Abstract

As the microloan becomes popular with the advance of information technology, the assessment of credit risk and understanding borrowers become crucial. However, without antithetical individuals, the prediction of loan probability and risk control cannot be so accurate. As an important consumption group in current commercial society, college students usually don’t have enough disposable income thus very likely become active lenders in microloan platforms. For microloan platforms, a vital question is how to distinguish the individuals who use the loans for the right purposes. In this study, we combine the student loan data from a microloan platform with student daily consumption data recorded by a campus e-card system to examine the change of consumption behavior for those students who borrowed money from the microloan platform. Our study finds that students with loan do have distinct consumption patterns for both long and short terms. Furthermore, by applying a difference-in-difference regression method, we find significant increases in both consumption frequency and money after students borrow money from the microloan platform for both long and short terms. Our research enriches the literature on microloan in the context of college students as consumers.

You have full access to this open access chapter, Download conference paper PDF

Similar content being viewed by others

Keywords

1 Introduction

Information technology provides a convenient channel for people who have microloan demand to seek loans. Microloan platforms (Lending club, Prosper et al.) are thus becoming more and more popular [12]. For microlenders, the borrowers’ credit risk assessment and understanding borrowers’ behavior are crucial in lending procedure [16]. Prior research often uses the borrowers’ demographic characteristics, social capital and credit history to assess the risk (e.g. [10, 16]). However, lacking of antithetical individuals, who have the similar characteristics (e.g. sex, age, enroll year et al.) as the borrower but don’t borrow money from the microloan platform, microlenders cannot obtain the unique characteristics of borrowers compared with non-borrowers and can hardly recognize who on earth need to borrow money.

Among the huge borrower group, young people who completed high school are “special” potential consumption group. They usually become to decide what to purchase by themselves without intervention from parents after they enter colleges. In recent years, college students’ consumption view has also upgraded. According to a report from iResearch, Chinese college students spend approximately 452.4 billion RMB in 2016Footnote 1. On the one hand, they begin to form their own consumption view out from the childhood. On the other hand, they don’t have enough disposable income to satisfy their demand and don’t have the qualification to apply credit card. Under such situation, most students are hesitated to seek help from family members or borrow money from friends due to fear of getting blame and feeling of embarrassment. However, because of lacking stable source of income and poor consumption plan, the limited money may not afford the purchasing need of some college students. Thus young people are very likely to seek money from microloan platforms. Meanwhile, the development of microloan business provides a loan channel for college students who are in short of money. Thus they are very likely become a type of active lenders in microloan platform. For microloan platform, how to distinguish the students who use the loan for the right (low-risk) purpose is a vital question. In many instances, college students are not familiar with the loan procedure, and have less responsibility and weak awareness of risk and information security, which leads to negative events such as high default rate, unduly debt collection and information theft. Therefore, how to trace students’ subsequent consumption behavior after borrowing money is an important question for college administrators and microloan lenders. For college administrators, how to distinguish the students who have need for financial support and give them some financial support to help them make through the financial difficulties and finish college education is a main concern.

Nevertheless, there is little literature on risk evaluation with daily consumption data and we need find valuable evaluation indicators. Since the digital campus has already been well-developed, almost all aspect of college life can be paid by campus e-card. Thus, our research idea is based on the student daily consumption behavior data acquired from the e-card records, mining features of high-risk borrowers. Furthermore, by investigating on comparing the behaviors before and after obtaining money from microlenders, we can help academia and industry better understand borrowers’ behaviors and trace their risk after loan. Moreover, the microlenders can recognize the low-risk financial demand borrowers and provide personalized service. The relevant regulators such as financial governors and college administrators can also recognize the group with real financial demand, thus provide financial support to them and improve the social well-being.

The paper is organized as follows: First, the relevant literature on microloan and e-card is reviewed. Next, we introduce our data set and variables. The research method and results are presented in Sect. 4. Finally, we summarize the conclusion and implications of our research.

2 Literature Review

The literature related to our research includes two streams: microloan and campus e-card.

At individual level, the literature on microloan is very rich. The literature can be approximately categorized into three types. One is about user credit and risk evaluation and prediction [1, 2, 8, 10, 13, 14, 16]. These studies contribute to testing the influential factors related to borrowers’ repayment risk, such as loan characteristics, borrower characteristics, credit history, and social capitals. The second strand of literatures analyzed microloan user behavior (e.g. [3, 5, 8, 11, 15]). These studies focus on users’ behavioral patterns such as herding, and reveal the existence of home bias. The third group of literature explored the factors related to successful loans, interest rates, as well as the investment patterns of lenders, etc. [4, 6, 7, 15, 21]. These studies face a common dilemma that their research factors are static and from the borrowers’ self-reported information, thus can lead to potential endogeneity problem.

