basis for making good decisions involving corporate change. Managers who keep postponing making investment decisions expose their company to a risk of bankruptcy or a loss of continuity. This is especially important if such threats relate to a loss of competitive advantage due to technological backwardness. Failure to consider new investments could trigger off negative effects. These could provide the first signs of impending company bankruptcy since they are observable in the long-term perspective. The large variability of the environment demands companies’ flexible adjustment to prevailing external conditions.

In the literature, [1] the proposal of a prototype based on the real option approach that integrates financial knowledge, predictive models, and business reasoning to support financial assessment in Early Warning Systems was presented. In this project, it is assumed that financial knowledge is formally defined by the domain ontology, which is one of the commonly used methods of representing knowledge in information systems.

The aim of the paper is to present the application of ontology in financial assessment based on the real options approach to support financial assessment in an Early Warning System. The paper has been structured as follows. In the next section we describe Early Warning Systems in the context of financial assessment, the use of real options for the purposes of investment appraisal, and an ontological approach to the representation of financial and business knowledge. In section three, we present the proposal of smart EWS for SMEs and the process of creating a financial assessment ontology. Next, we present a case study analysis that refers to prospective financial assessment based on the real option approach. Finally, in the last section, some conclusions are drawn.

2 Theoretical Background

2.1 Critical Analysis of Early Warning Systems in the Context of Financial Analysis

The manager should analyze diverse information from external and internal sources (Fig. 1). Depending on this information, there is a number of possible scenarios, each of them associated with some opportunities and threats. When identifying threats, enterprises often have to analyze various potential investments that can minimize the risk to the company’s operations.

A number of possible scenarios of opportunities and threats depending on external and internal sources

Early warning is a process which allows an organization to consistently anticipate and address competitive threats. As far back as the early seventies, managers of firms started thinking about methods that would allow early identification of opportunities and threats present in their business environment. It led to the emergence of Early Warning Systems, which were to forewarn of approaching threats and opportunities as early as possible and explore their weak signals.

The first Early Warning Systems were focused on the performance indicators (KPIs), which are a business metric used to evaluate factors crucial to the success of an organization and to help an enterprise assess progress toward declared goals. An Early Warning System supports continuous monitoring, collecting, and processing of information needed by strategic management to effectively run the business, even in real time.

Regardless of the area of application, the main functions of Early Warning Systems do not change: it is early information about approaching threats and/or opportunities. This requires the development of solutions to help and enable warning signs. Many methods have been developed to analyze SME performance aimed at creating an Early Warning System [2]. Unfortunately, they are more often based on past data, and this, at present, is simply not enough. The essential requirement for an SME to survive in a competitive market is the development of mechanisms allowing the generation of revenues from core operations in the future. In planning future activities, companies’ managers emphasize the need to maintain existing customers. If this is not possible, attempts are made to search for new customers. It is also necessary to analyze competitive actions, which in the near future could lead to a significant decrease in market share.

The loss of the company’s competitive potential constitutes one of the most common threats to maintaining the forecasted sales revenues. This loss may occur due to various factors, including:

-

a drop in the quality of manufactured products or delivered services,

-

technological backwardness, which is the reason for the inability to meet customers’ expectations,

-

a low level of corporate capacity that significantly reduces the time necessary for delivery,

-

a lack of ability to cooperate with other entities in order to execute orders exceeding the production capacity.

Of course, the listed reasons do not represent all the problems related to the loss of companies’ ability to compete effectively. These are factors that cannot be registered by means of typical Early Warning Systems. Implementation of innovations and other changes in the structure of fixed assets should be considered as the first approach solution. The basic problem of conducting a development project is the lack of equity funds and a limited possibility of obtaining external financing. If the owners of a company are not able to increase equity, then debt financing is required. While taking bank loans or issuing bonds to finance innovations are possible solutions, they generate a high risk of insolvency. The managers should make multi-faceted analyses when making investment decisions. These analyses should take a contingent approach to financial forecasting and analysis in the long-term perspective.

One of the main weaknesses of existing Early Warning Systems is the lack of a formal representation of the knowledge and analytical models that take into consideration both internal and external information. Internal information refers to resource consumption, cost structure, etc., whereas external information takes into account market conditions, competitive actions, legal requirements, etc. In consequence, the reasoning tasks and computation are very limited.

