Abstract

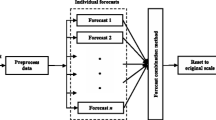

Modeling and forecasting of time series data are integral parts of many scientific and engineering applications. Increasing precision of the performed forecasts is highly desirable but a difficult task, facing a number of mathematical as well as decision-making challenges. This paper presents a novel approach for linearly combining multiple models in order to improve time series forecasting accuracy. Our approach is based on the assumption that each future observation of a time series is a linear combination of the arithmetic mean and median of the forecasts from all participated models together with a random noise. The proposed ensemble is constructed with five different forecasting models and is tested on six real-world time series. Obtained results demonstrate that the forecasting accuracies are significantly improved through our combination mechanism. A nonparametric statistical analysis is also carried out to show the superior forecasting performances of the proposed ensemble scheme over the individual models as well as a number of other forecast combination techniques.

Similar content being viewed by others

References

De Gooijer JG, Hyndman RJ (2006) 25 years of time series forecasting. J Forecast 22(3):443–473

Zhang GP (2007) A neural network ensemble method with jittered training data for time series forecasting. Inform Sci 177(23):5329–5346

Box GEP, Jenkins GM (1970) Time series analysis, forecasting and control, 3rd edn. Holden-Day, California

Andrawis RR, Atiya AF, El-Shishiny H (2011) Forecast combinations of computational intelligence and linear models for the NN5 time series forecasting competition. Int J Forecast 27(3):672–688

Lemke C, Gabrys B (2010) Meta-learning for time series forecasting and forecast combination. Neurocomputing 73:2006–2016

Clemen RT (1989) Combining forecasts: a review and annotated bibliography. J Forecast 5(4):559–583

Jose VRR, Winkler RL (2008) Simple robust averages of forecasts: some empirical results. Int J Forecast 24(1):163–169

Armstrong JS (2001) Principles of forecasting: a handbook for researchers and practitioners. Academic Publishers, Norwell, MA

Stock JH, Watson MW (2004) Combination forecasts of output growth in a seven-country data set. J Forecast 23:405–430

Larreche JC, Moinpour R (1983) Managerial judgment in marketing: the concept of expertise. J Market Res 20:110–121

Agnew C (1985) Bayesian consensus forecasts of macroeconomic variables. J Forecast 4:363–376

McNees SK (1992) The uses and abuses of ‘consensus’ forecasts. J Forecast 11:703–711

Crane DB, Crotty JR (1967) A two-stage forecasting model: exponential smoothing and multiple regression. J Manage Sci 13:B501–B507

Zarnowitz V (1967) An appraisal of short-term economic forecasts. National Bureau of Econ Res, New York

Reid DJ (1968) Combining three estimates of gross domestic product. J Economica 35:431–444

Bates JM, Granger CWJ (1969) Combination of forecasts. J Oper Res Q 20:451–468

Granger CWJ, Ramanathan R (1984) Improved methods of combining forecasts. J Forecast 3:197–204

Granger CWJ, Newbold P (1986) Forecasting economic time series, 2nd edn. Academic Press, New York

Aksu C, Gunter S (1992) An empirical analysis of the accuracy of SA, OLS, ERLS and NRLS combination forecasts. Int J Forecast 8:27–43

Newbold P, Granger CWJ (1974) Experience with forecasting univariate time series and the combination of forecasts (with discussion). J R Stat Soc A 137(2):131–165

Winkler RL, Makridakis S (1983) The combination of forecasts. J R Stat Soc A 146(2):150–157

Pollock DSG (1993) Recursive estimation in econometrics. Comput Stat Data An 44:37–75

Bunn D (1975) A Bayesian approach to the linear combination of forecasts. J Oper Res Q 26:325–329

Zhang GP (2003) Time series forecasting using a hybrid ARIMA and neural network model. Neurocomputing 50:159–175

Khashei M, Bijari M (2010) An artificial neural network (p, d, q) model for time series forecasting. J Expert Syst Appl 37(1):479–489

Khashei M, Bijari M (2011) A novel hybridization of artificial neural networks and ARIMA models for time series forecasting. J Appl Soft Comput 11:2664–2675

Adhikari R, Agrawal RK (2012) A novel weighted ensemble technique for time series forecasting. In: Proceedings of the 16th Pacific-Asia conference on knowledge discovery and data mining (PAKDD), Kuala Lumpur, Malaysia, pp 38–49

Winkler RL, Clemen RT (1992) Sensitivity of weights in combining forecasts. Oper Res 40(3):609–614

Tseng FM, Yu HC, Tzeng GH (2002) Combining neural network model with seasonal time series ARIMA model. J Technol Forecast Soc Change 69:71–87

Vapnik V (1995) The nature of statistical learning theory. Springer, New York

Suykens JAK, Vandewalle J (1999) Least squares support vector machines classifiers. Neural Process Lett 9(3):293–300

Hamzaçebi C, Akay D, Kutay F (2009) Comparison of direct and iterative artificial neural network forecast approaches in multi-periodic time series forecasting. J Expert Syst Appl 36(2):3839–3844

Gheyas IA, Smith LS (2011) A novel neural network ensemble architecture for time series forecasting. Neurocomputing 74(18):3855–3864

Lim CP, Goh WY (2005) The application of an ensemble of boosted Elman networks to time series prediction: a benchmark study. J Comput Intel 3(2):119–126

Chapelle O (2002) Support vector machines: introduction principles, adaptive tuning and prior knowledge. Ph.D. Thesis, University of Paris, France

Demuth H, Beale M, Hagan M (2010) Neural network toolbox user’s guide. The MathWorks, Natic, MA

Hyndman RJ (2011) Time series data library (TSDL), http://robjhyndman.com/TSDL/

Hollander M, Wolfe DA (1999) Nonparametric statistical methods. Wiley, Hoboken, NJ

Acknowledgments

The authors are thankful to the reviewers for their constructive suggestions which significantly facilitated the quality improvement of this paper. In addition, the first author likes to express his profound gratitude to the Council of Scientific and Industrial Research (CSIR), India, for the obtained financial support in performing this research work.

Author information

Authors and Affiliations

Corresponding author

Rights and permissions

About this article

Cite this article

Adhikari, R., Agrawal, R.K. A linear hybrid methodology for improving accuracy of time series forecasting. Neural Comput & Applic 25, 269–281 (2014). https://doi.org/10.1007/s00521-013-1480-1

Received:

Accepted:

Published:

Issue Date:

DOI: https://doi.org/10.1007/s00521-013-1480-1