Abstract

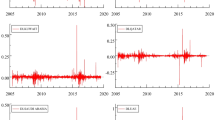

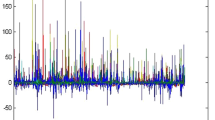

This study aims to analyze the Morgan Stanley Capital International (MSCI) world return and volatility of the healthcare price index using daily time series data. Since the data of MSCI healthcare returns cannot be described by linear models, the residual CUSUM GARCH(1,1) model is applied in this paper. The CUSUM test is used to estimate the optimal change point. The findings of this paper are (1) the estimated point is at day 1,201 of the entire daily data set of 4,209 observations; (2) if the change point is not taken into consideration, the estimated parameters of GARCH(1,1) become \(\hat{\gamma }_1+\hat{\beta }_1 \approx 1\), i.e., we encounter the “IGARCH effect”, which leads to an infinite variance for a model. The contribution of this paper is the recommendation for the analysis of the change point as the necessary condition, rather than jumping into using the whole data set to estimate all parameters of the model without testing nonlinearity, especially for financial time series data.

Access this chapter

Tax calculation will be finalised at checkout

Purchases are for personal use only

Similar content being viewed by others

Notes

- 1.

Developed markets countries are Australia, Austria, Belgium, Canada, Denmark, Finland, France, Germany, Hong Kong, Ireland, Israel, Italy, Japan, Netherlands, New Zealand, Norway, Portugal, Singapore, Spain, Sweden, Switzerland, the UK, and the US.

- 2.

References

Bollerslev, T., Chou, R.Y., Kroner, K.F.: ARCH modeling in finance: a review of the theory and empirical evidence. J. Econom. 52, 559 (1992)

Boonyanuphong, P., Sriboonchitta, S.: An Analysis of volatility and dependence between rubber spot and futures prices using copula-extreme value theory: implications for risk management. In: Huynh, V.N., Kreinovich, V., Sriboonchitta, S. (eds.) Modeling Dependence in Econometrics in Advances. Intelligent systems and computing, pp. 431–444. Springer, Heidenberg (2014)

Boonyanuphong, P., Sriboonchitta, S.: The impact of trading activity on volatility transmission and interdependence among agricultural commodity markets. Thai J. Math. pp. 211–227 (2014)

Carroll, R.J., Chen, X.: Mixing and moment properties of various GARCH and stochastic volatility models. Econom. Theory 18, 17–39 (2000)

Chevallier, J.: Detecting instability in the volatility of carbon prices. Energy Econ. 33, 99110 (2011)

Chinnakum, W., Sriboonchitta, S., Pastpipatkul, P.: Factors affecting economic output in developed countries: a copula approach to sample selection with panel data. Int. J. Approx. Reason. 54, 809–824 (2013)

Do, G.Q., Mcaleer, M., Sriboonchitta, S.: Effects of international gold market on stock exchange volatility: evidence from ASEAN emerging stock markets. Econ. Bull. 29, 599–610 (2009)

Kiatmanaroch, T., Sriboonchitta, S.: Dependence structure between world crude oil prices: evidence from NYMEX, ICE, and DME Markets. Thai J. Math. pp. 181–198 (2014)

Kiatmanaroch, T., Sriboonchitta, S.: Relationship between exchange rates, palm oil prices, and crude oil prices: a vine copula based GARCH approach: implications for risk management. In: Huynh, V.N., Kreinovich, V., Sriboonchitta, S. (eds.) Modeling Dependence in Econometrics in Advances, Intelligent systems and computing, pp. 399–413. Springer, Heidenberg (2014)

Lee, S., Lee, J.: Residual based cusum test for parameter change in AR-GARCH models. In: Huynh, V.N., Kreinovich, V., Sriboonchitta, S. (eds.) Modeling Dependence in Econometrics in Advances, Intelligent systems and computing pp. 101–110. Springer, Heidenberg (2014)

Lee, S., Tokutsu, Y., Maekawa, K.: The CUSUM test for parameter change in GARCH (1,1) model. ResearchGate (2000). doi:10.1080/03610920008832494

Lee, S., Ha, J., Na, O.: The CUSUM test for parameter change in time series models. Scand. J. Stat. 30, 781–790 (2003)

Neto, D.: The FMLS-based CUSUM statistic for testing the null of smooth time-varying cointegration in the presence of a structural break. Economics Letters 125, 208211 (2014)

Praprom, C., Sriboonchitta, S.: Dependence analysis of exchange rate and international trade of Thailand: application of vine copulas: implications for risk management. In: Huynh, V.N., Kreinovich, V., Sriboonchitta, S. (eds.) Modeling Dependence in Econometrics in Advances, Intelligent systems and computing, pp. 229–243. Springer, Heidenberg (2014)

