Abstract

Blockchain systems come with the promise of being inclusive for a variety of decentralized applications (DApps) that can serve different purposes and have different urgency requirements. Despite this, the transaction fee mechanisms currently deployed in popular platforms as well as previous modeling attempts for the associated mechanism design problem focus on an approach that favors increasing prices in favor of those clients who value immediate service during periods of congestion. To address this issue, we introduce a model that captures the traffic diversity of blockchain systems and a tiered pricing mechanism that is capable of implementing more inclusive transaction policies. In this model, we demonstrate that EIP-1559, the transaction fee mechanism currently used in Ethereum, is not inclusive and demonstrate experimentally that its prices surge horizontally during periods of congestion. On the other hand, we prove formally that our mechanism achieves stable prices in expectation and we provide experimental results that establish that prices for transactions can be kept low for low urgency transactions, resulting in a diverse set of transaction types entering the blockchain. At the same time, perhaps surprisingly, our mechanism does not necessarily sacrifice revenue since the lowering of the prices for low urgency transactions can be covered from high urgency ones due to the price discrimination ability of the mechanism.

Access this chapter

Tax calculation will be finalised at checkout

Purchases are for personal use only

Similar content being viewed by others

Notes

- 1.

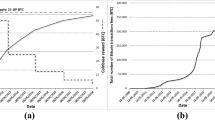

Both bitcoin and Ethereum average transaction charts exhibit periods of spikes that correlate with specific application use, cf. https://ycharts.com/indicators/bitcoin_average_transaction_fee and https://ycharts.com/indicators/ethereum_average_transaction_fee.

- 2.

Notice that the mechanism \(\mathcal {M}\) also takes into account F. In practice, this is not a direct input but a result of some dynamic price update mechanism that only observes some of the demand.

- 3.

In principal, TP can be extended to operate with an even “richer” set of acceptable diversity objectives.

- 4.

By medium-term here we mean sufficient time for the prices and delays to change, but not the tier number and size which are updated less frequently.

- 5.

For simplicity, we use k in place of \({\ensuremath {k_{\max }}}\) in this section, as the number of tiers is assumed to be fixed in our analysis.

References

The Ethereum Project. https://www.ethereum.org/

Basu, S., Easley, D., O’Hara, M., & Sirer, E. G. (2019). Towards a functional fee market for cryptocurrencies. arXiv:1901.06830

Buterin, V. (2016). On inflation, transaction fees and cryptocurrency monetary pol- icy.

Buterin, V., Conner, E., Dudley, R., Slipper, M., & Norden, I. (2019). Ethereum improvement proposal 1559: Fee market change for eth 1.0 chain.

Chung, H., Roughgarden, T., & Shi, E. (2024). Collusion-resilience in transaction fee mechanism design. arXiv:2402.09321

Chung, H., & Shi, E. (2021). Foundations of transaction fee mechanism design (p. 1474). IACR Cryptol. ePrint Arch.

Chung, H., & Shi, E. (2023). Foundations of transaction fee mechanism design. In Proceedings of the 2023 Annual ACM-SIAM Symposium on Discrete Algorithms (SODA) (pp. 3856–3899). SIAM.

Ferreira, M. V. X., Moroz, D. J., Parkes, D. C., & Stern, M. (2021). Dynamic posted-price mechanisms for the blockchain transaction-fee market. In Proceedings of the 3rd ACM Conference on Advances in Financial Technologies (pp. 86–99).

Fiat, A., Goldner, K., Karlin, A. R., & Koutsoupias, E. (2016). The fedex problem. In V. Conitzer, D. Bergemann, & Y. Chen (Eds.), Proceedings of the 2016 ACM Conference on Economics and Computation, EC ’16, Maastricht, The Netherlands, July 24–28, 2016 (pp. 21–22). ACM.

Gafni, Y., & Yaish, A. (2024). Barriers to collusion-resistant transaction fee mechanisms.

Goldberg, A. V., Hartline, J. D., Karlin, A. R., Saks, M., & Wright, A. (2006). Competitive auctions. Games and Economic Behavior, 55(2), 242–269.

Huberman, G., Leshno, J. D., & Moallemi, C. (2021). Monopoly without a monopolist: An economic analysis of the bitcoin payment system. The Review of Economic Studies, 88(6), 3011–3040.