The traditional Early Warning Systems are oriented towards identifying threats based mainly on the past information, and the design of such systems in an SME refers usually to internal reporting. Managers using simple Early Warning Systems receive various alerts, but they do not know which problems should be addressed first. Moreover, these systems do not indicate for managers which suggestions are to be implemented, hence managers have to rely solely on their managerial intuition. It is, therefore, necessary to extend the EWS functionality.

2.2 Using Real Options for Assessment Investment

The standard approach to investment appraisal is based on the discounted cash flow methodology, and NPV (Net Present Value) analysis in particular. This approach is currently insufficient mainly due to the high volatility of external factors affecting a company [3, 4]. The commonly used net present value criterion is currently considered as static mainly because it is calculated at a given moment and does not anticipate changes that may occur in the future. Moreover, while computing NPV, managers assume in advance that they know all factors affecting the investment’s effectiveness. As a result, the NPV criterion does not take into account the opportunity to react to new circumstances, such as [5]:

-

an unexpected collapse of the market, which leads to a reduction in the business size,

-

significant changes in prices, which may have a significant impact on the profitability of the project,

-

an exceptionally favourable situation that allows expanding the scope of activities.

Summarizing, the disadvantage of NPV is that it is based only on internal data and past data. Thus, the NPV calculated in this way is often referred to as passive or static.. The use of NPV for the assessment of investment project does not take into account external information, which may have both a negative (e.g. an unexpected collapse of the market, significant changes in prices) and a positive (e.g. an exceptionally favourable situation) impact on the implementation of an investment. Taking into account the limitations of the NPV criterion, the concept of real options should be applied.

The term “real option” was initially used in 1977 by Myers [6]. This concept was further developed by Dixit and Pindyck [7]. The term “real option” can be defined using an analogy to the financial option. Real option, therefore, means the right of its holder to buy or sell some underlying assets (basic instrument, which is usually an investment project) in specified sizes, at a fixed price and at a given time [8, p. 172]. Generally, it can be said that the real option is the right to modify an investment project in an enterprise [9, p. 269]. It helps managers create value, for if everything goes well, a project can be expanded; however, if the environment was to turn out to be unfavourable, then implementation of the project could be postponed. Projects that can be easily modified are much more valuable than those that do not provide for such flexibility. The more uncertain the future is and the more risk factors associated with the project, the more valuable is the flexibility of the project. Thus, real options can serve as a very helpful solution in making decisions on launching development projects as well as they are useful tools for managers looking for means to deal with their company’s financial problems.

Techniques based on the net present value are still necessary and valuable, hence they should not be underestimated in any case. However, real options allow for a deeper analysis of the investment appraisal issue and somehow expand the traditional methods due to the identification of various investment possibilities embedded in the investment projects. Jahanshahi et al. [10] argues the role that real options can play in an SME to increase market orientation and organizational learning, consequently providing a firm with the ability to both attain and sustain competitive advantage, particularly in a volatile environment.

The value of this flexibility is reflected in the option price (option premium); it increases if the probability of receiving new information increases and ability to bear risk increases. The value of this flexibility is the difference between the value of the investment project with the right of managers to modify the project embedded and the value of the project in the absence of managerial discretionary to modify the project. This relationship can be described as follows [11]:

where S-NPV – a strategic net present value, NPV – a standard (static, passive, direct) net present value, OV – an Option value.

The lack of flexibility is especially the main factor preventing managers from taking risks. They are often afraid of launching a new investment project and are not aware of the existence of a flexibility option. This is the reason why the development project is rejected. In addition, this kind of risk aversion may trigger off the company’s bankruptcy process. Power and Reid [12] test empirically whether real options logic applies to small firms implementing significant changes (e.g. in technology). Their research findings imply that strategic flexibility in investment decisions is necessary for good long-run performance of small companies.

The value of real options is very useful information for managers of small companies in the decision-making process related to undertaking an investment project. If a manager obtains information about the negative NPV of a project, then the project is usually rejected. Were a manager to adjust the static NPV with regard to the value of the real option, the final strategic value of the project could significantly change. This kind of financial projection prompts a manager to undertake the development project. Real options are treated as risk management instruments used to assess the financial risk of high-risk development projects as well as to influence the company’s ability to continue as a going concern in the future [13, 14].

