Abstract

We study a dual-mode inventory management problem of a high-value component where the customer demand and the regular transportation lead time are stochastic, and the review periods of the two modes are different. The manufacturer is subject to a chance credit constraint that bounds the working capital. To solve the resulting chance-constrained stochastic optimization problem, we develop a hybrid simulation optimization algorithm that combines the modified nested partitions method as the global search framework, a feasibility detection procedure for chance constraint verification, and a \(\hbox {KN}{++}\) procedure as the final “cleanup” procedure to ensure solution quality. We are then able to analyze the impact of the chance credit constraint on the inventory policies and operational cost. Our numerical study shows that the effects of the reduction in mean or variance of the regular transportation lead time depend on whether the chance credit constraint is loose or tight. We show in this way that this tightness may lead to different mechanisms dominating the observed behavior. Further, we show that substantially extending the deterministic credit limit is less effective than having a slight increase in the probability parameter of the chance credit constraint.

Similar content being viewed by others

References

Alrefaei M, Andradóttir S (2005) Discrete stochastic optimization using variants of the stochastic ruler method. Nav Res Logist 52(4):344–360

Andradóttir S (1995) A method for discrete stochastic optimization. Manag Sci 41(12):1946–1961

Andradóttir S, Kim S (2010) Fully sequential procedures for comparing constrained systems via simulation. Nav Res Logist 57(5):403–421

Bashyam S, Fu M (1998) Optimization of \((s, S)\) inventory systems with random lead times and a service constraint. Manag Sci 44(12):243–256

Batur D, Kim S (2005) Procedures for feasibility detection in the presence of multiple constraints. In: Proceedings of the 2005 winter simulation conference, pp 692–698

Bendavid I, Herer Y, Yücesan E (2016) Inventory management under working capital constraints. J Simul. https://doi.org/10.1057/s41273-016-0030-0

Blancard S, Boussemart JP, Briec W, Kerstens K (2006) Short- and long-run credit constraints in French agriculture: a directional distance function framework using expenditure-constrained profit functions. Am J Agric Econ 88(2):351–364

Buzacott J, Zhang R (2004) Inventory management with asset-based financing. Manag Sci 50(9):1274–1292

Charnes A, Cooper W (1959) Chance-constrained programming. Manag Sci 6(1):73–79

Charnes A, Cooper W (1963) Deterministic equivalents for optimizing and satisficing under chance constraints. Oper Res 11(1):18–39

Chen C (1995) An effective approach to smartly allocate computing budget for discrete event simulation. In: Proceedings of the 34th IEEE conference on decision and control, vol 3, pp 2598–2603

Chen C (1996) A lower bound for the correct subset-selection probability and its application to discrete-event system simulations. IEEE Trans Autom Control 41(8):1227–1231

Chen C, He D, Fu M (2006) Efficient dynamic simulation allocation in ordinal optimization. IEEE Trans Autom Control 51(12):2005–2009

Chen C, He D, Fu M, Lee L (2008) Efficient simulation budget allocation for selecting an optimal subset. INFORMS J Comput 20(4):579–595

Chen C, Yücesan E, Dai L, Chen H (2010) Optimal budget allocation for discrete-event simulation experiments. IIE Trans 42(1):60–70

Feder G (1985) The relation between farm size and farm productivity. J Dev Econ 18:297–313

Fu M (2002) Optimization for simulation: theory vs. practice. INFORMS J Comput 14(3):192–215

Fu M, Hu J (1997) Conditional Monte Carlo: gradient estimation and optimization applications. Kluwer, Norwell

Glasserman P, Tayur S (1995) Sensitivity analysis for base-stock levels in multiechelon production–inventory systems. Manag Sci 41(2):263–281

Guariglia A, Mateut S (2016) External finance and trade credit extension in china: does political affiliation make a difference? Eur J Finance 22(4–6):319–344

Hartmann S, Briskorn D (2010) A survey of variants and extensions of the resource-constrained project scheduling problem. Eur J Oper Res 207(1):1–14

Hillier FS (1967) Chance-constrained programming with 0–1 or bounded continuous decision variabes. Manag Sci 14(1):34–57

Hong L, Nelson B (2006) Discrete optimization via simulation using COMPASS. Oper Res 54(1):115–129

Hong L, Nelson B (2007) A framework for locally convergent random-search algorithms for discrete optimization via simulation. ACM Trans Model Comput Simul 17(4):19:1–22

Janakiraman G, Roundy R (2004) Lost-sales problems with stochastic lead times: convexity results for base-stock policies. Oper Res 52(5):795–803

