Abstract

This paper discusses a multi-objective mean-variance model and its solution algorithms for the project selection considering synergy under the uncertain environment. Two objective functions have been considered: maximizing the expected net present value (NPV) of the selected projects and minimizing the risk measured by variance of NPV. Here, the profits and investment outlays for candidate projects and synergistic profits and outlays of interdependent projects are considered as uncertain variables whose distributions are determined by experts’ evaluations. According to uncertainty theory, the deterministic equivalents are obtained. The effect of uncertainty on project selection is analyzed through comparison between the proposed uncertain model and the certain model with exact parameters. And the effect of synergy on the project selection is also analyzed. To get the Pareto-optimal solutions of the proposed multi-objective project selection model, we provide a new multi-objective modified binary Jaya (MOMB-Jaya) algorithm and a new multi-objective modified binary Rao (MOMB-Rao) algorithm, which respectively are modifications of the Jaya and Rao algorithms for solving the proposed multi-objective problems. Through numerical experiments on 15 example problems, including large-scale problems, the performances of the proposed multi-objective binary algorithms are tested. Comparison with the binary version of non-dominated teaching-learning-based optimization (NSTLBO) algorithm shows the better performance of the MOMB-Rao algorithm. Finally, a numerical example is given to demonstrate the validity of the proposed multi-objective uncertain model.

Similar content being viewed by others

References

Weingartner HM (1963) Mathematical programming and the analysis of capital budgeting problems. Englewood Press, New Jersey

Farshchian MM, Heravi G (2018) Probabilistic assessment of cost, time, and revenue in a portfolio of projects using stochastic agent-based simulation. J Constr Eng Manag 144(5):04018028. https://doi.org/10.1061/(ASCE)CO.1943-7862.0001476

Panadero J, Doering J, Kizys R, Juan AA, Fito A (2020) A variable neighborhood search simheuristic for project portfolio selection under uncertainty. J Heurist 26(3):353–375. https://doi.org/10.1007/s10732-018-9367-z

Zhang X, Gong B, Yang F, Ang S (2019) A stochastic multicriteria acceptability analysis-evidential reasoning method for uncertain multi-attribute decision-making problems. Expert Syst 36(4):e12426. https://doi.org/10.1111/exsy.12426

Wu Y, Xu C, Ke Y, Chen K, Sun X (2018) An intuitionistic fuzzy multi-criteria framework for large-scale rooftop PV project portfolio selection: Case study in Zhejiang, China. Energy 143:295–309. https://doi.org/10.1016/j.energy.2017.10.105

Mohagheghi V, Mousavi SM, Antuchevičienė J, Mojtahedi M (2019) Project portfolio selection problems: a review of models, uncertainty approaches, solution techniques, and case studies. Technol Econ Dev Econ 25(6):1380–1412. https://doi.org/10.3846/tede.2019.11410

Zhang Q, Huang X, Tang L (2011) Optimal multinational capital budgeting under uncertainty. Comput Math Appl 62(12):4557–4567. https://doi.org/10.1016/j.camwa.2011.10.035

Zhang Q, Huang X, Zhang C (2015) A mean-risk index model for uncertain capital budgeting. J Oper Res Soc 66(5):761–770. https://doi.org/10.1057/jors.2014.51

Liu B (2007) Uncertainty theory. Springer, Berlin, pp 205–234

Zhang B, Peng J, Li S (2017) Covering location problem of emergency service facilities in an uncertain environment. Appl Math Model 51:429–447. https://doi.org/10.1016/j.apm.2017.06.043

Rahdar M, Wang L, Hu G (2018) A tri-level optimization model for inventory control with uncertain demand and lead time. Int J Prod Econ 195:96–105. https://doi.org/10.1016/j.ijpe.2017.10.011

Wang X, Ning Y (2018) Uncertain chance-constrained programming model for project scheduling problem. J Oper Res Soc 69(3):384–391. https://doi.org/10.1057/s41274-016-0122-2

Lu Z, Zhu Y (2019) Numerical approach for solution to an uncertain fractional differential equation. Appl Math Comput 343:137–148. https://doi.org/10.1016/j.amc.2018.09.044

