Abstract

Dynamic graphical models aim to describe the time-varying dependency structure of multiple time-series. In this article we review research focusing on the formulation and estimation of such models. The bulk of work in graphical structurelearning problems has focused in the stationary i.i.d setting, we present a brief overview of this work before introducing some dynamic extensions. In particular we focuson two classes of dynamic graphical model; continuous (smooth) models which are estimated via localised kernels, and piecewise models utilising regularisation based estimation. We give an overview of theoretical and empirical results regarding these models, before demonstrating their qualitative difference in the context of a real-world financial time-series dataset. We conclude with a discussion of the state of the field and future research directions.

D.B. Nelson—This work is funded by the Defence Science Technology Laboratory (Dstl) National PhD Scheme.

Access this chapter

Tax calculation will be finalised at checkout

Purchases are for personal use only

Similar content being viewed by others

Notes

- 1.

For simplicity, in this paper we assume the mean parameter is zero \(\varvec{\mu }=\varvec{0}\).

- 2.

Note: the model here refers to the sparsity pattern, rather than the fact that the distribution is Gaussian.

- 3.

Note: we set the first changepoint (denoted by \(k=0\)) at \(\tau _{0}=1\) and the last \(K+1\)st changepoint is located at \(\tau _{K+1}=T\).

- 4.

The matrix \(\varvec{\varSigma }^{o}\) is known as an oracle estimator, as it has access to the ground truth \(\varvec{\varSigma }_{*}\) through the risk function \(\mathcal {R}(\cdot )\).

- 5.

We note that Harcharoui et al. perform their changepoint analysis in a reformulated lasso problem rather than considering directly jumps in \(\hat{\varvec{u}}\) as presented here.

- 6.

In the univariate setting for functional approximation this is analogous to the fused lasso of Tibshirani et al. [40].

- 7.

If we choose \(\hat{\varvec{S}}^{t}\) to be estimated through a localised kernel as in (14) we obtain the SINGLE estimator of Monti et al. [32], if we use a Dirac delta kernel i.e. \(\hat{\varvec{S}}^{t}=\varvec{y}^{\top }\varvec{y}/2\) then we recover the IFGL estimator of our previous work [18]. Note: the TESLA approach of Ahmed et al. [1] uses a regulariser term like \(R_{\mathrm {IFGL}}\) but with a logistic loss function for binary variables.

- 8.

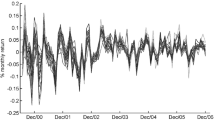

The data can be obtained from Ken French’s website http://mba.tuck.dartmouth.edu/pages/faculty/ken.french/data_library.html.

References

Ahmed, A., Xing, E.P.: Recovering time-varying networks of dependencies in social and biological studies. Proc. Natl. Acad. Sci. USA 106, 11878–11883 (2009)

Angelosante, D., Giannakis, G.B.: Sparse graphical modeling of piecewise-stationary time series. In: International Conference on Acoustics, Speech and Signal Processing (ICASSP) (2011)

Banerjee, O., Ghaoui, L.E., D’Aspremont, A.: Model selection through sparse maximum likelihood estimation for multivariate Gaussian or binary data. J. Mach. Learn. 9, 485–516 (2008)

Bleakley, K., Vert, J.P.: The group fused lasso for multiple change-point detection. Technical report HAL-00602121 (2011)

Boyd, S., Parikh, N., Chu, E.: Distributed optimization and statistical learning via the alternating direction method of multipliers. Found. Trends Mach. Learn. 3, 1–122 (2011)

Boyd, S., Vandenberghe, L.: Convex Optimization. Cambridge University Press (2004)

Cai, T., Liu, W., Luo X.: A constrained L1 minimization approach to sparse precision matrix estimation. J. Am. Stat. Assoc. (2011)

Carvalho, C.M., West, M.: Dynamic matrix-variate graphical models matrix-variate dynamic linear models. Bayesian Anal. 2, 69–97 (2007)

Cowell, R.G., Verrall, R.J., Yoon, Y.K.: Modelling operational risk with Bayesian networks. J. Risk Insur. 74, 795–827 (2007)

Danaher, P., Wang, P., Witten, D.M.: The joint graphical lasso for inverse covariance estimation across multiple classes. J. R. Stat. Soc. Ser. B (Stat. Methodol.) 76, 373–397 (2013)

Drton, M., Perlman, M.D.: Model selection for Gaussian concentration graphs. Biometrika 51, 591–602 (2004)

Enikeeva, F., Harchaoui, Z.: High-dimensional change-point detection with sparse alternatives (2013). arXiv:1312.1900

Foygel, R., Drton, M.: Extended Bayesian information criteria for Gaussian graphical models. In: Advances in Neural Information Processing Systems, vol. 23 (2010)

Friedman, J., Hastie, T., Tibshirani, R.: Sparse inverse covariance estimation with the graphical lasso. Biostatistics 9, 432–441 (2008)

Friedman, J., Hastie, T., Tibshirani, R.: Applications of the lasso and grouped lasso to the estimation of sparse graphical models (2010)

Gibberd, A.J., Nelson, J.D.B.: High dimensional changepoint detection with a dynamic graphical lasso. In: International Conference on Acoustics, Speech and Signal Processing (ICASSP) (2014)

Gibberd, A.J., Nelson, J.D.B.: Estimating multiresolution dependency graphs within the stationary wavelet framework. In: IEEE Global Conference on Signal and Information Processing (GlobalSIP) (2015)

Gibberd, A.J., Nelson, J.D.B.: Regularized estimation of piecewise constant Gaussian graphical models: the group-fused graphical lasso (2015). arXiv:1512.06171

Harchaoui, Z., Lévy-Leduc, C.: Multiple change-point estimation with a total variation penalty. J. Am. Stat. Assoc. 105, 1480–1493 (2010)