Kim S, Nelson B (2001) A fully sequential procedure for indifference-zone selection in simulation. ACM Trans Model Comput Simul 11(3):251–273

Kim S, Nelson B (2006a) On the asymptotic validity of fully sequential selection procedures for steady-state simulation. Oper Res 54(3):475–488

Kim S, Nelson B (2006b) Selecting the best system. In: Henderson S, Nelson B (eds) Handbooks in operations research and management science: simulation. Elsevier, Amsterdam, pp 501–534 (Chap. 13)

Kim S, Nelson B (2007) Recent advances in ranking and selection. In: Proceedings of the 2007 winter simulation conference, pp 692–698

Law AM, Kelton WD (2000) Simulation modeling and analysis. McGraw-Hill series in industrial engineering and management science. McGraw-Hill, New York

Lejeune M, Ruszczyński A (2007) An efficient trajectory method for probabilistic production–inventory–distribution problems. Oper Res 55(2):378–394

Liu S, Wang C (2009) Two-stage profit optimization model for linear scheduling problems considering cash flow. Constr Manag Econ 27(11):1023–1037

Luedtke J (2013) A branch-and-cut decomposition algorithm for solving general chance-constrained mathematical programs with finite support. Math Program 138:223–251

Luedtke J, Ahmed S (2008) A sample approximation approach for optimization with probabilistic constraints. SIAM J Optim 19(2):674–699

Luedtke J, Ahmed S, Nemhauser G (2010) An integer programming approach for linear programs with probabilistic constraints. Math Program 122(2):247–272

Malone G, Kim S, Goldsman D, Batur D (2005) Performance of variance updating ranking and selection procedures. In: Proceedings of the 2005 winter simulation conference, pp 825–832

Miller B, Wagner H (1965) Chance constrained programming with joint constraints. Oper Res 13(6):930–945

Minner S (2003) Multiple-supplier inventory models in supply chain management: a review. Int J Prod Econ 81–82:265–279

Moinzadeh K, Nahmias S (1988) A continuous review model for an inventory system with two supply modes. Manag Sci 34(6):761–773

Murr M, Prekopa A (2000) Solution of a product substitution problem using stochastic programming. Nonconv Optim Appl 49:252–271

Nelson B, Swann J, Goldsman D, Song W (2001) Simple procedures for selecting the best simulated system when the number of alternatives is large. Oper Res 49(6):950–963

Nemirovski A, Shapiro A (2006a) Convex approximations of chance constrained programs. SIAM J Optim 17(4):969–996

Nemirovski A, Shapiro A (2006b) Scenario approximations of chance constraints. In: Calafiore G, Dabbene F (eds) Probabilistic and randomized methods for design under uncertainty. Springer, Berlin, pp 3–47 (Chap. 1)

Ólafsson S, Yang J (2005) Intelligent partitioning for feature selection. INFORMS J Comput 17(3):339–355

Olson D, Swenseth S (1987) A linear approximation for chance-constrained programming. J Oper Res Soc 38(3):261–267

Pagnoncelli B, Ahmed S, Shapiro A (2009) Sample average approximation method for chance constrained programming: theory and applications. J Optim Theory Appl 41(2):263–281

Pichitlamken J, Nelson B (2003) A combined procedure for optimization via simulation. ACM Trans Model Comput Simul 13(2):155–179

Poojari C, Varghese B (2008) Genetic algorithms based technique for solving chance constraint problems. Eur J Oper Res 185(3):1128–1154

Ramasesh RV, Ord JK, Hayya JC, Pan A (1991) Sole versus dual sourcing in stochastic lead-time \((s, q)\) inventory models. Manag Sci 37(4):428–443

Reindorp M, Lange A, Tanrisever F (2013) Pre-shipment financing: credit capacities and supply chain consequences. Technical report, Eindhoven University of Technology, Eindhoven

Robbins H, Monro S (1951) A stochastic approximation method. Ann Math Stat 22(3):400–407

Scheller-Wolf A, Veeraraghavan S, van Houtun G (2007) Effective dual sourcing with a single index policy. Technical report, Carnegie-Mellon University, Pittsburgh

Sculli D, Wu S (1981) Stock control with two suppliers and normal lead times. Int J Oper Res Soc 32(11):1003–1009

Seppala Y (1971) Constructing sets of uniformly tighter linear approximations for a chance constraint. Manag Sci 17(11):736–749

Sheopuri A, Janakiraman G, Seshadri S (2010) New policies for the stochastic inventory control problem with two supply sources. Oper Res 58(3):734–745

Shi L, Ólafsson S (2000a) Nested partitions method for global optimization. Oper Res 48(3):390–407