The valuation of real options takes into account the scenario analysis prepared by managers before making the decision on the implementation of the development project. Very often, standard methods of investment appraisal do not take into account the possibilities that will occur during the implementation stage. Such omission may result in a loss of the ability to offer products with features similar to or exceeding those provided by competitors, and finally in the company’s bankruptcy.

The valuation of real options is a difficult task – very often impossible to be carried out by the manager of an SME. It should be noted that the value of real options is closely linked with high risk. A manager without advanced financial knowledge can increase the level of risk associated with running a business. Thus, it is necessary to use an information system that will guide the manager through all the risks associated with the investment project taking into account contingency factors.

2.3 Ontology of Financial and Business Knowledge

In the literature, we can find many definitions of ontology. A wide review of this issue is presented in [15, 16]. Most often, the term refers to the definition given by Gruber [17, p. 907], who describes it as “an explicit specification of a conceptualization”. Therefore, ontology is a model that defines formally the concepts of a specific area and the semantic relations between them. Constructing ontology always denotes analysis and organizing knowledge concerning a specific field noted in a formalized structure.

In general, the ontology is used to create the necessary knowledge models for defining functionalities in analytical tools. Using ontologies supporting an information search in an information system may help to reduce the following weaknesses of management information systems: (1) a lack of support in defining business rules for getting proactive information and support with respect to consulting in the process of decision making, and (2) a lack of a semantic layer describing relations between different economic concepts [18]. Ontology can be used to create the necessary knowledge (especially financial knowledge) models in analytical tools. The created financial ontologies, which contain experts’ knowledge, may serve as a strong support for decision makers in SMEs. The domain knowledge about relations between economic and financial ratios will make the analysis and interpretation of contextual connections easier. This is very important in the case of SMEs, where a company does not employ experts in economic-financial analysis, and using external consulting is too costly. Reproducing knowledge with the use of visualization of semantic network contributes inter alia to a better understanding of economic concepts and the interpretation of specific economic and financial indicators.

Ontology can be presented by visualization of a semantic network, which is a multi-faceted, interactive presentation tool, also allowing interactive visual searches for information [19]. This solution can contribute to a better understanding of economic concepts and the interpretation of specific economic and financial indicators, among other things. In this approach, special attention is paid to the role of the visualization of a semantic network which is not only a tool for presenting data but also one providing an interface allowing interactive visual information searching [20, 21].

In the relevant literature, many research projects show that creating an ontology of economic and financial indicators is advantageous in decision making [22,23,24,25,26].

3 Research Methodology

3.1 Proposal of Smart Early Warning Systems

A proposal of a smart Early Warning System for SMEs is presented in the paper [1]. This solution integrates financial knowledge, predictive models, and business reasoning to support the financial assessment of an enterprise and assess the profitability of an investment project. This EWS has introduced several new solutions. Figure 2 presents a functional schema of a smart EWS. There are four important elements:

-

using real options to calculate strategic NPV,

-

analysis of internal and external information,

-

using ontology of business knowledge,

-

integration of financial knowledge and predictive models.

(Source: [1])

Functional schema of a smart EWS

The presented smart EWS can facilitate automated analysis of information available in financial databases and external data. In this solution, real options are used to calculate the strategic net present value. The valuation of real options is a difficult task and very often impossible to be carried out by the manager of an SME, so financial knowledge is formally defined by the domain ontology. This proposal of a smart ESM is based on the introduction of financial ontology, containing internal and external variables related to real options. A manager can browse the hierarchy of concepts, relationships, and annotations. They can also define conditions such as positive and negative effects of decision process execution.

This smart EWS includes also extended analytical methods, which aims at integrating data from internal reporting with external information. The internal and external information and information about real options is interpreted by the decision rules, for example [1]:

where ® denotes a specific relationship between the values of fi and the threshold.

The system processes selected information from financial reports and the business environment, subsequently forecasting a company’s economic and financial situation. In a situation of a negative forecast, in addition to warning messages, it indicates the possibility of using the real options that would allow a manager to exit a critical situation. The financial ontology not only helps identify the concepts and relationships between them, but it also facilitates the interpretation of the current and future situations of the company.

