Abstract

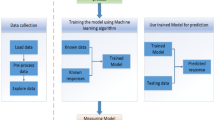

Due to the huge losses caused by the default of credit customers, the major loan platforms attach great importance to the testing and forecasting of non-performing loans. From the point of view of loan customer type identification and loan default, this paper constructs a WT early warning model of loan default client based on C5.0 decision tree, CART decision tree and CHAID decision tree in smart city. Aiming at the data characteristics of loan platform, this paper designs a posteriori combination mechanism of three algorithms and proposes a sub-model combined weighting algorithm based on the data characteristics of loan platform. Through the design performance test indicators, including sensitivity, accuracy, warning rate. The false alarm rate tests the performance of the combined and sub-model. In reality, using the real loan transaction dataset from the website of PPDAI to construct the WT model, it is found that the WT model overcomes the shortcomings of sub-model alone and achieves effective early warning of customer default. The empirical results show that the alarm rate of C5.0 is 29.17%, and the false alarm rate is 25.58%; the alarm rate of CART is 22.92%, and the false alarm rate is 20.59%; the alarm rate of CHAID is 23.75%, and the false alarm rate is 14.71%; the alarm rate of WT is 26.67%, and the false alarm rate is 17.65%; compared with other three algorithms, WT model is more effective in early warning of loan default.

Similar content being viewed by others

Explore related subjects

Discover the latest articles, news and stories from top researchers in related subjects.References

Adibi MA (2019) Single and multiple outputs decision tree classification using bi-level discrete-continues genetic algorithm. Pattern Recogn Lett 128:190–196

AghaeiRad A, Chen N, Ribeiro B (2017) Improve credit scoring using transfer of learned knowledge from self-organizing map. Neural Comput Appl 28:1329–1342

Ala’Raj M, Abbod MF (2016a) Classifiers consensus system approach for credit scoring. Knowl Based Syst 104:89–105

Ala’Raj M, Abbod MF (2016b) A new hybrid ensemble credit scoring model based on classifiers consensus system approach. Expert Syst Appl 64:36–55

Croux C, Jagtiani J, Korivi T, Vulanovic M (2020) Important factors determining Fintech loan default: evidence from a lendingclub consumer platform. J Econ Behav Org 173:270–296

Gadomer L, Sonowski ZA (2019) Knowledge aggregation in decision-making process with C-fuzzy random forest using OWA operators. Soft Comput 23:3741–3755

Hall M, Frank E, Holmes G, Pfahringer B, Reutemann P, Witten IH (2009) The WEKA data mining software: an update. SIGKDD Explor Newsl 11:10–18

Imtiaz S, Brimicombe AJ (2017) A better comparison summary of credit scoring classification. Int J Adv Comput Sci Appl. https://doi.org/10.14569/IJACSA.2017.080701

Kultur Y, Caglayan MU (2016) Hybrid approaches for detecting credit card fraud. Expert Syst. https://doi.org/10.1111/exsy.12191

Li X, Zhong Y (2012) An overview of personal credit scoring: techniques and future work. Int J Intell Sci. https://doi.org/10.4236/ijis.2012.2240242181-189

Ooi S, Tan S, Cheah W (2018) Temporal sleuth machine with decision tree for temporal classification. Soft Comput 22:8077–8095

Pang S, Gong J (2009) C5.0 classification algorithm and its application on individual credit score for banks. Syst Eng-Theory Pract 29:94–104

Pang S, Yuan J (2018) WT model and applications in loan platform customer default prediction based on decision tree algorithms. Intell Comput Theor Appl 6:1–13

Sivakumar S, Selvaraj R (2018) Predictive modeling of students performance through the enhanced decision tree. Adv Electron Commun Comput 10:21–36

Song Y, Wang Y, Ye X, Wang D, Yin Y, Wang Y (2020) Multi-view ensemble learning based on distance-to-model and adaptive clustering for imbalanced credit risk assessment in P2P lending. Inf Sci 525:182–204

Sun X (2019) Research on time series data mining algorithm based on Bayesian node incremental decision tree. Clust Comput 22:10361–10370

Tanoue Y, Kawada A, Yamashita S (2017) Forecasting loss given default of bank loans with multi-stage model. Int J Forecast 33:513–522

Xia Y, Liu C, Liu N (2017) Cost-sensitive boosted tree for loan evaluation in peer-to-peer lending. Electron Commer Res Appl 24:30–49

Xia Y, Liu C, Da B, Xie F (2018) A novel heterogeneous ensemble credit scoring model based on bstacking approach. Expert Syst Appl 93:182–199

Yuri Z, Fedorova E, Chekrizov D (2016) Two-step classification method based on geneticalgorithm for bankruptcy forecasting. Expert Syst Appl 88:393–401

Zhou L, Hamido F (2017) Posterior probability based ensemble strategy using optimizing decision directed acyclic graph for multi-class classification. Inf Sci 400–401:142–156

Acknowledgements

The paper is supported by the National Natural Science Foundation of China (91646112, 71771105).

Author information

Authors and Affiliations

Corresponding authors

Ethics declarations

Conflict of Interest

This paper is an original research and has not been submitted to any other journals. So there is no any conflict of interest in any other journals.

Additional information

Publisher's Note

Springer Nature remains neutral with regard to jurisdictional claims in published maps and institutional affiliations.

Rights and permissions

About this article

Cite this article

Pang, S., Wei, M., Yuan, J. et al. WT combined early warning model and applications for loaning platform customers default prediction in smart city. J Ambient Intell Human Comput 14, 1419–1430 (2023). https://doi.org/10.1007/s12652-021-03166-0

Received:

Accepted:

Published:

Issue Date:

DOI: https://doi.org/10.1007/s12652-021-03166-0