Abstract

In this paper, we propose an uncertain energy model with a time-varying volatility factor to describe the electricity and gas futures price dynamics. The corresponding spark-spread option pricing problem is also discussed. Numerical experiments show the effectiveness of proposed pricing method. Compared with the existing stochastic models, our uncertain energy model has a better performance to catch the price evolution of both gas and electricity futures.

Similar content being viewed by others

References

Chen, X., & Gao, J. (2013). Uncertain term structure model of interest rate. Soft Computing, 17(4), 597–604.

Chen, X., Li, J., Xiao, C., & Yang, P. (2021). Numerical solution and parameter estimation for uncertain SIR model with application to COVID-19. Fuzzy Optimization and Decision Making, 20(2), 189–208.

Hassanzadeh, S., & Mehrdoust, F. (2018). Valuation of European option under uncertain volatility model. Soft Computing, 22(12), 4153–4163.

Hassanzadeh, S., & Mehrdoust, F. (2020). European option pricing under multifactor uncertain volatility model. Soft Computing, 24(12), 8781–8792.

Jia, L., & Chen, W. (2021). Uncertain SEIAR model for COVID-19 cases in China. Fuzzy Optimization and Decision Making, 20(2), 243–259.

Lio, W., & Liu, B. (2021). Initial value estimation of uncertain differential equations and zero-day of COVID-19 spread in China. Fuzzy Optimization and Decision Making, 20(2), 177–188.

Liu, B. (2008). Fuzzy process, hybrid process and uncertain process. Journal of Uncertain systems, 2(1), 3–16.

Liu, B. (2009). Some research problems in uncertainty theory. Journal of Uncertain Systems, 3(1), 3–10.

Liu, B. (2012). Why is there a need for uncertainty theory. Journal of Uncertain Systems, 6(1), 3–10.

Liu, B. (2015). Uncertainty Theory (5th ed.). Uncertainty Theory Laboratory.

Liu, Y., & Liu, B. (2022). Estimating unknown parameters in uncertain differential equation by maximum likelihood estimation. Soft Computing, 26(6), 2773–2780.

Liu, Z. (2021). Generalized moment estimation for uncertain differential equations. Applied Mathematics and Computation, 392, 125724.

Liu, Z., & Yang, X. (2021). A linear uncertain pharmacokinetic model driven by Liu process. Applied Mathematical Modelling, 89(2), 1881–1899.

Liu, Y., & Liu, B. (2022). Residual analysis and parameter estimation of uncertain differential equations. Fuzzy Optimization and Decision Making. https://doi.org/10.1007/s10700-021-09379-4

Mehrdoust, F., & Najafi, A. R. (2020). An uncertain exponential Ornstein-Uhlenbeck interest rate model with uncertain CIR volatility. Bulletin of the Iranian Mathematical Society, 46(5), 1405–1420.

Mehrdoust, F., & Noorani, I. (2021). Forward price and fitting of electricity Nord Pool market under regime-switching two-factor model. Mathematics and Financial Economics, 1-43.

Mehrdoust, F., & Noorani, I. (2022). Valuation of spark-spread option written on electricity and gas forward contracts under two-factor models with non-Gaussian Lévy processes. Computational Economics, 1-47.

Noorani, I., Mehrdoust, F., & Lio, W. (2021). Electricity spot price modeling by multi-factor uncertain process: a case study from the Nordic region. Soft Computing, 1-22.

Rauch, J., Krayzler, M., Brunner, B., & Zagst, R. (2013). Pricing of derivatives on commodity indices. International Review of Financial Analysis, 29, 143–151.

Sheng, Y., Yao, K., & Chen, X. (2020). Least squares estimation in uncertain differential equations. IEEE Transactions on Fuzzy Systems, 28(10), 2651–2655.

Tang, H., & Yang, X. (2021). Uncertain chemical reaction equation. Applied Mathematics and Computation, 411, 126479.

Wimschulte, J. (2010). The futures and forward price differential in the Nordic electricity market. Energy Policy, 38(8), 4731–4733.

Yao, K., & Liu, B. (2020). Parameter estimation in uncertain differential equations. Fuzzy Optimization and Decision Making, 19(1), 1–12.

Yao, K., & Chen, X. (2013). A numerical method for solving uncertain differential equations. Journal of Intelligent & Fuzzy Systems, 25(3), 825-832.

Yang, X., Liu, Y., & Park, G. (2020). Parameter estimation of uncertain differential equation with application to financial market. Chaos, Solitons & Fractals, 139, 110026.

Author information

Authors and Affiliations

Corresponding author

Additional information

Publisher's Note

Springer Nature remains neutral with regard to jurisdictional claims in published maps and institutional affiliations.

Appendix

Appendix

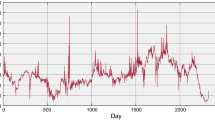

The data set for the NYMEX gas and the New England electricity futures prices are collected from EIA (Energy Information Administration) on a trading day from January 01, 2021 to June 30, 2021. The EIA is one of the reliable sources of energy data that many researchers rely on to collect their data on energy research (Tables 3 and 4).

Rights and permissions

About this article

Cite this article

Mehrdoust, F., Noorani, I. & Xu, W. Uncertain energy model for electricity and gas futures with application in spark-spread option price. Fuzzy Optim Decis Making 22, 123–148 (2023). https://doi.org/10.1007/s10700-022-09386-z

Accepted:

Published:

Issue Date:

DOI: https://doi.org/10.1007/s10700-022-09386-z