Lavi, Ron, Sattath, Or., & Zohar, Aviv. (2022). Redesigning bitcoin’s fee market. ACM Transactions on Economics and Computation, 10(1), 1–31.

Leonardos, S., Monnot, B., Reijsbergen, D., Skoulakis, E., & Piliouras, G. (2021). Dynamical analysis of the eip-1559 ethereum fee market. In Proceedings of the 3rd ACM Conference on Advances in Financial Technologies (pp. 114–126).

Leonardos, S., Reijsbergen, D., Reijsbergen, D., Monnot, B., & Piliouras, G. (2022). Optimality despite chaos in fee markets. arXiv:2212.07175

Nakamoto, S. (2008). Bitcoin: A peer-to-peer electronic cash system. http://bitcoin.org/bitcoin.pdf.

Reijsbergen, D., Sridhar, S., Monnot, B., Leonardos, S., Skoulakis, S., & Piliouras, G. (2021) Transaction fees on a honeymoon: Ethereum’s eip-1559 one month later. In 2021 IEEE International Conference on Blockchain (Blockchain) (pp. 196–204). IEEE.

Roughgarden, T. (2021). Transaction fee mechanism design. In P. Biró, S. Chawla, & F. Echenique (Eds.) EC ’21: The 22nd ACM Conference on Economics and Computation, Budapest, Hungary, July 18–23, 2021 (p. 792). ACM.

Loerakker, D., Kadianakis, G., Garnett, M., Taiwo, M., Dietrichs, A., Buterin, V., Feist, D. (2022). EIP-4844: Shard Blob Transactions. Retrieved April 15, 2024.

Yao, A. C.-C. (2018). An incentive analysis of some bitcoin fee designs. arXiv:1811.02351.

Author information

Authors and Affiliations

Corresponding author

Editor information

Editors and Affiliations

Appendices

Appendix 1: Tiered Pricing Has High Welfare

Proof

(Proof of Theorem 1.2) Let p be the price selected by EIP-1559, and \((d_1,p_1),\ldots ,(d_k,p_k)\) be the tier parameters selected by TP under load F. We have shown that these parameters are well-defined when the load is regular.

To satisfy the demand constraints in EIP-1559, we have that

where v is sampled from F. Similarly for TP, we have that:

Let \(p'\) be such that \(\Pr [ v(1) \ge p' | v \leftarrow F ] = B_1/n\). Also, we define the following sets:

-

\(V'= \{v \in F| v(1) \ge p'\}\),

-

\(V_1= \{v \in F| v(1) \ge p_1\}\),

-

\(V_2= \{v \in F| v(1) \ge p', (1,p_1) = M(v|F)\}\),

-

\(V_3 = V' \setminus V_2\),

-

\(V_4 = \{v \in F| v(1) < p', (1,p_1) = M(v|F)\}\),

where M is the TP mechanism.

First, since \(V_2 \subseteq V'\) and \(\Pr [ v\in V'] = B_1/n\), it is implied that \(p' \ge p_1\). Next, note that:

Also, for any \(v\in V_3\), since v selected a different tier than 1, it holds that \(v(d_j) -p_j \ge v(1) - p_1\), where \((d_j,p_j)\) is the value assigned by TP to v. Hence, by the definition of \(V_4\), if \(v' \in V_4\), it holds that: \(v(d_j)+v'(1) \ge v(1) + p_j \ge v(1)\).

We can thus lower bound the welfare of TP by the welfare contributed by the transactions in sets \(V_2,V_3,V_4\). Note that these sets are disjoint and we are not double counting.

where the first equality follows from the linearity of expectation. The second inequality follows by the fact that \(\Pr [v\in V_3] = \Pr [v\in V_4]\) and our earlier observation about the welfare generated by elements of the two sets. The last inequality follows from the fact that \(\Pr [ v\in V'] = B_1/n\) and that for any \(v_1\in V',v_2 \not \in V'\) it holds that \(v_1(1) > v(2)\).

Appendix 2: Tiered Pricing Is Diverse

It is quite challenging to study the entire tiered pricing mechanism, so we break the analysis up into discrete modules. We first adapt our steady state model to this particular mechanism. Then, we show that by fixing the tier sizes and delays we can prove that there always exists a unique ‘average’ price that satisfy our target tier sizes. Given this property of the price update inner loop, we can proceed to the less frequent delay updates of the tiered mechanism. We prove that such delays satisfying Inequality (1.1) exist (with accompanying prices) for any set of parameters \({\ensuremath {k_{\max }}},(a_i,\lambda _i,\mu _i)_{i}\).

