Abstract

This study extends the affine Nelson–Siegel model by introducing the time-varying volatility component in the observation equation of yield curve, modeled as a standard EGARCH process. The model is illustrated in state-space framework and empirically compared to the standard affine and dynamic Nelson–Siegel model in terms of in-sample fit and out-of-sample forecast accuracy. The affine based extended model that accounts for time-varying volatility outpaces the other models for fitting the yield curve and produces relatively more accurate 6- and 12-month ahead forecasts, while the standard affine model comes with more precise forecasts for the very short forecast horizons. The study concludes that the standard and affine Nelson–Siegel models have higher forecasting capability than their counterpart EGARCH based models for the short forecast horizons, i.e., 1 month. The EGARCH based extended models have excellent performance for the medium and longer forecast horizons.

Similar content being viewed by others

Notes

Prior research supports the evidence of time-varying volatility in the interest rate, including Brenner et al. (1996) and Koedijk et al. (1997). Both of them have modeled for short term interest rate volatility, thereby implicitly arguing that it is not constant over time. Furthermore, the volatility in the Japanese bond market is also evidenced asymmetric in Ullah et al. (2014).

The continuous state transition matrix K is converted into 1-month conditional matrices by computing \(\mathrm {exp}(-K{\Delta }t )\) with \(\Delta t=1/12\). Results for the conditional 1 month K (denoted as \({\tilde{F}})\) are shown in “Appendix 4”.

The forecast period comprises 54 months for 1-month ahead forecasts, 49 months for 6-months ahead and 43 months for the 1-year ahead forecasting.

References

Ang A, Piazzesi M (2003) A no-arbitrage vector autoregression of term structure dynamics with macroeconomic and latent variables. J Monet Econ 50:745–787

Balduzzi P, Das SR, Foresi S, Sundaram RK (1996) A simple approach to three factor affine term structure models. J Fixed Income 6:43–53

Black, F (1976) Studies of stock price volatility changes. In: Proceedings of the 1976 Meeting of the American Statistical Association, business and economics statistics section, pp 177–181

Brenner R, Harjes R, Kroner K (1996) Another look at models of the short-term interest rate. J Financ Quant Anal 31:85–107

Chen L (1996) Stochastic mean and stochastic volatility: a three-factor model of the term structure of interest rates and its applications to the pricing of interest rate derivatives. Blackwell Publishers, Oxford

Chen R, Scott L (1992) Pricing interest rate options in a two factor Cox–Ingersoll–Ross model of the term structure. Rev Financ Stud 5:613–636

Christensen JHE, Diebold FX, Rudebusch GD (2011) The affine arbitrage-free class of Nelson–Siegel term structure models. J Econom 164:4–20

Christie AA (1982) The stochastic behavior of common stock variances -value, leverage and interest rate effects. J Financ Econ 10:407–432

Cox JC, Ingersoll JE, Ross SA (1985) A theory of the term structure of interest rates. Econometrica 53:385–407

Dai Q, Singleton K (2000) Specification analysis of affine term structure models. J Financ 55:1943–1978

Diebold FX, Li C (2006) Forecasting the term structure of government bond yields. J Econom 130:337–364

Duffee GR (2002) Term premia and interest rate forecasts in affine models. J Financ 53:527–552

Duffie D, Kan R (1996) A yield-factor model of interest rates. Math Financ 6(4):379–406

Durbin J, Koopman SJ (2012) Time series analysis by state space methods. Number 38. Oxford University Press, Oxford

Fama E, Bliss R (1987) The information in long-maturity forward rates. Am Econ Rev 77:680–692

French KK, Sciswert GW, Stambaugh R (1987) Expected stock returns and volatility. J Financ Econ 19:3–29

Hamilton JD (1994) State space models. In: Engle RF, McFadden DL (eds) Handbook of econometrics. Elsevier, Amsterdam, pp 3041–3080

Hansen PR, Lunde A, Nason JM (2011) The model confidence set. Econometrica 79:453–497

Hansen PR, Lunde A, Nason JM (2005) A test for superior predictive ability. Econometrica 23:365–380

Harvey AC (1989) Forecasting structural time series models and the Kalman filter. Cambridge University Press, Cambridge

Hull J, White A (1990) Pricing interest-rate derivative securities. Rev Financ Stud 3(4):573–592

Kim DH, Orphanides A (2005) Term structure estimation with survey data on interest rate forecasts. Finance and Economics Discussion Board No. 48, Board of Governors of the Federal Reserve System

Koedijk K, Nissen F, Schotman P, Wolff C (1997) The dynamics of short-term interest rate volatility reconsidered. Eur Financ Rev 1:105–130

Koopman S, Mallee M, van der Wel M (2010) Analyzing the term structure of interest rates using dynamic Nelson–Siegel model with time-varying parameters. J Bus Econ Stat 28:329–343

Longstaff FA, Schwartz ES (1992) Interest rate volatility and the term structure: a two factor general equilibrium model. J Financ 47:1259–1282

Nelson CR, Siegel AF (1987) Parsimonious modeling of yield curves. J Bus 60:473–489

Svensson LEO (1995) Estimating forward interest rates with the extended Nelson–Siegel method. Sver Riksbank Q Rev 3:13–26

Ullah W, Matsuda Y, Tsukuda Y (2013a) Term structure modeling and forecasting of government bond yields: does a good in-sample fit imply reasonable out-of-sample forecast? Econ Pap J Appl Econ Policy 32(4):535–560

