Abstract

The measurement of financial risk relies on two factors: determination of riskiness by use of an appropriate risk measure; and the distribution according to which returns are governed. Wrong estimates of either, severely compromise the accuracy of computed risk. We identify the too-big-to-fail banks with the set of “Global Systemically Important Banks” (G-SIBs) and analyze the equity risk of its equally weighted portfolio by means of the “Foster–Hart risk measure”—a bankruptcy-proof, reserve based measure of risk, extremely sensitive to tail events. We model banks’ stock returns as an ARMA–GARCH process with multivariate “Normal Tempered Stable” innovations, to capture the skewed and leptokurtotic nature of stock returns. Our union of the Foster–Hart risk modeling with fat-tailed statistical modeling bears fruit, as we are able to measure the equity risk posed by the G-SIBs more accurately than is possible with current techniques.

Similar content being viewed by others

Notes

In Basel II, capital requirements for banks were uniform and not dependent on their systemic importance.

The list of G-SIBs included in our study, as it stood in November 2013 can be found in Table 6. For the latest list of G-SIBs, please visit http://www.financialstabilityboard.org/wp-content/uploads/2015-update-of-list-of-global-systemically-important-banks-G-SIBs.

The FSA was dissolved from April 1st, 2013 and its duties were split between the Prudential Regulation Authority, the Financial Conduct Authority and the Bank of England.

As may be easily observed, a trivial solution for bankruptcy-proofing future sequences of investments is to not undertake any such investment! Or equivalently, by imposing the minimal wealth required to undertake an investment to be infinite, one can trivially ensure non-bankruptcy—no matter what the future sequence of payoff distributions might be. However, what is remarkable about Foster and Hart (2009) is their result that agents could have a finite level of wealth, as computed by the Foster–Hart risk and still be almost surely bankruptcy-proof in the face of arbitrary sequences of bounded gambles.

Since the G-SIB portfolio is emblematic of the equity risk that the too-big-to-fail banks pose on the representative investor, we choose to weigh all constituent banks equally. While this is not the only set of weights consistent with such an objective, (other candidates include weights being proportional to the market capitalizations of individual banks; or to their assets under management, among others) it is the simplest one. Moreover for the purposes of comparison between estimates of different risk measures, the results remain qualitatively similar and do not depend too much on the details of the weight distribution between constituent banks.

The second right hand side follows if we assume that G is continuous.

Consistent with asymptotic power law decay of stock returns, the Foster–Hart risk incorporates rare events’ potential for causing extreme losses.

We note that while tempering the Stable distribution results in finite variance, thereby implying convergence to the Normal distribution via the Central Limit Theorem, the speed of convergence is slow; and the distribution of the summands remains close to that of the corresponding Stable distribution. This is an instance of a pre-limit theorem more details on which, and applications thereof, may be found in Rachev and Mittnik (2000).

We note that the linear combination of standard NTS random variables with common \(\alpha \) and \(\theta \) parameters is again an NTS random variable (Kim et al. 2012)—a fact that we use in portfolio analysis with NTS innovations in later sections.

The list of Global Systemically Important Banks as it stood in November 2013, is presented as Table 6 in the “Appendices”.

The latest list of G-SIBs (November 2015) includes two new banks: the Agricultural Bank of China and the China Construction Bank, while BBVA has been removed. For our study however, the list of G-SIBs excludes these developments and considers the list as it stood in November 2013 (see Table 6).

We broadly follow the approach of Kim et al. (2011), which studied ARMA–GARCH processes with Tempered Stable innovations.

There are about 250 trading days in a typical year. Hence our choice of a 250-day window corresponds to the most recent 1 year of return data for computing the covariance matrix.

1250 daily returns correspond to about 5 years of financial data, since each year has about 250 daily returns. This width of the rolling window is standard in literature.

For the case with NTS distributed assets, Kim et al. (2012) show that the portfolio—a linear combination of individual asset distributions—remains NTS distributed.

This test is also called the “proportion of failures” test in Kupiec (1995).

See http://www.financialstabilityboard.org/publications/r_131111 for more details.

References

Admati, A., & Hellwig, M. (2013). The Bankers’ new clothes: What’s wrong with banking and what to do about it. Princeton, NJ: Princeton University Press.

Alexander, S. S. (1961). Price movements in speculative markets: Trends or random walks. Industrial Management Review, 2, 7–25.

Anand, A., Li, T., Kurosaki, T., & Kim, Y. S. (2016). Foster-Hart optimal portfolios. Journal of Banking and Finance, 68, 117–130.

Artzner, P., Delbaen, F., Eber, J.-M., & Heath, D. (1998). Coherent measures of risk. Mathematical Finance, 6(3), 203–228.

Barndorff-Nielsen, O. E., & Shephard, N. (2001). Normal modified stable processes. Economics Series Working Papers from University of Oxford, Department of Economics 72.

Barndorff-Nielsen, O. E., & Levendorskii, S. Z. (2001). Feller processes of normal inverse gaussian type. Quantitative Finance, 1(3), 318–331.

Berkowitz, J. (2001). Testing density forecasts, with applications to risk management. Journal of Business and Economic Statistics, 19, 465–474.

Bollerslev, T. (1986). Generalized autoregressive conditional heteroskedasticity. Journal of Econometrics, 31, 307–327.

Christoffersen, P. F. (1998). Evaluating interval forecasts. International Economic Review, 39(4), 841–862.

Engle, R. (1982). Autoregressive conditional heteroscedasticity with estimates of the variance of united kingdom inflation. Econometrica, 4, 987–1008.

Fama, E. F. (1963). Mandelbrot and the stable Paretian hypothesis. Journal of Business, 36, 420–429.

