Abstract

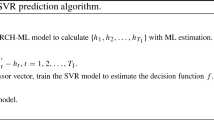

The support vector regression (SVR) is a supervised machine learning technique that has been successfully employed to forecast financial volatility. As the SVR is a kernel-based technique, the choice of the kernel has a great impact on its forecasting accuracy. Empirical results show that SVRs with hybrid kernels tend to beat single-kernel models in terms of forecasting accuracy. Nevertheless, no application of hybrid kernel SVR to financial volatility forecasting has been performed in previous researches. Given that the empirical evidence shows that the stock market oscillates between several possible regimes, in which the overall distribution of returns it is a mixture of normals, we attempt to find the optimal number of mixture of Gaussian kernels that improve the one-period-ahead volatility forecasting of SVR based on GARCH(1,1). The forecast performance of a mixture of one, two, three and four Gaussian kernels are evaluated on the daily returns of Nikkei and Ibovespa indexes and compared with SVR–GARCH with Morlet wavelet kernel, standard GARCH, Glosten–Jagannathan–Runkle (GJR) and nonlinear EGARCH models with normal, student-t, skew-student-t and generalized error distribution (GED) innovations by using mean absolute error (MAE), root mean squared error (RMSE) and robust Diebold–Mariano test. The results of the out-of-sample forecasts suggest that the SVR–GARCH with a mixture of Gaussian kernels can improve the volatility forecasts and capture the regime-switching behavior.

Similar content being viewed by others

References

Alexander C, Lazar E (2006) Normal mixture GARCH(1,1): applications to exchange rate modelling. J Appl Econom 21(3):307–336

Arlot S, Celisse A (2010) A survey of cross-validation procedures for model selection. Stat Surv 4:40–79

Bae GI, Kim WC, Mulvey JM (2014) Dynamic asset allocation for varied financial markets under regime switching framework. Eur J Oper Res 234(2):450–458

Bai X, Russell JR, Tiao GC (2003) Kurtosis of GARCH and stochastic volatility models with non-normal innovations. J Econom 114(2):349–360

Bollerslev T (1986) Generalized autoregressive conditional heteroskedasticity. J Econom 31:307–327

Brailsford TJ, Faff RW (1996) An evaluation of volatility forecasting techniques. J Bank Finance 20:419–438

Brooks C (2001) A Double-threshold GARCH Model for the French Franc/Deutschmark exchange rate. J Forecast 20(2):135–143

Brooks C, Persand G (2003) Volatility forecasting for risk management. J Forecast 22(1):1–22

Brownlees CT, Gallo GM (2009) Comparison of volatility measures: a risk management perspective. J Financial Econom 8(1):29–56

Cao L, Tay F (2003) Support vector machine with adaptive parameters in financial time series forecasting. IEEE Trans Neural Netw 14(6):1506–1518

Cao L, Tay FE (2001) Financial forecasting using support vector machines. Neural Comput Appl 10(2):184–192

Casella G, Berger RL (2001) Statistical inference, 2nd edn. Duxbury Press, California

Cavalcante RC, Brasileiro RC, Souza VL, Nobrega JP, Oliveira AL (2016) Computational intelligence and financial markets: a survey and future directions. Expert Syst Appl 55:194–211

Chen S, Härdle WK, Jeong K (2010) Forecasting volatility with support vector machine-based GARCH model. J Forecast 433(29):406–433

Cherkassky V, Ma Y (2004) Practical selection of SVM parameters and noise estimation for SVM regression. Neural Netw 17(1):113–126

Choudhry T, Wu HAO (2008) Forecasting ability of GARCH vs Kalman filter method: evidence from Daily UK Time-Varying Beta. J Forecast 689:670–689

Diebold FX, Mariano RS (1995) Comparing predictive accuracy. J Bus Econ Stat 13(3):253–263

Engle RF (1982) Autoregressive conditional Heteroscedasticity with estimates of the variance of United Kingdom inflation. Econometrica 50(4):987–1007

Fernandez C, Steel MFJ (1998) On Bayesian modeling of fat tails and skewness. J Am Stat Assoc 93(441):359

Fernando P-C, Afonso-Rodríguez JA, Giner J (2003) Estimating GARCH models using support vector machines. Quant Finance 3:1–10

Franses PH, van Dijk D (1996) Forecasting stock market volatility using (non-linear) Garch models. J Forecast 15(3):229–235

Gavrishchaka VV, Banerjee S (2006) Support vector machine as an efficient framework for stock market volatility forecasting. Comput Manag Sci 3(2):147–160

Gavrishchaka VV, Ganguli SB (2003) Volatility forecasting from multiscale and high-dimensional market data. Neurocomputing 55(1–2):285–305

Glosten LR, Jagannthan R, Runkle DE (1993) On the relation between the expected value and the volatility of the nominal excess return on stocks. J Finance 48(5):1779–1801

Guidolin M (2011) Markov switching models in empirical finance. In: Drukker DM (ed) Missing data methods: time-series methods and applications (advances in econometrics), vol 27. Emerald Group Publishing Limited, UK, pp 1–86

Haas M, Mittnik S, Paolella MS (2004) Mixed normal conditional heteroskedasticity. J Financial Econom 2(2):211–250

Hansen PR, Lunde A (2005) A forecast comparison of volatility models: does anything beat a GARCH(1,1)? J Appl Econom 20(7):873–889

Haykin S (1998) Neural networks: a comprehensive foundation, 2nd edn. Prentice Hall, New York (ISBN-10: 0132733501, ISBN-13: 978-0132733502)