Tiered Transaction Mechanisms

We focus on a particular case of transaction mechanisms with prices and delays. Specifically, we split up the blockchain throughput into tiers, each of which offers a distinct price and delay option. Suppose that our blockchain has tiers \(\{0, 1, 2, \ldots , k\}\)Footnote 5 with corresponding sizes \({\ensuremath {\textbf{B}}} = (B_1, B_2, \ldots , B_k)\) and delays \({\ensuremath {\textbf{d}}} = (d_1, d_2, \ldots , d_k)\) such that

where B is the throughput of the blockchain. Since not all transactions will be included, tier 0 is special and is reserved for those. This special tier has \(B_0 = \infty \). We assume that tiers with larger indices offer a reduced quality of service and have strictly higher delays (i.e., \(d_{j+1} > d_{j}\)). Each tier is also associated with a price \({\ensuremath {\mathbf {~}}}\hbox {p} = (p_1, p_2, \ldots , p_k)\). Slightly abusing the notation, we will refer to the utility of transaction i given delay d and price p as \(u_i(d, p).\) The mechanism would select for each transaction the tier that maximizes its utility. We use the tuple \(({\ensuremath {\textbf{B}}}, {\ensuremath {\textbf{d}}}, {\ensuremath {\textbf{p}}})\) as a shorthand to refer to a particular blockchain.

Given transactions \((v_1, \ldots , v_n) \leftarrow F\) let \(X_{ij}\) be the random variable indicating that transaction i chose tier j. Extending the preliminaries, we define the demand (or used space) of each tier as

and require that in expectation it should be at most as much as the allocated size of the tier

except for \(T_0\), which needs to capture every transaction that’s left out:

Note that Eq. 1.5 is always satisfied by the definition of \(X_{ij}\).

Of course, for any load n, F there are many blockchains \(({\ensuremath {\textbf{B}}}, {\ensuremath {\textbf{d}}}, {\ensuremath {\textbf{p}}})\) satisfying compatibility (recall Definition 1.1). For instance, any prices that are high enough to exclude all transactions. The following definition captures how EIP-1559 style price updates would translate into our steady-state model for the tiered mechanism.

Definition 1.7

(EIP-1559 Stable Blockchain) A blockchain \(({\ensuremath {\textbf{B}}}, {\ensuremath {\textbf{d}}}, {\ensuremath {\textbf{p}}})\) is stable for load n, F if it is compatible and for every \(j\in [k]\):

At first glance, it might seem as if Ethereum itself does not satisfy this definition. However, notice that for Ethereum, the target tier size (which is just the tier size in our notation) is not the physical maximum block size, but rather the target of having blocks be \(50\%\) full. Under that prism, as long as the prices lead to low demand, they will keep decreasing until the eventually reach 0, if necessary. In addition, the prices may not be ‘stable’ in the commonly understood sense. Indeed, as [14, 15] show, even for EIP-1559 the prices may exhibit chaotic behavior. However, it is also argued that the demand target is consistency close to its goal and the average of prices does converge to the theoretical value.

Distributional Assumptions

To prove the existence results, we need to impose certain mild regularity assumptions on the load distribution F. Specifically, that the expected load is continuous and behaves ‘predictably’ as the delay and price change.

Definition 1.8

(Load Regular) The value function distribution F is load regular if the valuations generated are parameterized by a tuple \((v_0, h)\) where \(v_0 \in [0,1]\) is the value for no delay and \(h : \mathbb {R}_{\ge 1} \rightarrow [0,1]\) is the discount factor and have the following form

Moreover, we need that

-

h(d) is continuous and strictly decreasing in d.

-

\(\lim _{d \rightarrow \infty } h(d) = 0\).

-

The probability density function of the marginal distribution of \(v_0\), defined as

$$\begin{aligned} f(v_0 | h) = \frac{d \Pr \left[ v \le v_0 | h\right] }{dv_0} \end{aligned}$$exists for all h.

-

\(f(v_0 | h) > 0\) for \(v_0 \in [0,1]\).

Remark 1.4

This assumption is similar to the more common ’no point masses’ assumption for single dimensional valuations and quasilinear utilities.