Hastie, T., Tibshirani, R.: Varying-coefficient models. J. R. Stat. Soc. B 55, 757–796 (1993)

Jordan, M.I.: Graphical models. Stat. Sci. 19, 140–155 (2004)

Kolar, M., Xing, E.P: On time varying undirected graphs. In: Proceedings of the International Conference on Artificial Intelligence and Statistics (AISTATS) (2011)

Kolar, M., Xing, E.P.: Estimating networks with jumps. Electron. J. Stat. 6, 2069–2106 (2012)

Lafferty, J., Liu, H., Wasserman, L.: Sparse nonparametric graphical models. Stat. Sci. 27, 519–537 (2012)

Lam, C., Fan, J.: Sparsistency and rates of convergence in large covariance matrix estimation. Ann. Stat. 37, 4254–4278 (2009)

Lauritzen, S.L.: Graphical Models. Oxford University Press, Oxford (1996)

Lèbre, S., Becq, J., Devaux, F., Stumpf, M.P.H., Lelandais, G.: Statistical inference of the time-varying structure of gene-regulation networks. BMC Syst. Biol. 4, 130 (2010)

Lee, J.D., Hastie, T.J.: Learning the structure of mixed graphical models. J. Comput. Graph. Stat. 24, 230–253 (2015)

Little, M.A., Jones, N.S.: Generalized methods and solvers for noise removal from piecewise constant signals. I. background theory. Proc. Math. Phys. Eng. Sci./R. Soc. 467, 3088–3114 (2011)

Loh, P., Wainwright, M.J.: Structure estimation for discrete graphical models: generalized covariance matrices and their inverses. In: Neural Information Processing Systems (NIPS) (2012)

Meinshausen, N., Bühlmann, P.: High-dimensional graphs and variable selection with the lasso. Ann. Stat. 34, 1436–1462 (2006)

Monti, R.P., Hellyer, P., Sharp, D., Leech, R., Anagnostopoulos, C., Montana, G.: Estimating time-varying brain connectivity networks from functional MRI time series. NeuroImage 103, 427–443 (2014)

Negahban, S.N., Ravikumar, P., Wainwright, M.J., Yu, B.: A unified framework for high-dimensional analysis of M-estimators with decomposable regularizers. Stat. Sci. 27, 538–557 (2012)

Ravikumar, P., Wainwright, M.J., Lafferty, J.D.: High-dimensional Ising model selection using \({l_1}\)-regularized logistic regression. Ann. Stat. 38, 1287–1319 (2010)

Ravikumar, P., Wainwright, M.J., Raskutti, G., Yu, B.: High-dimensional covariance estimation by minimizing \({l_1}\)-penalized log-determinant divergence. Electron. J. Stat. 5, 935–980 (2011)

Rothman, A.J., Bickel, P.J., Levina, E., Zhu, J.: Sparse permutation invariant covariance estimation. Electron. J. Stat. 2, 494–515 (2008)

Roy, S., Atchad, Y., Michailidis, G.: Change-point estimation in high-dimensional Markov random field models (2015). arXiv:1405.6176v2

Talih, M., Hengarter, N.: Structural learning with time-varying components: tracking the cross-section of financial time series. J. R. Stat. Soc. B 67, 321–341 (2005)

Tibshirani, R.: Regression shrinkage and selection via the lasso. J. R. Stat. Soc. Ser. B (Stat. Methodol.) 73, 273–282 (1996)

Tibshirani, R., Saunders, M., Rosset, S., Zhu, J., Knight, K.: Sparsity, smoothness via the fused lasso. J. R. Stat. Soc. Ser. B (Stat. Methodol.) 67, 91–108 (2005)

Wang, H.: Bayesian graphical lasso models and efficient posterior computation. Bayesian Anal. 7, 867–886 (2012)

Xuan, X., Murphy, K.: Modeling changing dependency structure in multivariate time series. In: International Conference on Machine Learning (2007)

Yang, E., Ravikumar, P.K., Allen, G.I., Liu, Z.: On Poisson graphical models. In: Advances in Neural Information Processing Systems (NIPS) (2013)

Yang, S., Pan, Z., Shen, X., Wonka, P., Ye, J.: Fused multiple graphical lasso (2012)

Yi-Ching, Y., Au, S.T.: Least-squares estimation of a step function. Indian J. Stat. Ser. A 51, 370–381 (1989)

Yuan, X.: Alternating direction method for covariance selection models. J. Sci. Comput. 51, 261–273 (2011)

Zhang, B., Geng, J., Lai, L.: Multiple change-points estimation in linear regression models via sparse group lasso. IEEE Trans. Signal Process. 63, 2209–2224 (2014)

Zhou, S., Lafferty, J., Wasserman, L.: Time varying undirected graphs. Mach. Learn. 80, 295–319 (2010)

Author information

Authors and Affiliations

Corresponding author

Editor information

Editors and Affiliations

Rights and permissions

Copyright information

© 2016 Springer International Publishing Switzerland

About this paper

Cite this paper

Gibberd, A.J., Nelson, J.D.B. (2016). Estimating Dynamic Graphical Models from Multivariate Time-Series Data: Recent Methods and Results. In: Douzal-Chouakria, A., Vilar, J., Marteau, PF. (eds) Advanced Analysis and Learning on Temporal Data. AALTD 2015. Lecture Notes in Computer Science(), vol 9785. Springer, Cham. https://doi.org/10.1007/978-3-319-44412-3_8

Download citation

DOI: https://doi.org/10.1007/978-3-319-44412-3_8

Published:

Publisher Name: Springer, Cham

Print ISBN: 978-3-319-44411-6

Online ISBN: 978-3-319-44412-3

eBook Packages: Computer ScienceComputer Science (R0)