To the best of our knowledge, the literature on application of campus e-card data is scarce. In the limited literature, a few papers employ e-card data to investigate the factors that may influence students’ study performance [17, 19], and they find that students’ breakfast frequency, consumption habit are strongly correlated with their study performance. Another stream of studies investigates student behavioral patterns such as dinning frequency, dinning money, shopping money and frequent canteen windows with data mining method such as clustering [9, 18]. Fu et al. [20] use the MapReduce method to visualize the student consumption behavior among different season and grade in the Hadoop framework. However, the extant research does not: (1) make full use of the e-card consumption data, (2) have a deep investigation in the data, (3) associate the data to the student financial status, and (4) allocate students with economic difficulties.

In summary, the prior literature has not empirically investigated the factors revealing why individuals borrow money from microloan with second-hand consumption flow data; and there is a gap in literature on tracing and comparing borrowers’ purchasing behaviors before and after loan attainment. Campus e-card data of college students can trace the daily consumption activities and thus provide good opportunities to fill in the above research gaps.

3 Data Description

Our dataset contains two parts: loan data from the online lending platform and campus e-card consumption data. The loan data is from a Chinese microloan platform whose business mainly targets college students. We obtained 520 student borrowers from a unique school in China. The school has both college and university students according to their scores in higher-education entrance examination. All loans were applied from June 2014 to February 2015, and are the first time for these students to experience in the platform. The dataset includes students’ basic information such as whether he/she is an undergraduate student, gender, age, study major, etc. We also have borrowers’ self-reported loan purpose, and we categorize them into two types: daily consumption and emergency consumption. Loan information includes interest rate, loan term and loan size. Detailed repayment records are also included in the loan data. The descriptive statistic of loan data is shown as Table 1.

We obtained campus e-card consumption data from the same school of the 520 students who borrowed money from the microloan platform. With the agreement of students and help of school managers, we totally got 12,282 students’ over 40 million consumption data records from 2009 to 2017. The dataset contains student basic information such as gender, age, year of attendance, hometown, and very detailed consumption flow data such as amount, time and consumption purpose (i.e., consumption in canteen, shopping in stores, and recharge the e-card). Notably, the platform doesn’t have the information on students’ daily consumption and do not use them in risk assessment, so there is no sample selection bias from the platform employers. We match the 520 sample students’ loan information with their campus e-card records by phone numbers with the help of a third-party e-campus service providers. We do not have any information that could identify the authentic identity of every student in our dataset.

Without the students who don’t borrow money from the platform, we can’t control the unobservable heterogeneity in student characteristics. Furthermore, randomly picking unborrowed student can’t make sure that the borrowed group and unborrowed group are comparable. Thus, we use propensity score matching (PSM) method to find the antithetical individuals. First, we use the logit regression method to find the significant variables that may influence the two group, the logit regression result is shown in Table 2. Then we use these variables to match the two group in the full sample and compare the mean difference of these variables between the two groups. We get a perfect match for each student who borrow money from microlenders.

After PSM, we had 1,040 students (520 borrowers and 520 non borrowers) with 1,572,803 e-card consumption records. Then we code the student dinning behavior, shopping behavior and recharge behavior for both long and short terms. The long terms include a year before borrowing and borrowing date to repayment date. The short terms include a month before borrowing money and a month after borrowing. For the long-term variables, we also code the regularity using the corresponding standard deviation of each student. By comparing the mean value of each variable, we preliminarily find that students without loan have more consumption frequency and money than students with loan on average.

4 Method and Results

For the first research question: what kind of student will borrow money from the microloan platform, we use logit regression to find the answer. However, since there are endogeneity problems because the students who borrow money may have special consumption behavior pattern, which will lead the causality relationship unreliable. In order to avoid this issue, we use the average amount of all the students who are in the same period as the student who borrows money expect his/her own consumption amount as an instrumental variable. We set a year before borrowing money from the platform as a long-term period and a month before borrowing money from the platform as a short-term period. The long-term and short-term regression results are shown in Table 3.