Yang X, Jing F, Ma N, Nie F (2020) Supply chain pricing and effort decisions with the participants’ belief under the uncertain demand. Soft Comput 24(9):6483–6497. https://doi.org/10.1007/s00500-019-04633-9

Huang X, Zhao T (2016) Project selection and adjustment based on uncertain measure. Inf Sci 352–353:1–14. https://doi.org/10.1016/j.ins.2016.02.050

Huang X, Zhao T, Kudratova S (2016) Uncertain mean-variance and mean-semivariance models for optimal project selection and scheduling. Knowl-Based Syst 93:1–11. https://doi.org/10.1016/j.knosys.2015.10.030

Li X, Zhong Z, Zhang Y, Wang Y (2017) Uncertain mean-variance model for project portfolio selection problem with divisibility. J Intell Fuzzy Syst 32(6):4513–4522. https://doi.org/10.3233/JIFS-169215

Yan S, Ji X (2018) Portfolio selection model of oil projects under uncertain environment. Soft Comput 22(17):5725–5734. https://doi.org/10.1007/s00500-017-2619-2

Abbassi D, Ashrafi M, Ghodsypour SH (2020) A multi objective-BSC model for new product development project portfolio selection. Expert Syst Appl 162:113757. https://doi.org/10.1016/j.eswa.2020.113757

Nemati-Lafmejani R, Davari-Ardakani H, Najafzad H (2019) Multi-mode resource constrained project scheduling and contractor selection: mathematical formulation and metaheuristic algorithms. Appl Soft Comput 81:105533. https://doi.org/10.1016/j.asoc.2019.105533

Gupta N, Sharma A, Pachariya MK (2020) Testing and debugging: an empirical evaluation of integrated approaches. Sādhanā 45(1):148. https://doi.org/10.1007/s12046-020-01382-6

Deng Y, Xu H, Wu J (2021) Optimization of blockchain investment portfolio under artificial bee colony algorithm. J Comput Appl Math 385:113199. https://doi.org/10.1016/j.cam.2020.113199

Chen R, Liang C, Gu D, Zhao H (2020) A competence-time-quality scheduling model of multi-skilled staff for IT project portfolio. Comp Ind Eng 139:106183. https://doi.org/10.1016/j.cie.2019.106183

Rao RV, Savsani VJ, Vakharia DP (2011) Teaching-learning-based optimization: a novel method for constrained mechanical design optimization problems. Comput Aided Des 43(3):303–315. https://doi.org/10.1016/j.cad.2010.12.015

Rao RV (2016) Jaya: A simple and new optimization algorithm for solving constrained and unconstrained optimization problems. Int J Ind Eng Comput 7:19–34. https://doi.org/10.5267/j.ijiec.2015.8.004

Rao RV (2020) Rao algorithms: three metaphor-less simple algorithms for solving optimization problems. Int J Ind Eng Comput 11:107–130. https://doi.org/10.5267/j.ijiec.2019.6.002

Rao RV, Rai DP, Balic J (2018) Multi-objective optimization of machining and micro-machining processes using non-dominated sorting teaching-learning-based optimization algorithm. J Intell Manuf 29(8):1715–1737. https://doi.org/10.1007/s10845-016-1210-5

Rao RV, Rai DP, Balic J (2017) A multi-objective algorithm for optimization of modern machining processes. Eng Appl Artif Intell 61:103–125. https://doi.org/10.1016/j.engappai.2017.03.001

Rao RV, Keesari HS (2020) Rao algorithms for multi-objective optimization of selected thermodynamic cycles. Eng Comp. https://doi.org/10.1007/s00366-020-01008-9

Kern Z, Lu Y, Vasko FJ (2020) An OR practitioner’s solution approach to the multidimensional knapsack problem. Int J Ind Eng Comput 11:73–82. https://doi.org/10.5267/j.ijiec.2019.6.004