Praprom, C., Sriboonchitta, S.: Extreme value copula analysis of dependence between exchange rates and exports of Thailand: implications for risk management. In: Huynh, V.N., Kreinovich, V., Sriboonchitta, S. (eds.) Modeling Dependence in Econometrics in Advances, Intelligent systems and computing pp. 187–199. Springer, Heidenberg (2014)

Puarattanaarunkorn, O., Sriboonchitta, S.: Analysis of volatility and dependence between the tourist arrivals from China to Thailand and Singapore: a copula-based GARCH approach : implications for risk management. In: Huynh, V.N., Kreinovich, V., Sriboonchitta, S. (eds.) Uncertainty Analysis in Econometrics with Applications, Intelligent Systems and Computing, pp. 283–294. Springer, Heidenberg (2014)

Puarattanaarunkorn, O., Sriboonchitta, S.: Copula based GARCH dependence model of Chinese and Korean tourist arrivals to Thailand: implications for risk management. In: Huynh, V.N., Kreinovich, V., Sriboonchitta, S. (eds.) Modeling Dependence in Econometrics in Advances, Intelligent systems and computing pp. 343–365. Springer, Heidenberg (2014)

Sims, C.A., Waggoner, D.F., Zha, T.: Methods for inference in large multiple-equation Markov-switching models. J. Econom. 146, 255–274 (2008)

Sirisrisakulchai, J., Sriboonchitta, S.: Modeling Dependence of Accident-Related Outcomes Using Pair Copula Constructions for Discrete Data: implications for risk management. In: Huynh, V.N., Kreinovich, V., Sriboonchitta, S. (eds.) Modeling Dependence in Econometrics in Advances, pp. 215–228. Heidenberg, Intelligent Systems and Computing, Springer (2014)

Tang, J., Sriboonchitta, S., Yuan, X.: A Mixture of Canonical Vine Copula GARCH Approach for Modeling Dependence of European Electricity Markets. Thai Journal of Mathematics, 165–180 (2014)

Wichian, A., Sirisrisakulchai, J., Sriboonchitta, S.: Copula based polychotomous choice selectivity model: application to occupational choice and wage determination of older workers: implications for risk management. In: Huynh, V.N., Kreinovich, V., Sriboonchitta, S., Suriya, K. (eds.) Econometrics of Risk, Intelligent systems and computing pp. 359–375. Springer, Heidenberg (2015)

Wichian, A., Sriboonchitta, S.: Econometric analysis of private and public wage determination for older workers using a copula and switching regression. Thai J. Math. pp. 111-128 (2014)

Xiongtoua, T., Sriboonchitta, S.: Analysis of volatility of and dependence between exchange Rate and inflation rate in Lao peoples democratic republic using copula-based GARCH approach: implications for risk management. In: Huynh, V.N., Kreinovich, V., Sriboonchitta, S. (eds.) Modeling Dependence in Econometrics in Advances, Intelligent Systems and Computing, pp. 201–214. Springer, Heidenberg (2014)

Acknowledgments

We are thankful to Professor Sangyeol Lee from Seoul National University, Department of Statistics, who inspired us by giving us the great idea of doing this research. Additionally, we then extend our gratitude to Miss Young Mai Lee, Professor Sangyeol Lee’s Ph.D. student, who designed the computational part correctly. We greatly appreciate the referees comments to improve our paper substantially. Furthermore, we are indebted to Professor Thierry Denoeux from Universit\(\acute{e}\) Technologie de Compi\(\grave{e}\)gne, who took the time to read this paper. Moreover, we are grateful to Lhoyd Castillo, the Customer Support Executive, Investment Management, from Thomson Reuters, who provided significant data for this work. Many thanks are extended to Puay Ungphakorn Center of Excellence in Econometrics, Faculty of Economics, Chiang Mai University.

Author information

Authors and Affiliations

Corresponding author

Editor information

Editors and Affiliations

Rights and permissions

Copyright information

© 2016 Springer International Publishing Switzerland

About this chapter

Cite this chapter

Thianpaen, N., Sriboonchitta, S. (2016). Analyzing MSCI Global Healthcare Return and Volatility with Structural Change Based on Residual CUSUM GARCH Approach. In: Huynh, VN., Kreinovich, V., Sriboonchitta, S. (eds) Causal Inference in Econometrics. Studies in Computational Intelligence, vol 622. Springer, Cham. https://doi.org/10.1007/978-3-319-27284-9_24

Download citation

DOI: https://doi.org/10.1007/978-3-319-27284-9_24

Published:

Publisher Name: Springer, Cham

Print ISBN: 978-3-319-27283-2

Online ISBN: 978-3-319-27284-9

eBook Packages: EngineeringEngineering (R0)