In long term, we can find that the recharge frequency has a significant positive effect on whether borrowing money, whose coefficient is approximately 0.514. Both the breakfast frequency and the recharge money have significant negative effect on whether borrowing money from the platform and their parameters are −0.484 and −0.673 separately. This indicates that students with a healthy breakfast eating habit are less likely to borrow money since they maybe more organized. Furthermore, the students with less recharge money and more recharge frequency are more likely to spend all their money quickly and seek for extra financial support.

Similarly, we can know that almost all the consumption behaviors have significant negative effect on the probability of borrowing money in the short term. The significance and value of each variable indicates that if a student decrease the consumption in campus suddenly in recent month and there exists a large chance that the student will need an additional financial support and loan money from online microlenders if the demand is not satisfied.

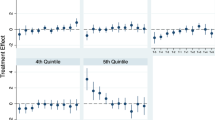

For the second research question: whether the students with loan behave differently after borrowing money from the microloan platform, we use the Difference-in-Difference (DID) method to test this question. We generated a dummy variable “time” and set time equal to 1 if the period of the variables is after borrowing else set time equal to 0. Our dependent variables can be divided into three categories. One category is dinning variable, including dinning frequency, dinning money and dinning regularity. The second category is shopping variable, including shopping frequency, shopping money and shopping regularity. The third category is recharge variable, including recharge frequency, recharge money and recharge regularity. We analysis the long-term effect and short-term effect. We controlled the demographic characteristics such as gender, age, enroll year. We also controlled the number of days of holiday, vacation and weekend. The long-term behavior change is shown in Table 4.

In long term, the students with loan do have an increase in consumption frequency and consumption money. Significant increase exists in dinner frequency, recharge frequency, dinning money and recharge money. The increase in consumption means that students borrow money from the microloan platform in order to improve their living quality other than because of some irrational consumption psychology and impulse buying.

The short-term behavior change is shown in Table 5. In short term, the increase of the consumption behavior of the student borrowers in campus are more significant. All the consumption variables are significant and positive. This further indicates the student are merely lack of money to improve their life quality.

The DID regression results with the student campus e-card data shows that the students didn’t borrow money for irrational consumption reasons or impulse buying, which is different from the common knowledge and intuitive feeling. It’s an important finding for the college administrator to recognize the student with real financial difficulties, offer financial support to them and help them get through.

5 Conclusion and Implications

College students are at a special period. Their financial demand is an important issue that need concern. How to find the target students that need financial support and trace their consumption behavior is a meaningful question both for academia and practice. Many universities have constructed campus e-card system in the proceeding of digital campus, which provide abundant student consumption data to investigate students’ consumption behavior. By combining student consumption data from a university in China and student borrowing data from a microloan platform, our study finds that students with less breakfast frequency, more recharge frequency but less recharge money are more likely to borrow money from the platform in long term. We infer that this is because this kind of students do not have a reasonable plan for using money. In short term, almost all the consumption behavior will decrease for the student borrowers. This indicates that the students will decrease their temporary consumption if they are short of money. This can be an important indicator for college managers to recognize the students with financial difficulties. Furthermore, we find that the students with loan have a significant improvement in their campus consumption for both long term and short term. This means the students borrow money from the platform for improving life quality other than for impulse consumption needs.

Our findings have some theoretical contributions. Firstly, we investigated the consumption characteristic of the students who borrow money from online lending platform with a unique empirical data and find out some valuable indicators. Secondly, we analyzed the consumption behavior difference of the students before borrowing and after borrowing, which is not investigated by prior literature. Thirdly, we researched the microloan platform risk management with campus e-card data. Last, we enriched the literature on campus e-card and microloan. Our findings also have practical implications for university, government and corporation. For universities, the conclusion can help them distinguish the students who need financial support, provide financial aids for these students, trace their consumption behaviors after borrowing, and provide a better solution for the problems of campus loan. For managers of microloan companies, they may better supervise the risk with students’ daily consumption data.