Both conditions are necessary to ensure that a wide range of transaction fee mechanism designs have a well defined steady state behavior. For instance, notice that without the positive pdf requirement for \(v_0\) it is impossible to guarantee that stable prices exists, even for Ethereum with just one tier. This is clear if the demand exceeds the supply and everyone has exactly the same valuation. However, the other requirements are also crucial. An example highlighting the need for strictly decreasing temporal discounts can be found in Observation 1.1.

It is not always easy to work directly with these probability distributions because they are over functions, instead of just real numbers. We provide the following lemma which often comes in handy and provides some guarantee that the assumptions lead to better mathematical properties. Due to space constraints we point to the full version of the paper for the proof.

Lemma 1.1

For any blockchain \(({\ensuremath {\textbf{B}}}, {\ensuremath {\textbf{d}}}, {\ensuremath {\textbf{p}}})\) and regular load n, F, \(\mathbb {E}\left[ T_j\right] \) is continuous in \({\ensuremath {\textbf{p}}}\) and \({\ensuremath {\textbf{d}}}\). This holds even if we drop the last regularity assumption, namely that \(f(v_0 | h) > 0\).

Finally, we argue that given the notion of EIP-1559 stability, the previous distributional assumptions are indeed necessary.

Observation 1.1

Suppose that \(B_1 = B_2 = 1, d_1 = 1, d_2 = 2, n = 3\) and for F:

-

With probability 1/3, \(v_0\) is distributed uniformly in [0, 1] for delay less than 1 and 0 otherwise.

-

With probability 2/3, \(v_0\) is uniform in [0, 1] for any delay.

If \(p_1 \ne p_2\) then it has to be \(p_1 > p_2\). Otherwise, all transactions will chose \(B_1\), leaving \(B_2\) empty. By Definition 1.7 \(p_2 = 0\), leading to a contradiction since we assumed \(p_1 < p_2 = 0\) and \(p_1\) has to be non-negative. This leaves us with two options:

-

\(p_1 > p_2\). In this case, all transactions with \(d=2\) will choose to pay \(p_2\). To achieve stability, we need that \(p_2 > 1/2\). But then \(p_1 > p_2 > 1/2\) is too high to fill \(B_1\).

-

\(p_1 = p_2\). In this case, \(B_1\) will have higher demand than \(B_2\), as it is selected by transactions with \(d=1\) and half of the transactions with \(d = 2\). Since \(B_1 = B_2\), it is impossible to have prices \(p_1 = p_2\) that equally fill both blocks. Since the block that is not totally filled needs to have a price equal to 0, \(p_1 = p_2 > 0\) is not a possible solution.

Properties of the Tiered Pricing Mechanism

We need to show that the previously described tiered pricing mechanism does indeed converge to set of steady-state tier parameters. This requires laying some theoretical groundwork, before proceeding to establish that:

-

For fixed tier sizes and delays we can always find compatible and EIP-1559 stable prices.

-

These prices are unique.

-

For fixed tier sizes, we can always find delays and prices satisfying a desired diversity objective.

The first step, also serving as a ‘sanity’ check, for this model is all about Definitions 1.1 and 1.7. Do blockchains such as Ethereum satisfy our definitions? The answer is positive. In Ethereum’s case every parameter other than the price is set: there is just one tier with minimal delay.

Proposition 1.2

Ethereum with EIP-1559 is compatible with any load. In particular, for any B and n, F there exists price \({\ensuremath {\textbf{p}}}\) such that \(({\ensuremath {\textbf{B}}}, {\ensuremath {\textbf{d}}}, {\ensuremath {\textbf{p}}})\) is compatible with n, F.

Proof

For EIP-1559 we have that \(B = B_1\) and \(d_1 = 0\). Clearly, for \(p_1 = 0\) we have that \(\mathbb {E}\left[ T_1\right] = n\), by Definition 1.8. Since for \(p_1 > 1\) we have that \(\mathbb {E}\left[ T_1\right] = 0\) (since the utility of any transaction is at most 1) and \(\mathbb {E}\left[ T_1\right] \) is continuous in \(p_1\), there exists some \(p_1 > 0\) such that \(\mathbb {E}\left[ T_j\right] = B < n\), satisfying Definition 1.1.

This is a good time to highlight that for tiered blockchains, the combination of compatibility and EIP-1559 stability implies a more intuitive property.

Proposition 1.3

For any blockchain \(({\ensuremath {\textbf{B}}}, {\ensuremath {\textbf{d}}}, {\ensuremath {\textbf{p}}})\) that is compatible and EIP-1559 stable with demand n, F, it holds that:

for all \(j \in [k]\).