Awadallah MA, Al-Betar MA, Hammouri AI, Alomari OA (2020) Binary JAYA algorithm with adaptive mutation for feature selection. Arab J Sci Eng 45(12):10875–10890. https://doi.org/10.1007/s13369-020-04871-2

Sharma SR, Singh B, Kaur M (2021) Classification of Parkinson disease using binary Rao optimization algorithms. Expert Syst 38:e12674. https://doi.org/10.1111/exsy.12674

Kumar M, Mittal M, Soni G, Joshi D (2018) A hybrid TLBO-TS algorithm for integrated selection and scheduling of projects. Comp Ind Eng 119:121–130. https://doi.org/10.1016/j.cie.2018.03.029

Lu Y, Vasko FJ (2015) An OR practitioner’s solution approach for the set covering problem. Int J Appl Metaheur Comput 6(4):1–13. https://doi.org/10.4018/IJAMC.2015100101

Deb K, Pratap A, Agarwal S (2002) A fast and elitist multiobjective genetic algorithm: NSGA-II. IEEE Trans Evol Comput 6(2):182–197. https://doi.org/10.1109/4235.996017

Author information

Authors and Affiliations

Corresponding author

Additional information

Publisher's Note

Springer Nature remains neutral with regard to jurisdictional claims in published maps and institutional affiliations.

A Uncertainty Theory

A Uncertainty Theory

To help understand uncertain portfolio selection, we provide the fundamentals of uncertainty theory used in out paper. For more knowledge, the readers can refer to [9].

The uncertain variable in uncertainty theory is characterized by an uncertainty distribution defined as below.

Definition 1

[9] For any real number t, the function \(\Phi (t)\) defined by

is called the uncertainty distribution of the uncertain variable \(\xi\).

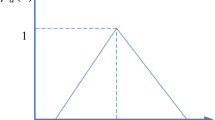

For a linear uncertain variable \(\xi\), its uncertainty distribution is expressed as

For convenience, the linear uncertainty distribution is denoted by \(\xi \thicksim {{\mathcal {L}}}(a,b)\) where \(a<b\).

For a normal uncertain variable \(\xi\), its uncertainty distribution is expressed as

For convenience, it is denoted by \(\xi \thicksim {{\mathcal {N}}}(\mu ,\sigma )\) where \(\mu\) and \(\sigma\) are real numbers and \(\sigma >0\).

[9].

Theorem 7

[9] Let uncertain variables \(\xi _1, \xi _2, \ldots , \xi _n\) be independent and their uncertainty distributions \(\Phi _1, \Phi _2, \ldots , \Phi _n\) be regular. If \(f(\xi _1, \xi _2, \ldots , \xi _n)\) increases monotonically with respect to \(\xi _1, \xi _2, \ldots , \xi _m\) and decreases monotonically with respect to \(\xi _{m+1}, \xi _{m+2}, \ldots , \xi _n\), then the inverse uncertainty distribution of

is expressed as

Definition 2

[9] The quantity \(E[\xi ]\) defined by

is called the expected value of the uncertain variable \(\xi\) if at least one of the two integrals is finite.

Theorem 8

Let \(\xi\) be an uncertain variable and \(\Phi\) be a regular uncertainty distribution of \(\xi\). If there exists the expected value of \(\xi\), then

Definition 3

[9] Let \(\xi\) be an uncertain variable and \(\mu\) be a finite expected value of \(\xi\). Then the quantity \(V[\xi ]\) defined by

is called the variance of the uncertain variable \(\xi\), and the square root of the variance is called the standard deviation of \(\xi\).

Theorem 9

[9] Let \(\xi\) be an uncertain variable, \(\Phi\) be a regular uncertainty distribution of \(\xi\) and \(\mu\) be a finite expected value of \(\xi\). Then

Rights and permissions

About this article

Cite this article

Huang, X., Hong, K.R., Kim, J.S. et al. Multi-objective uncertain project selection considering synergy. Int. J. Mach. Learn. & Cyber. 13, 2383–2402 (2022). https://doi.org/10.1007/s13042-022-01532-8

Received:

Accepted:

Published:

Issue Date:

DOI: https://doi.org/10.1007/s13042-022-01532-8