3.2 Creating Financial Assessment Ontology

In the literature, many different approaches to the design of an ontology can be found (a wide review of the issue is presented in: [15]). There are many methods describing the methods of creating an ontology for information systems [27,28,29]. But so far there is no single approach accepted by all. The ontology of this study was built using the methodology presented in [18, 30]. This study has been carried out in the five stages:

-

(1)

Definition of the goals, scope, and constraints of the created ontology. While creating an ontology, assumptions about the created model of knowledge have to be provided. That requires an answer to the question: what will the created ontology be used for? For our purpose, an ontological framework was designed to represent the area of knowledge of financial assessment. This stage involves also checking and answering the question: can existing and available ontologies be used in entirety or in fragments in the developed ontology? We analyzed the created ontologies of business knowledge which can be used partially or in entirety. In our research on financial analysis in SMEs, we created an ontology of the part of financial analysis, which contains basic financial indicators [31]. The results of this stage are (1) identification of possible fragments of the created ontology to be used in our study and (2) a definition of the extent of developed ontology and its required level of detail.

-

(2)

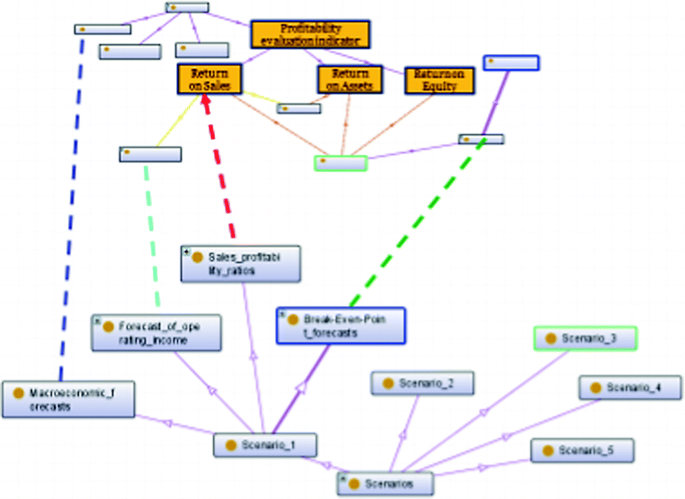

Conceptualization of the ontology. This is the most important stage of creating an ontology of business knowledge because it is the most important stage in creating a model based on ontology. It includes the identification of all concepts, definition of classes and their hierarchic structures, modelling relations, identification of instances, specification of axioms, and rules of reasoning. The result of this stage is a constructed model of an ontology of the defined field of business knowledge with respect to financial assessment (Fig. 3).

Fig. 3.

The example of the part of the created ontology

-

(3)

Verification of the ontology’s correctness by experts. The aim of this stage is to answer the question: is it necessary to modify the ontology model developed for the chosen part of business knowledge? The created ontology was verified in the following way: (1) a formal verification of the specified ontology (e.g. incorrect relations were indicated) and (2) a content verification (e.g. correctness of taxonomic concepts, and correctness of relational dependencies between concepts).

-

(4)

Encoding the ontology is described in the formal language or editor of ontology. We encoded the ontology using Protégé, which is a free, open-source platform (http://protege.stanford.edu/), which can be extended with many plug-ins for ontology visualization (http://protegewiki.stanford.edu/wiki/Visualization).

-

(5)

Validation and evaluation of the built ontology. In this stage, the encoded ontology is checked to ensure that it meets the needs of the users (e.g. the managers). Validation is carried out in two areas. Firstly, validation of usefulness and correctness of the created ontology is carried out by experts. Secondly, validation of predefined use cases is carried out. That requires an answer to the questions: (1) will the created ontology be useful for the users (the managers) who will use it? and (2) is it necessary to modify the encoded ontology for the selected part of business knowledge? We prepared use cases of financial assessment scenarios and validated the created ontology. In our study, evaluation of semantic network visualization as they pertained to contextual dependencies was conducted using the OntoGraf module in the Protégé 4.1 program.