Fama, E. F. (1965). The behavior of stock market prices. Journal of Business, 38, 34–105.

FinAnalytica Inc. (2014). Cognity 4.0. http://optimizer.cognity.net/.

Foster, D. P., & Hart, S. (2009). An operational measure of riskiness. Journal of Political Economy, 117(5), 785–814.

Haas, M., & Pigorsch, C. (2009). Financial economics, fat-tailed distributions. In R. A. Meyers (Ed.), Complex systems in finance and econometrics (pp. 308–339). New York: Springer.

Hodrick, R., & Prescott, E. C. (1997). Postwar U.S. business cycles: An empirical investigation. Journal of Money, Credit and Banking, 29(1), 1–16.

Kim, Y. S., Giacometti, R., Rachev, S. T., Fabozzi, F. J., & Mignacca, D. (2012). Measuring financial risk and portfolio optimization with a non-Gaussian multivariate model. Annals of Operations Research, 201(1), 325–343.

Kim, Y. S., Rachev, S. T., Bianchi, M. L., & Fabozzi, F. J. (2008). Financial market models with Levy processes and time-varying volatility. Journal of Banking and Finance, 32(7), 1363–1378.

Kim, Y. S., Rachev, S. T., Bianchi, M. L., & Fabozzi, F. J. (2010). Tempered stable and tempered infinitely divisible GARCH models. Journal of Banking and Finance, 34, 2096–2109.

Kim, Y. S., Rachev, S. T., Bianchi, M. L., Mitov, I., & Fabozzi, F. J. (2011). Time series analysis for financial market meltdowns. Journal of Banking and Finance, 35, 1879–1891.

Kupiec, P. H. (1995). Techniques for verifying the accuracy of risk measurement models. Journal of Derivatives, 6, 6–24.

Kurosaki, T., & Kim, Y. S. (2013). Sytematic risk measurement in the global banking stock market with time series analysis and CoVaR. Investment Management and Financial Innovations, 10(1), 184–196.

Mandelbrot, B. (1963a). New methods in statistical economics. Journal of Political Economy, 71, 421–440.

Mandelbrot, B. (1963b). The variation of certain speculative prices. Journal of Business, 36, 394–419.

Mandelbrot, B. (1967). The variation of some other speculative prices. Journal of Business, 40, 393–413.

Rachev, S. T., Schwartz, E., & Khindanova, I. (2003). Stable modeling of credit risk. In S. T. Rachev (Ed.), Handbook of heavy tailed distributions in finance. Amsterdam: North Holland.

Rachev, S. T., Stoyanov, S., Biglova, A., & Fabozzi, F. (2005). An empirical examination of daily stock return distributions for US stocks. In D. Baier, R. Decker & L. Schmidt-Thieme (Eds.), Data analysis and decision support. Berlin: Springer.

Rachev, S. T., & Mittnik, S. (2000). Stable Paretian models in finance. Hoboken, NJ: Wiley.

Riedel, F., & Hellmann, T. (2015). The Foster–Hart measure of riskiness for general gambles. Theoretical Economics, 10, 1–9.

Acknowledgments

The opinions, findings, conclusions or recommendations expressed in this paper are our own and do not necessarily reflect the views of the Bank of Japan. Abhinav Anand gratefully acknowledges financial support by the Science Foundation Ireland Under Grant Number 08/SRC/FMC1389. Tiantian Li thanks financial support by the National Natural Science Foundation of China Under Grant Number 71471119. We would like to express our gratitude to Svetlozar Rachev for methodological guidance and constant encouragement without which this research would have been impossible. We also thank Sandro Brusco, Yair Tauman and Hugo Benitez-Silva; and to Xin Tang for their critical commentary on an earlier version of this work. Special thanks are in order to Bruno Badia, for suggestions for improvements on a previous draft of this working paper. All remaining flaws of course, are entirely our own.

Author information

Authors and Affiliations

Corresponding author

Appendices

Appendices

The “Appendices” include tables indicating the membership of G-SIBs, as assessed by the Financial Stability Board. Also contained are graphical results that chart variation in computed risk with changes in the underlying statistical model.

1.1 Appendix 1: The global systemically important banks

The list of Systemically Important Banks is included in Table 6. This table was prepared in November 2013 by the Financial Stability Board.Footnote 20 It features 8 banks from North America, 16 banks from Europe and 5 banks from Asia.

1.2 Appendix 2: Variation of FH risk with the underlying statistical model

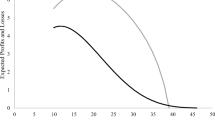

As should be expected, due to the fat-tailed distributional hypothesis of the AGNTS model, the FH equity risk under AGNTS is higher than that computed under the AGT and the AGNormal model. While there are qualitative similarities, for almost all time periods, the FH risk under AGNTS dominates that under the others, as can be seen in Fig. 5. (We note however, that this behavior is reversed for the third and fourth quarter of 2012 during which FH risk under AGNormal dominates the others).

We use the unique, continuity property of the Foster–Hart risk to rule out the existence of outliers. We note that this technique is justified since the time series of maximum losses of the portfolio is (approximately) continuous.

Variation of FH Risk with AGNTS, AGT and AGNormal models. All series have been smoothed by using the Hodrick–Prescott filter with \(\lambda =20{,}000\)

Rights and permissions

About this article

Cite this article

Anand, A., Li, T., Kurosaki, T. et al. The equity risk posed by the too-big-to-fail banks: a Foster–Hart estimation. Ann Oper Res 253, 21–41 (2017). https://doi.org/10.1007/s10479-016-2309-y

Published:

Issue Date:

DOI: https://doi.org/10.1007/s10479-016-2309-y