Shi L, Ólafsson S (2000b) Nested partitions method for stochastic optimization. Methodol Comput Appl Probab 2(3):271–291

Shi L, Olafsson S (2007) Nested partitions optimization. Tutor Oper Res 29:1–22

Shi L, Ólafsson S (2008) Nested partitions method, theory and applications. Springer, Berlin

Shi L, Ólafsson S, Sun N (1999) New parallel randomized algorithms for the traveling salesman problem. Comput Oper Res 26(4):371–394

Swenson D (2011) The influence of Chinese trade policy on automobile assembly and parts (October 25, 2011). CESifo working paper series no. 3615. http://ssrn.com/abstract=1949070

Swisher J, Jacobson S, Yücesan E (2003) Discrete-event simulation optimization using ranking, selection, and multiple comparison procedures: a survey. ACM Trans Model Comput Simul 13(2):134–154

Swisher J, Hyden P, Jacobson S, Schruben L (2004) A survey of recent advances in discrete input parameter discrete-event simulation optimization. IIE Trans 36(6):591–600

Talluri S, Narasimhan R, Nair A (2006) Vendor performance with supply risk: a chance-constrained DEA approach. Int J Prod Econ 100(2):212–222

Tanrisever F, Cetinay H, Reidorp M, Fransoo J (2012) The value of reverse factoring in multi-stage supply chains. Technical report, Eindhoven University of Technology, Eindhoven

Veeraraghavan S, Scheller-Wolf A (2008) Now or later: a simple policy for effective dual sourcing in capacitated systems. Oper Res 56(4):850–864

Vlachos D, Tagaras G (2001) An inventory system with two supply modes and capacity constraints. Int J Prod Econ 72(1):41–58

Wu D, Olson D (2008) Supply chain risk, simulation, and vendor selection. Int J Prod Econ 114(2):646–655

Xu J, Nelson B, Hong J (2010) Industrial strength COMPASS: a comprehensive algorithm and software for optimization via simulation. ACM Trans Model Comput Simul 20(1):3

Zhang H, Shi L, Meyer R, Nazareth D, D’Souza W (2009) Solving beam-angle selection and dose optimization simultaneously via high-throughput computing. INFORMS J Comput 21(3):427–444

Zhao L, Langendoen F, Fransoo J (2012) Supply management of high-value components with a credit constraint. Flex Serv Manuf J 24(2):100–118

Acknowledgements

The research is partially funded by the National Natural Science Foundation of China under Projects No. 70771053.

Author information

Authors and Affiliations

Corresponding author

Appendices

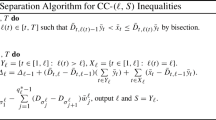

Nested partitions method

The nested partitions method is described in Algorithm 4.

Solutions in contour plots

In the following, we show the solutions of the hybrid algorithm in contour plots corresponding to \(\alpha = 2\%\) and \(\alpha = 5\%\) in Figs. 10, 11, which are similar to Fig. 2 except different locations of the solution points. In addition, we provide the summary of results of the solutions and the corresponding objective function values of the hybrid algorithm in Table 7.

Solutions in contour plots: \(\alpha = 2\%\)

Solutions in contour plots: \(\alpha = 5\%\)

Empirical distribution of the over-limit credit

We further examine the empirical distribution of the “realized credits” in the numerical examples. In particular, we evaluate one optimal solution of our base model (without a credit cap) for \(\alpha = 0.01, 0.02, 0.05, 0.10\), respectively, and present the histograms of the over-limit credit (i.e., \(\max (-\mathcal {P}(t) - \tau , 0)\)) observed in 1000 simulation replications in Fig. 12. It shows that, although our base model does not explicitly enforce a cap on the over-limit credit, the over-limit credit is still bounded to some extent. We further observe that a tighter chance credit constraint results in lower credit line.

Histograms of the over-limit credit with different \(\alpha \) values

The negative cash position is computed according to Eq. (13). The pipeline inventory and on-hand inventory in consecutive periods are correlated. Therefore, the negative cash positions in consecutive periods are also correlated. If the negative cash position is extremely high in one period, it is also likely to be high in the surrounding periods, which altogether increase the overall chance to violate the credit limit \(\tau \).

Rights and permissions

About this article

Cite this article

Chen, Q., Zhao, L., Fransoo, J.C. et al. Dual-mode inventory management under a chance credit constraint. OR Spectrum 41, 147–178 (2019). https://doi.org/10.1007/s00291-018-0532-4

Received:

Accepted:

Published:

Issue Date:

DOI: https://doi.org/10.1007/s00291-018-0532-4