The presented process of the created ontology is characterized by iterative design. The iterative design of ontology is important because the created ontology should be useful to the managers. The use of ontologies within analytical tools can help you solve the following problem: support in defining business rules in order to obtain proactive information and advice in the decision-making process. The use of the created ontology in financial assessment based on the real options approach to support financial assessment in EWS will be discussed in the next section.

4 Case Study

To illustrate the need for real option valuation, we present the case of a project that would be rejected on the basis of traditional analytical methods. Based on the valuation of flexible option to expand, we have shown that to avoid going bankrupt, the management should choose to implement the project.

Assumptions of the case study [see also: 1]:

-

managers of a manufacturing company producing water heaters and wood fireplaces, while preparing sales forecasts, identify a significant problem with the company’s ability to continue its operations,

-

managers, based on their expertise and experience, foresee that if they decide to abandon development projects, the company will lose the ability to continue its operations within 5–7 years,

-

when planning innovations in the enterprise, a new design of a fully ecological cogeneration fireplace meeting the most stringent environmental standards has been developed,

-

the forecasted product cost suggests a high selling price that does not allow launching the project,

-

it is necessary to implement changes in production technology which would make it possible to reduce costs and offer a lower price of the new product; however, the NPV analysis indicates that the project would still be unprofitable.

To detail the case study, let us examine the data in Table 1. The input data needed to estimate the NPV values presented in this table were prepared with the assumption of homogeneous ranks for each presented piece of information. The prepared EWS prototype allows the manager to assign any rank to each source of information. However, less experienced managers can use the hint embedded in the prototype, which suggests default solutions.

The information in Table 1 is divided into three parts related to the project’s life cycle: investment, operation, and liquidation. Each of these phases requires different data needed to conduct investment appraisal. Individual items of costs of revenues and cash flows may occur only in a given phase, therefore some cells of the table are empty. Sales revenue and cash flow balances in the operating phase remain at the same level in the period 2025–2027, as the company, without taking advantage of embedded real options, is not in a position to develop.

Based on the above assumptions and data, managers should not make any decision to implement any development project in the company. The data presented in the table clearly show that the analyzed development project is not profitable, as the NPV is negative and equals – 2.2 million PLN. The financial prospect of this company is bad. However, the lack of profitability has been projected based on traditional measures. Relying on the additional external information, a manager may apply the flexibility option, and all of a sudden the project becomes profitable.

However, it is clear that the rejection of the investment may lead to the company’s bankruptcy. It is necessary to apply advanced analyses that take into account the option of developing business in the future. The valuation of such an option is based on the following premises:

-

high social pressure on promoting environmentally-friendly solutions,

-

anticipated changes in law indicate that in the future it will not be possible to build houses meeting high ecological standards without the modern heaters and fireplaces,

-

the design of the new technological solution allows its use in other products because, along with favourable external conditions and small expenditures, it will be possible to expand the range of new environmentally-friendly products,

-

governmental research agencies plan to subsidize new solutions that meet high environmental standards in the future,

-

within the national entrepreneurship development strategy, there are various aid programs for innovative entrepreneurs.

At this moment, the manager can use the module of the created ontology in the smart EWS. Figure 4 presents important concepts in rectangles for the analysis of the strategic NPV. There are two panels on the screenshot. The panel to the left shows taxonomic relations, while the one to the right allows for visualization of taxonomic and semantic relations between defined concepts (semantic network visualization). The presented part of the ontology shows that Strategic NPV depends on standard NPV and Real options, which contain Positive real options and Negative real options. Positive real options increase Strategic NPV, while negative real options decrease Strategic NPV. Instances of positive and negative real options are External information (for example Industry reports on the sales and Environmental fee). This part of the ontology shows to the manager that if they want to calculate Strategic NPV, they should estimate Real options. The manager can see that they should analyze External information affecting the calculation of the positive and negative values of real options. The manager can add, modify, as well as retrieve concepts related to the problem at hand.

(Source: own elaboration using Protégé editor)

An example of visualization of a semantic network of Strategic NPV

The above market conditions based on external information serve as the basis for valuation of the flexible development option, which extends the traditional investment appraisal analysis. The sales forecast of the company indicates the clear signal of significant operating losses. Among the most important causes of the significant decrease in the ROS ratio were: a declining demand for the company’s products and high operating leverage, i.e. a significant share of fixed costs in the total cost of production.