Proof

If for some tier j it was \(\mathbb {E}\left[ T_j\right] < B_j\), which is possible by compatibility, EIP-1559 stability would imply that the price of that tier is zero. However, in this case any transaction would have positive utility from joining that tier. Since \(n > \sum _{j \in [k]} B_j\) this tier would have demand at least \(n - (\sum _{\ell \in [k]} B_{\ell } - B_j) > B_j\) and therefore would not be compatible.

In addition, we show the simple fact that for high prices, the demand is zero.

Lemma 1.2

For any blockchain \(({\ensuremath {\textbf{B}}}, {\ensuremath {\textbf{d}}}, {\ensuremath {\textbf{p}}})\) and regular load n, F, if \(p_j = 1\) then \(\mathbb {E}\left[ T_j\right] = 0\)

Proof

where the first inequality follows because for any transaction to enter tier j it’s utility needs to be non-negative and the last equality by the last two distributional assumptions (i.e., that \(v_0\) is distributed in [0, 1] and has zero probability of being equal to 1).

And a complementary result for low prices.

Lemma 1.3

For any blockchain \(({\ensuremath {\textbf{B}}}, {\ensuremath {\textbf{d}}}, {\ensuremath {\textbf{p}}})\) and regular load n, F, if \(p_j = 0\) then \(\sum _{j \in [k]}\mathbb {E}\left[ T_j\right] < B\)

Proof

If \(p_j = 0\) then almost surely every transaction would have positive utility in tier j, therefore would be included in some tier. The proof follows given that the arrival rate is higher then the throughput: \(n > B\).

Lemma 1.4

For any blockchain \(({\ensuremath {\textbf{B}}}, {\ensuremath {\textbf{d}}}, {\ensuremath {\textbf{p}}})\) and regular load n, F where \({\ensuremath {\textbf{p}}}\) is EIP-1559 stable, we have that

for all \(1 \le j < k\).

Proof

Suppose that for some \(1\le j < k\) we have that \(p_j < p_{j+1}\). In this case, tier j would have lower price and (by definition ) lower delay that tier \(j+1\). As such, we have that \(u(i, j) > u(i,j + 1)\) for any transaction i, leading to \(T_{j+1} = \emptyset \). However, \(p_{j+1} > p_{j} \ge 0\), leading to a contradiction as an empty tier must necessarily have zero price.

Remark 1.5

The previous result only holds if the price vector is EIP-1559. Compatibility alone is not enough, as tier j would be empty but it could be the case that \(T_j \le B_j\) if the \(p_j\) is still high enough.

We are now ready to prove our first result about the existence of prices. To avoid the cumbersome blockchain notation, we prove the following technical lemma about a continuous function f which exhibits all salient properties of the expected demands \(\mathbb {E}\left[ T_j\right] \) relative to the prices \({\ensuremath {\textbf{p}}}\), as proven with the previous lemmas. Essentially, f can be though of as the map from \({\ensuremath {\textbf{p}}}\) to \((\mathbb {E}\left[ T_1\right] , \mathbb {E}\left[ T_2\right] , \ldots , \mathbb {E}\left[ T_k\right] )\). The third property follows immediately: if a price of some tier increases, its demand decreases and the demand for other tiers cannot decrease. Due to space constraints we point to the full version of the paper of the proof.

Lemma 1.5

lema Let \(f : [0, 1]^k \rightarrow \mathbb {R}_{\ge 0}^k\) be a function with the following properties:

-

1.

\(f(x_1, \ldots , x_k)\) is uniformly continuous in \({\ensuremath {\textbf{x}}}\) and decreasing in \(x_j\) for \(j \in [k]\).

-

2.

If \(x_j = 1\), then \(f_j({\ensuremath {\textbf{x}}}) = 0\), where \(f_j\) is the \(j-th\) coordinate of \(f({\ensuremath {\textbf{x}}})\).

-

3.

If \(x_j = 0\) for some \(j \in [k]\) then:

$$\begin{aligned} \sum _{j \in [k]} f_j({\ensuremath {\textbf{x}}}) > B. \end{aligned}$$ -

4.