Ullah W, Matsuda Y, Tsukuda Y (2014) Dynamics of the term structure of interest rates and monetary policy: is monetary policy effective during zero interest rate policy? J Appl Stat 41(3):546–572

Ullah W, Tsukuda Y, Matsuda Y (2013b) Term structure forecasting of government bond yields with latent and macroeconomic factors: do macroeconomic factors imply better out-of-sample forecasts? J Forecast 32:702–723

Vasicek O (1977) An equilibrium characterization of the term structure. J Financ Econ 5:177–188

Welch G, Bishop G (2006) An introduction to the Kalman filter. Department of Computer Science, University of North Carolina, Chapel Hill

Acknowledgements

We would like to thank the anonymous referees and the Editor for making useful comments to improve this paper.

Author information

Authors and Affiliations

Corresponding author

Appendices

Appendix 1

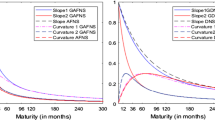

The yield-adjustment term A in the AFNS and AFNS-EGARCH models

The appendix reports the analytical solution for the yield-adjustment term A as derived in the Christensen et al. (2011). For a general volatility matrix,

the analytical solution for is: \({A}(t,T)/(T-t)\) is:

Since, the A(t, T) term is a complex function of the volatility matrix \(\Sigma \), decay parameter \(\uplambda \) and maturity \((T-t)\). In both affine based models, i.e., AFNS and AFNS-EGARCH, we use the above analytical solution to estimate the yield curve.

Appendix 2

Coefficients and latent variable in the general state-space form

In the statistical formulation of the models in Sect. 2.3, the matrices and vectors for the state and observations equations should be considered as follows. The matrices and vectors in state-space system in (12–14) for the simple AFNS model should be defined as:

while the system in (12–14), for the AFNS-EGARCH can be specified as:

where \({\Lambda }(\lambda )\) is \((\hbox {N}\times 3)\) matrix of loadings, \({\Gamma }_{\varepsilon }\) is (\(\hbox {N}\times 1\)) vector showing the sensitivity of various yields to common volatility component, \(\theta \) is \((3\times 1)\) vectors of factors mean, and K is \((3\times 3)\) full-matrices of parameters. \(\varepsilon _{t}\) and \(v_{t}\) are \((\hbox {N}\times 1)\) and \((3\times 1)\) innovations vectors of the observation and state equations respectively, \({\Omega }\) is \((\hbox {N}\times \hbox {N})\) covariance matrix of the measurement equation innovations, and \({\Sigma }_{v}\) is \((3\times 3)\) lower triangular covariance matrix of the state innovations (assumed to be a full-matrix rather than a diagonal one). Moreover, \(\varepsilon _{t}^{+}\) is \((\hbox {N}\times 1)\) errors vector of the observation equation in EGARCH based model.

Appendix 3

Data description

We consider JGB yields with maturities of 3, 6, 9, 12, 15, 18, 21, 24, 30, 36, 48, 60, 72, 84, 96, 108, 120, 180, 240 and 300 months. The yields are derived from bid/ask average price quotes, from January 2000 through June 2013, using the Fama and Bliss (1987) methodology.

The figure shows the yield curves, 2000:01–2013:06. The sample consists of monthly yield data from January 2000 to June 2013 (162 months) for maturities of 3, 6, 9, 12, 15, 18, 21, 24, 30, 36, 48, 60, 72, 84, 96, 108, 120, 180, 240 and 300 months (20 maturities)

Table 8 provides summary statistics for the data-set. For each maturity, we report mean, standard deviation, minimum, maximum, skewness, kurtosis, and autocorrelation coefficients at various displacements. The summary statistics reveal that the average yield curve is upward sloping. Unconditional volatility increases with maturity and yields for all maturities are persistent, however, relatively short rates persistency is higher than those of the long rates.

In addition to the findings in Table 8, we see few interesting characteristics in Fig. 4, which plots cross-section of yields over time. The first noticeable fact is that long term yields vary significantly over time. Second, the short rates are almost zero during the prolonged period except with a little rise in late 2006 and early 2007 that causes a fall in the slope of the curves (apparent in figure). Moreover, when short rates are stuck at zero, the long end seem more volatile than the short end of the curves.

Appendix 4

1 month conditional estimates of mean-reversion matrix \({{\varvec{K}}}\)

The state transition matrix K in AFNS and AFNS-EGARCH are modeled continuously and should be transformed in order to be comparable with the DNS based specifications. The continuous state transition matrix K is converted into 1-month conditional matrix by computing \(\mathrm {exp}( -K{\Delta }t )\) with \({\Delta }t=1/12\). The resulting matrix for the AFNS is as:

while for the AFNS-EGARCH is as:

The 1 month conditional estimation results indicate that all the three factors are more persistent in the AFNS-EGARCH than the rest of three models, being very close to one. Cross-factors dynamics seems unimportant in the AFNS-EGARCH model, while reasonably stronger in AFNS framework than the rest of three models.

Rights and permissions

About this article

Cite this article

Ullah, W. Term structure forecasting in affine framework with time-varying volatility. Stat Methods Appl 26, 453–483 (2017). https://doi.org/10.1007/s10260-017-0378-y

Accepted:

Published:

Issue Date:

DOI: https://doi.org/10.1007/s10260-017-0378-y