Thus, in order to survive, it is necessary to implement new products as well as to modify the current manufacturing technology. This is why the manager requests the profitability analysis of the investment project. The basis for this analysis is future sales revenues from new products and funds allocated for the acquisition of new technologies. The future cash flows obviously should be discounted to the present, taking into account the time value of money. The net present value is negative, thus the static analysis indicates that the project implementation is not profitable and the project should not be undertaken.

The Early Warning System based on the created ontology and in-depth analysis of the extended (strategic) version of NPV estimated using stochastic models [32] suggests extending the decision-making context. This extension takes into account the valuation of the flexibility option. For the purposes of the valuation of flexibility options, the system uses the following external information that involves the following:

-

an opportunity to obtain additional external financing for an investment project involving the implementation of low-carbon technology (the amount of up to PLN 200,000) dedicated for Polish enterprises from the SME sector,

-

a possibility of financing innovative environmentally-friendly technologies with amounts of up to 80% of eligible costs for enterprises from the SME sector,

-

a possibility of receiving a tax relief for SME enterprises investing in reconstruction and implementation of environmentally-friendly production solutions.

The ontology built into the EWS (Fig. 2) explains to the manager the basic concepts and problems associated with the sales profitability. The ontology also presents the knowledge that combines the profitability issue with the investment project appraisal. Information transformed by the system indicates the possibility of acomprehensive profitability analysis. The system triggers off a signal that informs the manager of the option of analyzing the strategic NPV. This signal contains the suggestion that it is necessary to obtain additional information. After processing the available data for the purposes of the analyzed company, the system returns the value of the flexibility option that exceeds the negative NPV. In the analyzed company, the situation allows initiating preparatory activities to launch the project.

5 Conclusion and Future Works

The main objective of the paper was to present the application of ontology in smart Early Warning Systems. The created ontology contains knowledge about internal and external variables related to real options. The knowledge contained in the ontology explains to the manager the essence of valuating the flexibility option. The ontology also indicates the necessary external data that would make valuation possible. A manager who does not have detailed financial knowledge – is able to learn – thanks to the ontology – the relation between the flexibility option and the investment project profitability. The system presents a set of fundamental information needed to evaluate the flexibility option, but the information should be verified by the manager.

The example discussed in the paper is based on real data extracted from a small company. A risk of bankruptcy could be avoided by making decisions based on intelligent in-depth analysis of external information combined with the analysis of financial situation that allows the implementation of corrective solutions. From a financial perspective, the presented case study supports the conclusion that the decision to undertake any investment cannot be based solely on the estimation of standard NPV. It also requires an analysis of various external factors determining the decision-making process. Managers of SMEs may take advantage of the smart EWS that integrates the created ontology of financial knowledge and predictive models. Therefore, the system provides knowledge not only on the required internal information from various reports but also from external information (which consists in weak signals). The proposed ontology seems to be a promising extension to Early Warning Systems. It not only improves the quality of analysis but also enhances the managerial ability to better understand relations between financial data (internal information) and various factors affecting the development of SMEs (external information).

The presented process of designing an ontology in this paper requires further work verifying its usefulness in creating an ontology of financial knowledge. The use of an ontology of business knowledge seems to be a promising extension of EWS for SMEs. It not only should improve the efficiency of analysis, but also increase SMEs managers’ capacity of understanding economic and financial data.

Further work should be focused on a global process-oriented approach to financial assessment, which will not be possible without large databases of real case studies and the use of knowledge possessed by experienced managers and financial analysts. For a company, the multidisciplinary approach to developing the prospective analysis in an Early Warning System could contribute to the attainment of a competitive advantage and increasing its financial stability.

