Abstract

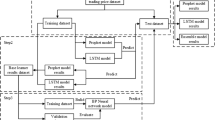

Several countries have formulated carbon–neutral plans in dealing with global warming, which have also derived various carbon trading markets. All parties involved in carbon trading aim to obtain the maximum benefit from it, and this requires participants to accurately judge the carbon trading price. This study then proposes a two-stage heterogeneous ensemble method for predicting carbon trading prices. To accurately capture the characteristics of the time series data, we extracted four feature sets based on the lag length, moving average, variational mode decomposition, and empirical mode decomposition methods. Subsequently, four algorithms, linear regression, neural network, random forest, and XGBoost, constructed the first-layer model. We used a neural network algorithm to build the second-layer model to enhance the predictive model fit. Moreover, we used the particle swarm optimization algorithm to optimize the crucial parameters involved in the model. Extensive numerical experiments were conducted on carbon trading data from the Beijing carbon trading market in the past five years (2016–2021), and showed that our proposed method is superior to other popular methods such as LightGBM, support vector machine, and k-nearest neighbor.

Similar content being viewed by others

Notes

https://www.c2es.org/content/extreme-weather-and-climate-change/. Access date: 2021/10/31.

https://www.un.org/en/chronicle/article/small-islands-rising-seas. Access date: 2021/10/31.

https://en.wikipedia.org/wiki/United_Nations_Framework_Convention_on_Climate_Change. Access date: 2021/10/31.

https://en.wikipedia.org/wiki/Kyoto_Protocol. Access date: 2021/10/31.

https://en.wikipedia.org/wiki/2015_United_Nations_Climate_Change_Conference. Access date: 2021/10/31.

References

Abdar, M., Zomorodi-Moghadam, M., Zhou, X., Gururajan, R., Tao, X., Barua, P. D., & Gururajan, R. (2018). A new nested ensemble technique for automated diagnosis of breast cancer. Pattern Recognition Letters. https://doi.org/10.1016/J.PATREC.2018.11.004

Abedin, M. Z., Hasan, M. M., Hassan, M. K., & Petr, H. (2021). Deep learning-based exchange rate prediction during the COVID–19. Annals of Operations Research. https://doi.org/10.1007/s10479-021-04420-6

Abedin, M. Z., Chi, G., Moula, F. E., Azad, A. S. M. S., & Khan, M. S. U. (2019). Topological applications of multilayer perceptrons and support vector machine in financial decision support systems. International Journal of Finance & Economics, 24, 474–507.

Alameer, Z., Elaziz, M. A., Ewees, A. A., Ye, H., & Jianhua, Z. (2019). Forecasting gold price fluctuations using improved multilayer perceptron neural network and whale optimization algorithm. Resources Policy, 61, 250–260.

Cui, S., Qiu, H., Wang, S., & Wang, Y. (2021a). Two-stage stacking heterogeneous ensemble learning method for gasoline octane number loss prediction. Applied Soft Computing, 113, 107989.

Cui, S., Wang, Y., Wang, D., Sai, Q., Huang, Z., & Cheng, T. C. E. (2021b). A two-layer nested heterogeneous ensemble learning predictive method for COVID-19 mortality. Applied Soft Computing, 113, 107946.

Cui, S., Wang, Y., Yin, Y., Cheng, T. C. E., Wang, D., & Zhai, M. (2021c). A cluster-based intelligence ensemble learning method for classification problems. Information Sciences, 560, 386–409.

Cui, S., Yin, Y., Wang, D., Li, Z., & Wang, Y. (2021d). A stacking-based ensemble learning method for earthquake casualty prediction. Applied Soft Computing, 101, 107038.

D’Ecclesia, R. L., & Clementi, D. (2021). Volatility in the stock market: ANN versus parametric models. Annals of Operations Research, 299(1–2), 1101–1127.

Fan, X., Li, S., & Tian, L. (2015). Chaotic characteristic identification for carbon price and an multi-layer perceptron network prediction model. Expert Systems with Applications, 42(8), 3945–3952.

Ghoddusi, H., Creamer, G. G., & Rafizadeh, N. (2019). Machine learning in energy economics and finance: A review. Energy Economics, 81, 709–727.

Hao, Y., & Tian, C. (2020). A hybrid framework for carbon trading price forecasting: The role of multiple influence factor. Journal of Cleaner Production, 262, 120378.

He, F., Zhou, J., Feng, Z., & kai, Liu, G., & Yang, Y. (2019). A hybrid short-term load forecasting model based on variational mode decomposition and long short-term memory networks considering relevant factors with Bayesian optimization algorithm. Applied Energy, 237, 103–116.

Hou, Y., Wu, N. Q., Zhou, M. C., & Li, Z. W. (2017). Pareto-optimization for scheduling of crude oil operations in refinery via genetic algorithm. IEEE Transactions on Systems, Man, and Cybernetics: Systems, 47(3), 517–530.

Huang, Y., & He, Z. (2020). Carbon price forecasting with optimization prediction method based on unstructured combination. Science of the Total Environment, 725, 138350.

Jiang, M., Jia, L., Chen, Z., & Chen, W. (2020). The two-stage machine learning ensemble models for stock price prediction by combining mode decomposition, extreme learning machine and improved harmony search algorithm. Annals of Operations Research. https://doi.org/10.1007/s10479-020-03690-w

Kılıç, D. K., & Uğur, Ö. (2018). Multiresolution analysis of S&P500 time series. Annals of Operations Research, 260(1–2), 197–216.

