Abstract

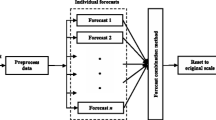

In the field of forecasting, there are always more than one method to deal with a problem, and more than one institute will supply their own research on the same problem. It’s hard to say which method or information source is better, so the research how to make full use of all the information that we have is valuable. In this paper, we proposed a new fusion method to make full use of all kinds of forecast information to improve the performance of forecasting and made an application to oil price forecast fusion by it. This approach presented a stable and great performance. What’s more, it doesn’t require training data, little limit of the source data, no complex computation, and it also provides a solution to combination puzzle.

Similar content being viewed by others

References

Abramson B, Finizza A (1995) Probabilistic forecasts from probabilisticmodels: a case study in the oil market. Int J Forecast 11(1):63–72

Alvarez-Ramirez J, Soriano A, Cisneros M, Suarez R (2003) Symmetry/anti-symmetry phase transitions in crude oil markets. Phys A 322:583–596

Andrawis RR, Atiya AF, El-Shishiny H (2011) Forecast combinations of computational intelligence and linear models for the NN5 time series forecasting competition. Int J Forecast 27:672–688

Andreas Graefe, Scott Armstrong J, Randall J. Jones Jr., Alfred G. Cuzán (2014) Combining forecasts: an application to elections. Int J Forecast 30:43–54

Assaad M, Bone R, Cardot H (2008) A new boosting algorithm for improved time-series forecasting with recurrent neural networks. Inf Fusion 9(1):41–55

Barrow DK, Crone SF (2016) A comparison of AdaBoost algorithms for time series forecast combination. Int J Forecast 32:1103–1119

Cheng Hsiao, Shui Ki Wan (2014) Is there an optimal forecast combination? J Econ 178:294–309

Claeskens G, Magnus JR, Vasnev AL, Wang W (2016) The forecast combination puzzle: a simple theoretical explanation. Int J Forecast 32:754–762

Conflitt C, De Mol C, Giannone D (2015) Optimal combination of survey forecasts. Int J Forecast 31:1096–1103

Cortes C, Vapnik V (1995) Support-vector networks, maching learning 20:273–297

De Gooijer JG, Hyndman RJ (2006) 25 years of time series forecasting. Int J Forecast 22:443–473

Drucker H (1997) Improving regressors using boosting techniques. In: The fourteenth international conference on machine learning, Morgan Kaufmann Inc, pp 107–115

Duin RPW, Tax DMJ (2000) Experiments with classifier combining rules, multiple classifier systems, Lecture notes in computer science, vol. 1857, pp 16–29

Freund Y, Schapire RE (1997) A decision-theoretic generalization of on-line learning and an application to boosting. J Comput Syst Sci 55:119–139

Hagen R (1994) How is the international price of a particular crude determined? OPEC Review 18(1):145–158

Hastie T, Tibshirani R, Friedman J (2009) The elements of statistical learning. Springer, New York

Lam L, Suen CY (1997) Application of majority voting to pattern recognition: an analysis of its behavior and performance. IEEE Trans Syst Man: Syst Hum 27(5):553–568

Mirmirani S, Li HC (2004) A comparison of VAR and neural networks with genetic algorithm in forecasting price of oil. Adv Econ 19:203–223

Mohammadi H, Su L (2010) International evidence on crude oil pricedynamics: applications of ARIMA-GARCH models. Energy Econ 32:1001–1008

Perols J, Chari K, Agrawal M (2009) Information market-based decision fusion. Manage Sci 55(5):827–842

Samuelsa JD, Rodrigo M. Sekkel (2017) Model confidence sets and forecast combination. Int J Forecast 33:48–60

Suen CY, Lam L (2000) Multiple classifier combination methodologies for different output levels. In: multiple classifier systems, Lultiple Classifier Systems. MCS 2000. Lecture Notes in Computer Science, vol 1857. Springer, Berlin, pp 52–66

Wei YG, Lim CP, Peh KK (2003) Predicting drug dissolution profiles with an ensemble of boosted neural networks. IEEE Trans Neural Networks 14(2):459–463

Xie JR, Hong T (2016) GEFCom2014 probabilistic electric load forecasting: an integrated solution with forecast combination and residual simulation. Int J Forecast 32:1012–1016

Xie W, Yu LA, Xu SY, Wang SY (2006) A new method for crude oilprice forecasting based on support vector machines. Lect Notes Comput Sci 3994:441–451

Yu LA, Wang SY, Lai KK (2008) Forecasting crude oil price with anEMD-based neural network ensemble learning paradigm. Energy Econ 30:2623–2635

Zhang JS, Feng X, Zou SH (2014) On China’s coal demand forecast model based on the trend combination. Commer Res 446:51–56

Author information

Authors and Affiliations

Corresponding author

Rights and permissions

About this article

Cite this article

Ye, Y., Zhang, J., Huang, Z. et al. A new information fusion method of forecasting. J Ambient Intell Human Comput 10, 307–314 (2019). https://doi.org/10.1007/s12652-017-0666-2

Received:

Accepted:

Published:

Issue Date:

DOI: https://doi.org/10.1007/s12652-017-0666-2