Huang, C., Gao, F., Jiang, H., 2014. Combination of biorthogonal wavelet hybrid kernel OCSVM with feature weighted approach based on EVA and GRA in financial distress prediction. In: Mathematical problems in Engineering 2014

Hyndman RJ, Koehler AB (2006) Another look at measures of forecast accuracy. Int J Forecast 22(4):679–688

Jorion P (1995) Predicting volatility in the foreign exchange market. J Finance 50(2):507–528

Karush W (1939) Minima of functions of several variables with inequalities as side constraints. Ph.D. thesis, University of Chicago

Kohavi R (1995) A study of cross-validation and bootstrap for accuracy estimation and model selection. In: Proceedings of the 14th international joint conference on artificial intelligence, vol 14. Morgan Kaufmann Publishers Inc., Monreal, pp 1137–1143

Kuhn HW, Tucker A (1951) Nonlinear programming. University of California Press, California

Levy M, Kaplanski G (2015) Portfolio selection in a two-regime world. Eur J Oper Res 242(2):514–524

Li Y (2014) Estimating and forecasting APARCH-Skew- t model by wavelet support vector machines. J Forecast 269(March):259–269

Marcucci J (2005) Forecasting stock market volatility with regime-switching GARCH models. Stud Nonlinear Dyn Econom 9(4):1–55

Marron JS, Wand M (1992) Exact mean integrated squared error. Ann Stat 20(2):712–736

McLachlan G, Peel D (2004) Finite mixture models. Wiley, Canada

Mcmillan DG, Speight A (2000) Forecasting UK stock market volatility. Appl Financial Econ 10:435–448

Mercer J (1909) Functions of positive and negative type and their connection with the theory of integral equations. Philos Trans R Soc Lond 209(A):415–446

Nelson DB (1991) Conditional heteroskedasticity in asset returns: a new approach. Econometrica 59(2):347–370

Newey WK, West KD (1987) A simple, positive semi-definite, heteroskedasticity and autocorrelation consistent covariance matrix. Econometrica 55:703–708

Ou P, Wang H (2013) Volatility modelling and prediction by hybrid support vector regression with chaotic genetic algorithms. Int Arab J Inf Technol 11(3):287–292

Patton AJ (2011) Volatility forecast comparison using imperfect volatility proxies. J Econ 160(1):246–256

Poon SH, Granger CW (2003) Forecasting volatility in financial markets: a review. J Econ Lit 41(2):478–539

Sangeetha R, Kalpana B (2010) A comparative study and choice of an appropriate kernel for support vector machines. In: Information and communication technologies, pp 549–553

Santamaría-Bonfil G, Frausto-Solís J, Vázquez-Rodarte I (2015) Volatility forecasting using support vector regression and a hybrid genetic algorithm. Comput Econ 45:111–133

Sapankevych NI, Sankar R (2009) Time series prediction using support vector machines: a survey. IEEE Comput Intell Mag 4(2):24–38

Sermpinis G, Stasinakis C, Theofilatos K, Karathanasopoulos A (2014) Inflation and unemployment forecasting with genetic support vector regression. J Forecast 33(6):471–487

Shalev-shwartz S, Ben-david S (2014) Understanding machine learning: from theory to algorithms. Cambridge University Press, New York

Smola AJ, Schölkopf B (2004) A tutorial on support vector regression. Stat Comput 14:199–222

Stone M (1974) Cross-validatory choice and assessment of statistical predictions. J R Stat Soc 36(2):111–147

Tang L-B, Sheng H-Y, Tang L-X (2009a) GARCH prediction using spline wavelet support vector machine. Neural Comput Appl 18(8):913–917

Tang L-B, Tang L-X, Sheng H-Y (2009b) Forecasting volatility based on wavelet support vector machine. Expert Syst Appl 36(2):2901–2909

Tsay RS (2010) Analysis of financial time series, 3rd edn, vol 48. Wiley, Newyork

Tu J (2010) Is regime switching in stock returns important in portfolio decisions? Manag Sci 56(7):1198–1215

Vapnik VN (1995) The nature of statistical learning theory. Springer, Berlin

Vapnik VN, Chervonenkis AY (1974) Theory of pattern recognition: statistical problems of learning. Nauka, Moscow

Wang B, Huang H, Wang X (2011) A support vector machine based MSM model for financial short-term volatility forecasting. Neural Comput Appl 22(1):21–28

Wang J, Taaffe MR (2015) Multivariate mixtures of normal distributions: properties, random vector generation, fitting, and as models of market daily changes. INFORMS J Comput 27(2):193–203

Wirjanto TS, Xu D (2009) The applications of mixtures of normal distributions in empirical finance: a selected survey, Working paper 0904. University of Waterloo, Department of Economics. http://economics.uwaterloo.ca/documents/mn-review-paper-CES.pdf

Zhang L, Zhou W, Jiao L (2004) Wavelet support vector machine. IEEE Trans Syst Man Cybern Part B 34(1):34–39

Author information

Authors and Affiliations

Corresponding author

Rights and permissions

About this article

Cite this article

Bezerra, P.C.S., Albuquerque, P.H.M. Volatility forecasting via SVR–GARCH with mixture of Gaussian kernels. Comput Manag Sci 14, 179–196 (2017). https://doi.org/10.1007/s10287-016-0267-0

Received:

Accepted:

Published:

Issue Date:

DOI: https://doi.org/10.1007/s10287-016-0267-0