References

Nita, B., Oleksyk, P., Korczak, J., Dudycz, H.: Prospective financial assessment based on real options in small and medium-sized company. In: Ganzha, M., Maciaszek, L., Paprzycki, M. (eds.) Proceedings of the 2018 Federated Conference on Computer Science and Information Systems, Annals of Computer Science and Information Systems, vol. 15, pp. 789–793 (2018). https://doi.org/10.15439/2018f161

Koyuncugil, A.S., Ozgulbas, N. (eds.) Surveillance Technologies and Early Warning Systems: Data Mining Applications for Risk Detection. IGI Global (2009). https://doi.org/10.4018/978-1-61692-865-0

Adelaja, T.: Capital Budgeting: Capital Investment Decision Paperback. CreateSpace Independent Publishing Platform (2016)

Götze, U., Northcott, D., Schuster, P.: Investment Appraisal: Methods and Models. Springer, Heidelberg (2015). https://doi.org/10.1007/978-3-662-45851-8

Damodaran, A.: The promise of real option. In: Stern, J.M., Chew, D.H. (eds.) The Revolution in Corporate Finance. Blackwell Publishing (2003). https://doi.org/10.1111/j.1745-6622.2000.tb00052.x

Myers, S.C.: Determinants of capital borrowing. J. Financ. Econ. 5, 147–175 (1977)

Dixit, A., Pindyck, R.S.: Investment Under Uncertainty. Princeton University Press, Princeton (1994)

Nita, B.: Metody wyceny i kształtowania wartości przedsiębiorstwa [Methods of Corporate Valuation and Value-Based Management]. PWE, Warszawa (2007)

Brealey, R.A., Myers, S.C.: Principles of Corporate Finance. Mc-Graw Hill, New York City (2003)

Jahanshahi, A., Nawaser, K., Eizi, N., Etemadi, M.: The role of real options thinking in achieving sustainable competitive advantage for SMEs. Global Bus. Organ. Excell. 35(1), 35–44 (2015). https://doi.org/10.1002/joe.21643

Trigeorgis, L.: Real Options. Managerial Flexibility and Strategy in Resource Allocation. The MIT Press, Cambridge (1998)

Power, B., Reid, G.: Organisational change and performance in long-lived small firms: a real options approach. Eur. J. Finance 19(7/8), 791–809 (2013). https://doi.org/10.1080/1351847X.2012.670124

Benaroch, M., Lichtenstein, Y., Robinson, K.: Real options in information technology risk management: an empirical validation of risk-option relationships. MIS Q. 30(40), 827–864 (2006)

Favato, G., Vecchiato, R.: Embedding real options in scenario planning: a new methodological approach. Technol. Forecast. Soc. Chang. 124(C), 135–149 (2017). https://doi.org/10.1016/j.techfore.2016.05.016

Smith, B.: Ontology and information systems (2010). http://ontology.buffalo.edu/ontology%28PIC%29.pdf

Arp, R., Smith, B., Spear, A.D.: Building Ontologies with Basic Formal Ontology. MIT Press, Cambridge (2015)

Gruber, T.R.: Toward principles for the design of ontologies used for knowledge sharing. Technical report KSL, Knowledge Systems Laboratory, Stanford University (1993). http://tomgruber.org/writing/onto-design.pdf

Dudycz, H., Korczak, J.: Conceptual design of financial ontology. In: Ganzha, M., Maciaszek, L., Paprzycki, M. (eds.) Proceedings of the 2016 Federated Conference on Computer Science and Information Systems. Annals of Computer Science and Information Systems, vol. 5, pp. 1505–1511 (2015). https://doi.org/10.15439/978-83-60810-66-8

Ertek, G., Tokdemir, G., Sevinç, M., Tunç, M.M.: New knowledge in strategic management through visually mining semantic networks. Inf. Syst. Front. 19, 165–185 (2015). https://doi.org/10.1007/s10796-015-9591-0

Grand, B.L., Soto, M.: Topic maps, RDF graphs, and ontologies visualization. In: Geroimenko, V., Chen, C. (eds.) Visualizing the Semantic Web. XML-Based Internet and Information Visualization, pp. 59–79. Springer, London (2010). https://doi.org/10.1007/1-84628-290-X_4

Wienhofen, L.W.M.: Using graphically represented ontologies for searching content on the semantic web. In: Geroimenko, V., Chen, C. (eds.) Visualizing the Semantic Web. XML-Based Internet and Information Visualization, pp. 137–153. Springer, London (2010). https://doi.org/10.1007/1-84628-290-x

Aruldoss, M., Maladhy, D., Venkatesan, V.P.: A framework for business intelligence application using ontological classification. Int. J. Eng. Sci. Technol. 3(2), 1213–1221 (2011)

