Abstract

The data envelopment analysis (DEA) technique has been found very useful for evaluating the mutual fund performance. This applied study extends previous results in two ways: to properly reflect the pervasive skewness and leptokurtosis in return distributions of actively managed funds, new risk measures value-at-risk (VaR) and conditional value-at-risk (CVaR) are introduced into inputs of the existing DEA models; to fairly evaluate the relative performance of the same fund during different time periods, we creatively treat the same fund during different periods as different decision making units. Except for confirming current empirical conclusions, detailed empirical analyses using data of the Chinese mutual fund market show that, VaR and CVaR, especially their combinations with traditional risk measures, are very helpful for comprehensively describing return distribution properties and fund characteristics such as the asset allocation structure, which, in turn, can better evaluate the overall performance of mutual funds. Treating the same fund during different time periods as different funds can not only show the specific performance variation, but reveal the reasons for that variation.

Similar content being viewed by others

Notes

See the web site http://www.cas.american.edu/ jpnolan

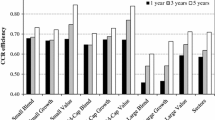

Due to the space limitation, we do not report here corresponding efficiency scores, which can be provided upon request.

Again, due to the space limitation, we do not present concrete estimates here, which can be provided upon request.

References

Ang JS, Chua JH (1979) Composite measures for the evaluation of investment performance. J Financ Quant Anal 14:361–384

Artzner P, Delbaen F, Eber JM, Heath D (1999) Coherent measures of risk. Math Financ 9:203–228

Banker RD, Charnes A, Cooper WW (1984) Some models for estimating technical and scale efficiencies in data envelopment analysis. Manage Sci 30:1078–1092

Basso A, Funari S (2001) A data envelopment analysis approach to measure the mutual fund performance. Eur J Oper Res 135:477–492

Basso A, Funari S (2002) A generalized performance attribution technique for mutual funds. Working Paper n.01.08, GRETA

Charnes A, Cooper WW, Rhodes E (1978) Measuring the efficiency of decision making units. Eur J Oper Res 2:429–444

Consiglio Andrea, Massabo Ivar, Ortobelli Sergio (2002) Non-Gaussian distribution for VaR calculation: an assessment for the Italian market. Working paper, University of Calabria

Cooper WW, Seiford LM, Tone K (2000) Data envelopment analysis: a comprehensive text with models, applications, references and DEA solver software. Kluwer, Boston

Duffie D, Pan J (1997) An overview of value at risk. J Deriv 4:7–49

Ferson WE, Schadt RW (1996) Measuring fund strategy and performance in changing economic conditions. J Finance 51:425–461

Jensen MC (1968) The performance of mutual funds in the period 1945–1964. J Finance 23:389–416

Kogon SM, Williams DB (1998) Characteristic function based estimation of stable parameters. In: Adler R, Feldman R, Taqqu M (eds) A practical guide to heavy tailed data. Birkhauser, Boston

Ma SC, Song LM, Wang W (2000) Empirical study of factors affecting stock prices in the Shanghai stock market. Stat Res 8:24–28 (in Chinese)

McMullen PR, Strong RA (1998) Selection of mutual fund using data envelopment analysis. J Bus Econ Stud 4:1–12

Morey MR, Morey RC (1999) Mutual fund performance appraisals: a multi-horizon perspective with endogenous benchmarking. Omega 27:241–258

Morgan JP (1996) RiskMetrics. Technical document, 4th edn. Morgan, New York

Murthi BPS, Choi YK, Desai P (1997) Efficiency of mutual funds and portfolio performance measurement: a non-parametric approach. Eur J Oper Res 98:408–418

Nolan JP (1997) Numerical computation of stable densities and distribution functions. Commun Stat-Stoch Models n. 13

Nolan JP (1999) An algorithm for evaluating stable densities in Zolotarev’s parameterization. Math Comput Model n. 29

Pastor J (1996) Translation invariance in data envelopment analysis: a generalization. Ann Oper Res 66:93–102

Rockafellar RT, Uryasev S (2000) Optimization of conditional value-at-risk. J Risk 2:21–42

Schneeweis T, Spurgin R (1998) Multifactor analysis of hedge funds, managed futures, and mutual fund return and risk characteristics. J Altern Invest 1–24 Fall

Sharpe WF (1966) Mutual fund performance. J Bus 34:119–138

Sortino FA, Price LN (1994) Performance measurement in a downside risk framework. J Invest 59–64 Fall

Stephens A, Proffitt D (1991) Performance measurement when return distributions are nonsymmetric. Q J Bus Econ 23–39 Autumn

Treynor JL (1965) How to rate management of investment funds. Harvard Bus Rev 43:63–75

Author information

Authors and Affiliations

Corresponding author

Additional information

This research was partially supported by the National Natural Science Foundation of China (10571141), the second author’s research was also supported by the Natural Science Foundation of Wenzhou University (2005L002). The authors are grateful to the anonymous referee, Professors Edwin Fischer and Hans–Otto Guenther (Editors) for their valuable comments and suggestions on a former version of this paper.

Rights and permissions

About this article

Cite this article

Chen, Z., Lin, R. Mutual fund performance evaluation using data envelopment analysis with new risk measures. OR Spectrum 28, 375–398 (2006). https://doi.org/10.1007/s00291-005-0032-1

Published:

Issue Date:

DOI: https://doi.org/10.1007/s00291-005-0032-1