For \({\ensuremath {\textbf{y}}} = {\ensuremath {\textbf{x}}} + \delta \cdot {\ensuremath {\textbf{e}}}_j\) such that \({\ensuremath {\textbf{x}}}, {\ensuremath {\textbf{y}}} < 1\) we have that \(f_j({\ensuremath {\textbf{y}}}) < f_j({\ensuremath {\textbf{x}}})\) and \(f_\ell ({\ensuremath {\mathbf {~}}}\hbox {y)} \ge f_\ell ({\ensuremath {\textbf{x}}})\) for \(\ell \ne j\).

Then, for any \(B_1, B_2, \ldots , B_k > 0\) such that \(\sum _{j \in [k]} B_j = B\) there exists some \({\ensuremath {\textbf{x}}} \in [0, 1]^n\) such that:

for all \(j \in [k]\).

Putting it all together, we obtain our first result.

Theorem 1.3

For any blockchain with fixed \({\ensuremath {\textbf{B}}}\) and \({\ensuremath {\textbf{d}}}\) and any regular load n, F, there exists \({\ensuremath {\textbf{p}}}\) such that \(({\ensuremath {\textbf{B}}}, {\ensuremath {\textbf{d}}}, {\ensuremath {\textbf{p}}})\) is compatible with the load and EIP-1559 stable.

Knowing that compatible and EIP-1559 stable \({\ensuremath {\textbf{p}}}\) always exist for any \(({\ensuremath {\textbf{B}}}, {\ensuremath {\textbf{d}}})\), we are almost ready to prove that these prices are indeed unique. As a warmup to be used in the main proof, we show that if all prices increase, the aggregate demand cannot increase as well.

Lemma 1.6

Given \({\ensuremath {\textbf{B}}}, {\ensuremath {\textbf{d}}}\) and n, F and two different price vectors \({\ensuremath {\textbf{p}}} \ge {\ensuremath {\textbf{p}}}'\) (i.e., each price in \({\ensuremath {\textbf{p}}}\) is equal or higher than the corresponding in \({\ensuremath {\textbf{p}}}'\)), we have that

for all \(j \in [k]\).

Proof

Let S be the set of valuations that would lead to positive utility if included in their favorite tier of blockchain \(({\ensuremath {\textbf{B}}}, {\ensuremath {\textbf{d}}}, {\ensuremath {\textbf{p}}}')\). Clearly the utility of all of them would increase if they are included in \(({\ensuremath {\textbf{B}}}, {\ensuremath {\textbf{d}}}, {\ensuremath {\textbf{p}}})\) instead in the same tier. Defining \(S'\) similarly, we have that \(S' \subseteq S \Rightarrow \Pr \left[ S'\right] \le \Pr \left[ S\right] \). Since S (and \(S'\)) can be partitioned into disjoint sets \(S_j\) based on the preferred tier of each transaction such that \(\Pr \left[ S_j\right] = T_j\) multiplying by n gives us the claimed result.

Showing that the prices are unique builds upon and refines this lemma. Due to space constraints we point to the full version of the paper for the proof.

Theorem 1.4

For any blockchain with fixed \({\ensuremath {\textbf{B}}}\) and \({\ensuremath {\textbf{d}}}\) and any regular load n, F, if there exists \({\ensuremath {\textbf{p}}}\) such that if \(({\ensuremath {\textbf{B}}}, {\ensuremath {\textbf{d}}}, {\ensuremath {\textbf{p}}})\) is compatible with the load and EIP-1559 stable, then \({\ensuremath {\textbf{p}}}\) is unique.

This result provides some guarantee that as long as the tiers and delays are mostly fixed (or at the very least, change slowly and the first line of defense against changing demand are the fluctuating prices), any sensible price update oscillations.

Steady-State of the Tiered Pricing Mechanism

Under load n, F and fixed \({\ensuremath {\textbf{B}}}\), the Tiered Pricing mechanism aims to find a blockchain \(({\ensuremath {\textbf{B}}}, {\ensuremath {\textbf{d}}}, {\ensuremath {\textbf{p}}})\) such that:

where \((\lambda _j,\mu _j)_{j\in [k-1]}\) are the meta-parameters provided to the mechanism.

We show that it is always possible to find such delay and price combinations.

Theorem 1.5

For any \({\ensuremath {\textbf{B}}}\), factors \((\lambda _j,\mu _j)_{j\in [k-1]}\) and regular load n, F there exists a blockchain \(({\ensuremath {\textbf{B}}}, {\ensuremath {\textbf{d}}}, {\ensuremath {\textbf{p}}})\) which is compatible, EIP-1559 stable and satisfies Inequalities 1.7.