References

Agarwal, S., Liu, C.: Determinants of credit card delinquency and bankruptcy: macroeconomic factors. J. Econ. Finance 27(1), 75–84 (2003)

Allen, T.: Optimal (partial) group liability in microfinance lending. J. Dev. Econ. 121, 201–216 (2016)

Cai, S., Lin, X., Xu, D., et al.: Judging online peer-to-peer lending behavior: a comparison of first-time and repeated borrowing requests. Inf. Manag. 53(7), 857–867 (2016)

Canales, R., Greenberg, J.: A matter of (relational) style: loan officer consistency and exchange continuity in microfinance. Manag. Sci. 62(4), 1202–1224 (2016)

Gonzalez, L.: Online Social Lending: The Effect of Cultural, Economic and Legal Frameworks. Economic and Legal Frameworks (2014)

Guo B.: Research on the factors affecting the successful borrowing rate of P2P network lending in China—taking the case of Renrendai online lending as an example. In: International Conference on Industrial Economics System and Industrial Security Engineering, pp. 1–5. IEEE (2016)

Herzenstein, M., Andrews, R.L.: The democratization of personal consumer loans? Determinants of success in online peer-to-peer lending communities. Boston Univ. Sch. Manag. Res. Pap. 14(6), 1–36 (2008)

Herzenstein, M., Dholakia, U.M., Andrews, R.L.: Strategic herding behavior in peer-to-peer loan auctions. J. Interact. Mark. 25(1), 27–36 (2011)

Nan, J., Weisheng, X.: Student consumption and study behavior analysis based on the data of the campus card system. Microcomput. Appl. 31(2), 35–38 (2015)

Lin, M., Prabhala, N.R., Viswanathan, S.: Judging borrowers by the company they keep: friendship networks and information asymmetry in online peer-to-peer lending. Manag. Sci. 59(1), 17–35 (2013)

Lin, M., Viswanathan, S.: Home bias in online investments: an empirical study of an online crowdfunding market. Manag. Sci. 62(5), 1393–1414 (2015)

Liu, D., Brass, D.J., Lu, Y., et al.: Friendships in online peer-to-peer lending: pipes, prisms, and relational herding. MIS Q. 39(3), 729–742 (2013)

Lu, Y., Gu, B., Ye, Q., et al.: Social influence and defaults in peer-to-peer lending networks (2012)

Pötzsch, S., Böhme, R.: The role of soft information in trust building: evidence from online social lending. In: Acquisti, A., Smith, S.W., Sadeghi, A.-R. (eds.) Trust 2010. LNCS, vol. 6101, pp. 381–395. Springer, Heidelberg (2010). https://doi.org/10.1007/978-3-642-13869-0_28

Puro, L., Teich, J.E., Wallenius, H., et al.: Bidding strategies for real-life small loan auctions. Decis. Support Syst. 51(1), 31–41 (2011)

Serrano-cinca, C., Gutiérreznieto, B., Lópezpalacios, L., et al.: Determinants of default in P2P lending. PLoS ONE 10(10), e0139427 (2015)

Rui, T.: The Study on Academic Record Prediction and Students’ Friendship Network Detection Based on Consumption Data of Campus Card. Central China Normal University, Hubei (2016)

Fang, W., Zhuosheng, J.: Constructing student conduct analyzing system based on campus smart card system. Comput. Sci. 35(10), 212–215 (2008)

Jian, X.: The research and analysis of consume behavior and grades relativity on the basis of campus cards’ data. Nanchang University, Nanchang (2010)

Fu, Y., Jing, M., Cheng, D.: Analysis on data of the Campus IC Card based on Hadoop. Wirel. Internet Technol. 15, 77–79 (2016)

Zvilichovsky, D., Inbar, Y., Barzilay, O.: Playing Both Sides of the Market: Success and Reciprocity on Crowdfunding Platforms. Social Science Electronic Publishing (2015)

Acknowledgments

This work was supported by the National Natural Science Foundation of China (grant # 91546104) and the Scientific Research Project of Shanghai Science and Technology Committee (grant #17DZ1101002).

Author information

Authors and Affiliations

Corresponding author

Editor information

Editors and Affiliations

Rights and permissions

Copyright information

© 2019 Springer Nature Switzerland AG

About this paper

Cite this paper

Zhang, C., Xiao, S., Lu, T., Lu, X. (2019). Who Borrows Money from Microloan Platform? - Evidence from Campus E-card. In: Nah, FH., Siau, K. (eds) HCI in Business, Government and Organizations. Information Systems and Analytics. HCII 2019. Lecture Notes in Computer Science(), vol 11589. Springer, Cham. https://doi.org/10.1007/978-3-030-22338-0_24

Download citation

DOI: https://doi.org/10.1007/978-3-030-22338-0_24

Published:

Publisher Name: Springer, Cham

Print ISBN: 978-3-030-22337-3

Online ISBN: 978-3-030-22338-0

eBook Packages: Computer ScienceComputer Science (R0)