Cheng, A., Lu, Y.-C., Sheu, C.: An ontology-based business intelligence application in financial knowledge management system. Expert Syst. Appl. 36(2), part 2, 3614–3622 (2009). https://doi.org/10.1016/j.eswa.2008.02.047

Korczak, J., Dudycz, H., Dyczkowski, M.: Design of financial knowledge in dashboard for SME managers. In: Ganzha, M., Maciaszek, L., Paprzycki, M. (eds.) Proceedings of the 2013 Federated Conference on Computer Science and Information Systems. Annals of Computer Science and Information Systems, vol. 1, pp. 1111–1118 (2013)

Korczak, J., Dudycz, H., Nita, B., Oleksyk, P., Kaźmierczak, A.: Extension of intelligence of decision support systems: manager perspective. In: Ziemba, E. (ed.) AITM/ISM-2016. LNBIP, vol. 277, pp. 35–48. Springer, Cham (2017). https://doi.org/10.1007/978-3-319-53076-5_3

Neumayr, B., Schrefl, M., Linner, K.: Semantic cockpit: an ontology-driven, interactive business intelligence tool for comparative data analysis. In: De Troyer, O., Bauzer Medeiros, C., Billen, R., Hallot, P., Simitsis, A., Van Mingroot, H. (eds.) ER 2011. LNCS, vol. 6999, pp. 55–64. Springer, Heidelberg (2011). https://doi.org/10.1007/978-3-642-24574-9_9

Dudycz, H.: Mapa pojęć jako wizualna reprezentacja wiedzy [The topic map as a visual representation of economic knowledge] (in Polish). Wydawnictwo Uniwersytetu Ekonomicznego we Wrocławiu, Wrocław (2013)

Gomez-Perez, A., Corcho, O., Fernandez-Lopez, M.: Ontological Engineering: with Examples from the Areas of Knowledge Management, e-Commerce and the Semantic Web. Springer, London (2004). https://doi.org/10.1007/b97353

Noy, F.N., McGuinness, D.L.: Ontology development 101: a guide to creating your first ontology (2005). http://www.ksl.stanford.edu/people/dlm/papers/ontology101/ontology101-noy-mcguinness.html

Dudycz, H., Korczak, J.: Process of ontology design for business intelligence system. In: Ziemba, E. (ed.) Information Technology for Management. LNBIP, vol. 243, pp. 17–28. Springer, Cham (2016). https://doi.org/10.1007/978-3-319-30528-8_2

Korczak, J., Dudycz, H., Nita, B., Oleksyk, P.: Semantic approach to financial knowledge specification - case of emergency policy workflow. In: Ziemba, E. (ed.) AITM/ISM-2017. LNBIP, vol. 311, pp. 24–40. Springer, Cham (2018). https://doi.org/10.1007/978-3-319-77721-4_2

Schulmerich, M.: Real Options Valuation: The Importance of Interest Rate Modelling in Theory and Practice. Springer, Heidelberg (2010). https://doi.org/10.1007/978-3-642-12662-8

Acknowledgement

The authors would like to thank Jerzy Korczak from the International University of Logistics and Transport, Wrocław, Poland, for his significant contribution to the development of the concept and prototype of the smart EWS as well as cooperation on the development of methods for automating inference rules.

Author information

Authors and Affiliations

Corresponding author

Editor information

Editors and Affiliations

Rights and permissions

Copyright information

© 2019 Springer Nature Switzerland AG

About this paper

Cite this paper

Dudycz, H., Nita, B., Oleksyk, P. (2019). Application of Ontology in Financial Assessment Based on Real Options in Small and Medium-Sized Companies. In: Ziemba, E. (eds) Information Technology for Management: Emerging Research and Applications. AITM ISM 2018 2018. Lecture Notes in Business Information Processing, vol 346. Springer, Cham. https://doi.org/10.1007/978-3-030-15154-6_2

Download citation

DOI: https://doi.org/10.1007/978-3-030-15154-6_2

Published:

Publisher Name: Springer, Cham

Print ISBN: 978-3-030-15153-9

Online ISBN: 978-3-030-15154-6

eBook Packages: Computer ScienceComputer Science (R0)