Li, Z., Chen, J., Zi, Y., & Pan, J. (2017). Independence-oriented VMD to identify fault feature for wheel set bearing fault diagnosis of high speed locomotive. Mechanical Systems and Signal Processing, 85, 512–529.

Liang, D., Tsai, C. F., Dai, A. J., & Eberle, W. (2018). A novel classifier ensemble approach for financial distress prediction. Knowledge and Information Systems, 54(2), 437–462.

Lu, H., Ma, X., Huang, K., & Azimi, M. (2020). Carbon trading volume and price forecasting in China using multiple machine learning models. Journal of Cleaner Production, 249, 119386.

Malhotra, R., & Khanna, M. (2018). Particle swarm optimization-based ensemble learning for software change prediction. Information and Software Technology, 102, 65–84.

Mohammadi, H., & Su, L. (2010). International evidence on crude oil price dynamics: Applications of ARIMA-GARCH models. Energy Economics, 32(5), 1001–1008.

Mselmi, N., Lahiani, A., & Hamza, T. (2017). Financial distress prediction: The case of French small and medium-sized firms. International Review of Financial Analysis, 50, 67–80.

Nobre, J., & Neves, R. F. (2019). Combining principal component analysis, discrete wavelet transform and XGBoost to trade in the financial markets. Expert Systems with Applications, 125, 181–194.

Papouskova, M., & Hajek, P. (2019). Two-stage consumer credit risk modelling using heterogeneous ensemble learning. Decision Support Systems, 118, 33–45.

Parmezan, A. R. S., Souza, V. M. A., & Batista, G. E. A. P. A. (2019). Evaluation of statistical and machine learning models for time series prediction: Identifying the state-of-the-art and the best conditions for the use of each model. Information Sciences, 484, 302–337.

Perdan, S., & Azapagic, A. (2011). Carbon trading: Current schemes and future developments. Energy Policy, 39(10), 6040–6054.

Shajalal, M., Petr, H., & Abedin, M. Z. (2021). Product backorder prediction with deep neural network on imbalance data. International Journal of Production Research. https://doi.org/10.1080/00207543.2021.1901153

Sun, G., Chen, T., Wei, Z., Sun, Y., Zang, H., & Chen, S. (2016). A carbon price forecasting model based on variational mode decomposition and spiking neural networks. Energies, 9(1).

Sun, W., & Xu, C. (2021). Carbon price prediction based on modified wavelet least square support vector machine. Science of the Total Environment, 754, 142052.

Wang, N., Zhao, S., Cui, S., & Fan, W. (2021). A hybrid ensemble learning method for the identification of gang-related arson cases. Knowledge-Based Systems, 218, 106875.

Wei, S., Chongchong, Z., & Cuiping, S. (2018). Carbon pricing prediction based on wavelet transform and K-ELM optimized by bat optimization algorithm in China ETS: The case of Shanghai and Hubei carbon markets. Carbon Management, 9(6), 605–617.

Yang, W. A., Zhou, Q., & Tsui, K. L. (2016). Differential evolution-based feature selection and parameter optimisation for extreme learning machine in tool wear estimation. International Journal of Production Research, 54(15), 4703–4721.

Yao, L., Fang, Z., Xiao, Y., Hou, J., & Fu, Z. (2021). An intelligent fault diagnosis method for lithium battery systems based on grid search support vector machine. Energy, 214, 118866.

Yilmazer, S., & Kocaman, S. (2020). A mass appraisal assessment study using machine learning based on multiple regression and random forest. Land Use Policy, 99, 104889.

Zhu, B., Wang, P., Chevallier, J., & Wei, Y. (2015). Carbon price analysis using empirical mode decomposition. Computational Economics, 45(2), 195–206.

Zhu, B., & Wei, Y. (2013). Carbon price forecasting with a novel hybrid ARIMA and least squares support vector machines methodology. Omega, 41(3), 517–524.

Zhu, B., Ye, S., Wang, P., He, K., Zhang, T., & Wei, Y. M. (2018). A novel multiscale nonlinear ensemble leaning paradigm for carbon price forecasting. Energy Economics, 70, 143–157.

Zhu, J., Wu, P., Chen, H., Liu, J., & Zhou, L. (2019). Carbon price forecasting with variational mode decomposition and optimal combined model. Physica a: Statistical Mechanics and Its Applications, 519, 140–158.

Acknowledgements

This paper was supported in part by the National Natural Science Foundation of China under Grant Numbers 72171161, 71971041, 71871148, and 71533001; by the China Scholarship Council under Grant Number 202006060162, by the Outstanding Young Scientific and Technological Talents Foundation of Sichuan Province under Grant number 2020JDJQ0035; and by the Major Program of National Social Science Foundation of China under Grant 20&ZD084; and by Sichuan University to Building a World-class University under Grant No. SKSYL2021-08.

Author information

Authors and Affiliations

Corresponding author

Additional information

Publisher's Note

Springer Nature remains neutral with regard to jurisdictional claims in published maps and institutional affiliations.

Rights and permissions

About this article

Cite this article

Cui, S., Wang, D., Yin, Y. et al. Carbon trading price prediction based on a two-stage heterogeneous ensemble method. Ann Oper Res 345, 953–977 (2025). https://doi.org/10.1007/s10479-022-04821-1

Accepted:

Published:

Issue Date:

DOI: https://doi.org/10.1007/s10479-022-04821-1