Proof

Set \(d_1 = 1\). Then, define

Essentially, \(d_{j+1}\) is sufficiently higher than \(d_j\) so that the discount factor incurred to almost all transactions is at least \(\lambda _j / 2\) smaller than for \(d_j\). We can capture this ‘almost all’ property with the following sets:

and \(H = \cap ^k_{j \ge 1} H_j\). The probability that in a sample of n transactions we observe none with discount functions outside of the set H is:

Therefore, \(d_{j+1}\) can be set high enough so that with probability at least \(1-\delta \) all transactions in a sample have discount functions such that consecutive tiers are at least \(\mu _j\) times less valuable.

Let \({\ensuremath {\textbf{p}}}\) be the compatible and EIP-1559 stable prices guaranteed to exist from Theorem 1.3, for the service levels \(d_1, d_2, \ldots , d_k\) that we just described. By Proposition 1.3 we know that each tier needs to be exactly full for these prices. Therefore, for any tier j there must exist a transaction with \(h \in H\) and \(v_0\) such that tier \(j+1\) is preferable to tier j and its utility is positive. Formally:

Using that the utility is positive (i.e., \(v_0\cdot h(d_{j+1}) - p_{j+1}> 0\) we continue:

Therefore, for the appropriately chosen service levels it is guaranteed that the prices will also follow our constraints.

The above theorem can be rephrased to refer to the ability of the Tiered Pricing mechanism to meet the diversity objectives (Definition 1.4) implied by Inequality 1.7.

Corollary 1.1

For any regular load n, F, any \(k\le B\), and any parameter set \(\{(a_j)_{j\in [k]},((\lambda _j, \mu _j))_{j\in [k-1]}\}\), where \(a_j\in (0,1],\lambda _j\in \mathbb {R}_{>1},\mu _j\in (0,1)\), and \(\sum _{j}a_i =1\), the Tiered Pricing mechanism with the same parameters and \({\ensuremath {k_{\textsf{active}}}},{\ensuremath {k_{\max }}}:=k\), \({\ensuremath {t_{\textsf{price}}}},{\ensuremath {t_{\textsf{delay}}}}<\infty \),\({\ensuremath {t_{\textsf{tier}}}}:=\infty \) is \(((d_i,p_i,a_i))_{i\in [k]}\)-diverse, for some \(((d_i,p_i))_{i\in [k]}\) that satisfy Inequalities 1.7.

Unfortunately, there are many pairs of \({\ensuremath {\textbf{p}}}\) and \({\ensuremath {\textbf{d}}}\) satisfying these properties. For example, the delay of the last tier can always be increased (lowering its corresponding price), while maintaining our guarantees. However, our tiered pricing mechanism finds a locally minimum solution, which does not unnecessarily inflate delays.

Theorem 1.6

For any \({\ensuremath {\textbf{B}}}\), parameters \((\lambda _j,\mu _j)_{j\in [k-1]}\) and regular load n, F there exists a blockchain \(({\ensuremath {\textbf{B}}}, {\ensuremath {\textbf{d}}}, {\ensuremath {\textbf{p}}})\) which is compatible, EIP-1559 stable and satisfies Inequalities 1.7. Moreover, no delay can be independently lowered without sacrificing any of the guarantees of Inequalities 1.7.

The proof is omitted, as it is similar to Theorem 1.3.

Appendix 3: Tiered Pricing Pseudocode

Rights and permissions

Copyright information

© 2024 The Author(s), under exclusive license to Springer Nature Switzerland AG

About this paper

Cite this paper

Kiayias, A., Koutsoupias, E., Lazos, P., Panagiotakos, G. (2024). Tiered Mechanisms for Blockchain Transaction Fees. In: Leonardos, S., Alfieri, E., Knottenbelt, W.J., Pardalos, P. (eds) Mathematical Research for Blockchain Economy. MARBLE 2024. Lecture Notes in Operations Research. Springer, Cham. https://doi.org/10.1007/978-3-031-68974-1_1

Download citation

DOI: https://doi.org/10.1007/978-3-031-68974-1_1

Published:

Publisher Name: Springer, Cham

Print ISBN: 978-3-031-68973-4

Online ISBN: 978-3-031-68974-1

eBook Packages: Economics and FinanceEconomics and Finance (R0)