Abstract

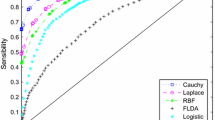

Support vector machines (SVM) from statistical learning theory are powerful classification methods with a wide range of applications including credit scoring. The urgent need to further boost classification performance in many applications leads the machine learning community into developing SVM with multiple kernels and many other combined approaches. Owing to the huge size of the credit market, even small improvements in classification accuracy might considerably reduce effective misclassification costs experienced by banks. Under certain conditions, the combination of different models may reduce or at least stabilize the risk of misclassification. We report on combining several SVM with different kernel functions and variable credit client data sets. We present classification results produced by various combination strategies and we compare them to the results obtained earlier with more traditional single SVM credit scoring models.

Access this chapter

Tax calculation will be finalised at checkout

Purchases are for personal use only

Preview

Unable to display preview. Download preview PDF.

Similar content being viewed by others

References

Duin, R.P.W. and Tax, D.M.J. (2000): Experiments with Classifier Combining Rules. In: Kittler, J. and Roli, F. (Eds.): MCS 2000, LNCS 1857. Springer, Berlin Heidelberg, 16–19

Kuncheva, L.I. (2004): Combining Pattern Classifiers: Methods and Algorithms. Wiley 2004

Schebeschc, K.B. and Stecking, R. (2005): Support Vector Machines for Credit Scoring: Extension to Non Standard Cases. In: Baier, D. and Wernecke, K.-D. (Eds.): Innovations in Classification, Data Science and Information Systems. Springer, Berlin, 498–505.

Schebesch, K.B. and Stecking, R. (2005): Support vector machines for credit applicants: detecting typical and critical regions. Journal of the Operational Research Society, 56(9), 1082–1088.

Schebesch, K.B. and Stecking, R. (2006): Selecting SVM Kernels and Input Variable Subset in Credit Scoring Models, submitted to Proceedings of the 30th Annual Conference of the GfKl 2006.

Stecking, R. and Schebesch, K.B. (2006): Comparing and Selecting SVMKernels for Credit Scoring. In: Spiliopoulou, M., Kruse, R., Borgelt, C., Nürnberger, A., Gaul, W. (Eds.): From Data and Information Analysis to Knowledge Engineering. Springer, Berlin, 542–549

Author information

Authors and Affiliations

Editor information

Editors and Affiliations

Rights and permissions

Copyright information

© 2007 Springer-Verlag Berlin Heidelberg

About this paper

Cite this paper

Stecking, R., Schebesch, K.B. (2007). Combining Support Vector Machines for Credit Scoring. In: Waldmann, KH., Stocker, U.M. (eds) Operations Research Proceedings 2006. Operations Research Proceedings, vol 2006. Springer, Berlin, Heidelberg. https://doi.org/10.1007/978-3-540-69995-8_23

Download citation

DOI: https://doi.org/10.1007/978-3-540-69995-8_23

Publisher Name: Springer, Berlin, Heidelberg

Print ISBN: 978-3-540-69994-1

Online ISBN: 978-3-540-69995-8

eBook Packages: Business and EconomicsBusiness and Management (R0)