Abstract

News is an important source of information for investment decision-making. Many studies analyzing listed companies in the US & Japan have been reported. However, the number of studies focusing on Korean stock markets is limited. This study analyzes the influence of news articles on Korean stock markets with high frequency trading data. Especially, we focus on analyses of the relationship between news articles and financial markets. Furthermore, we also analyze differences in market reactions according to language (English or Korean) of news articles and present three case studies.

Access this chapter

Tax calculation will be finalised at checkout

Purchases are for personal use only

Similar content being viewed by others

Notes

- 1.

- 2.

Source: The World Bank.

- 3.

Calculated from Korea Exchange (KRX) database and Nikkei Economic Electronic Databank System.

- 4.

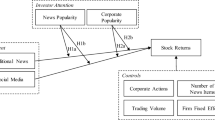

We previously showed that news articles have an impact on stock trading volume using the high frequency data of Samsung Electronics [21].

References

Antweiler, W., Frank, M.Z.: Is all that talk just noise? The information content of internet stock message boards. J. Financ. 59(3), 1259–1293 (2004)

Bishop, C.M.: Pattern Recognition and Machine Learning. Springer, Heidelberg (2006). https://doi.org/10.1007/978-1-4615-7566-5

Black, F., Scholes, M.: The pricing of options and corporate liabilities. J. Polit. Econ. 81(3), 637–654 (1973)

Campbell, J.Y., Lo, A.W., MacKinlay, A.C.: The Econometrics of Financial Markets. Princeton University Press, Princeton (1997)

Dougal, C., Engelberg, J., Garcia, D., Parsons, C.A.: Journalists and the stock market. Rev. Financ. Stud. 25(3), 639–679 (2012)

Engelberg, J., Reed, A.V., Ringgenberg, M.C.: How are shorts informed? Short sellers, news, and information processing. J. Financ. Econ. 105(2), 260–278 (2012)

Fama, E.: Efficient capital markets: a review of theory and empirical work. J. Financ. 25(2), 383–417 (1970)

Goshima, K., Takahashi, H.: Quantifying news tone to analyze Tokyo stock exchange with recursive neural networks. Secur. Anal. J. 54(3), 76–86 (2016)

Goshima, K., Takahashi, H., Terano, T.: Estimating financial words’ negative-positive from stock prices. In: The 21st International Conference Computing in Economics and Finance (2015)

Goshima, K., Takahashi, H.: Analyzing the relationship between news articles and high frequency trading data in Japanese stock markets. In: The 24th Annual Meeting - Nippon Finance Association (2016)

Ingersoll, J.E.: Theory of Financial Decision Making. Rowman & Littlefield, Lanham (1987)

Kim, Y.M., Willett, T.D.: News and the behavior of the Korean stock market during the global financial crisis. Korea World Econ. 15(3), 395–419 (2014)

Lee, D.W., Cho, J.H.: Stock price reactions to news and the momentum effect in the korean stock market. Asia-Pac. J. Financ. Stud. 43, 556–588 (2014)

Loughran, T., McDonald, B.: When is a liability not a liability? Textual analysis, dictionaries, and 10-Ks. J. Financ. 66(1), 35–65 (2011)

Luenberger, D.G.: Investment Science. Oxford University Press, Oxford (2000)

Sharpe, W.F.: Capital asset prices: a theory of market equilibrium under condition of risk. J. Financ. 19(3), 425–442 (1964)

Takahashi, H., Terano, T.: Agent-based approach to investors’ behavior and asset price fluctuation in financial markets. J. Artif. Soc. Soc. Simul. 6(3), 1–3 (2003)

Takahashi, H.: An analysis of the influence of dispersion of valuations on financial markets through agent-based modeling. Int. J. Inf. Technol. Decis. Mak. 11, 143–166 (2012)

Tetlock, P.C.: Giving content to investor sentiment: the role of media in the stock market. J. Financ. 62(3), 1139–1168 (2007)

Tetlock, P.C., Saar-Tsechansky, M., Macskassy, S.: More than words: quantifying language to measure firms fundamentals. J. Financ 63(3), 1437–1467 (2008)

Yoon, S.J., Suge A., Takahashi H.: JSAI International Symposia on AI, Workshop 3: Artificial Intelligence of and for Business (AI-Biz 2017)

Acknowledgements

This research was supported by a grant-in-aid from the Kayamori Foundation of Informational Science Advancement.

Author information

Authors and Affiliations

Corresponding author

Editor information

Editors and Affiliations

Rights and permissions

Copyright information

© 2018 Springer International Publishing AG, part of Springer Nature

About this paper

Cite this paper

Yoon, S., Suge, A., Takahashi, H. (2018). Do News Articles Have an Impact on Trading? - Korean Market Studies with High Frequency Data. In: Arai, S., Kojima, K., Mineshima, K., Bekki, D., Satoh, K., Ohta, Y. (eds) New Frontiers in Artificial Intelligence. JSAI-isAI 2017. Lecture Notes in Computer Science(), vol 10838. Springer, Cham. https://doi.org/10.1007/978-3-319-93794-6_9

Download citation

DOI: https://doi.org/10.1007/978-3-319-93794-6_9

Published:

Publisher Name: Springer, Cham

Print ISBN: 978-3-319-93793-9

Online ISBN: 978-3-319-93794-6

eBook Packages: Computer ScienceComputer Science (R0)