Abstract

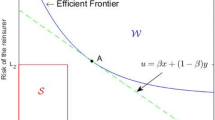

The notion of Pareto optimality is commonly employed to formulate decisions that reconcile the conflicting interests of multiple agents with possibly different risk preferences. In the context of a one-period reinsurance market comprising an insurer and a reinsurer, both of which perceive risk via distortion risk measures, also known as dual utilities, this article characterizes the set of Pareto-optimal reinsurance policies analytically and visualizes the insurer–reinsurer trade-off structure geometrically. The search of these policies is tackled by translating it mathematically into a functional minimization problem involving a weighted average of the insurer’s risk and the reinsurer’s risk. The resulting solutions not only cast light on the structure of the Pareto-optimal contracts, but also allow us to portray the resulting insurer–reinsurer Pareto frontier graphically. In addition to providing a pictorial manifestation of the compromise reached between the insurer and reinsurer, an enormous merit of developing the Pareto frontier is the considerable ease with which Pareto-optimal reinsurance policies can be constructed even in the presence of the insurer’s and reinsurer’s individual risk constraints. A strikingly simple graphical search of these constrained policies is performed in the special cases of Value-at-Risk and Tail Value-at-Risk.

Similar content being viewed by others

Notes

This condition, which is stronger than the usual \(g(0)=0\), is a necessary condition for the finiteness of the DRM of unbounded random variables, which are of particular relevance to reinsurance.

To ensure that the Lebesgue–Stieltjes integral with respect to \(g(S_{Y}(\cdot ))\) is well-defined, the left- or right-continuity of g is required. See the proof of Lemma 2.1 of Cheung and Lo (2017) about how general distortion functions (not necessarily left-continuous or right-continuous) can be dealt with.

TVaR is also known variously as Average Value-at-Risk (AVaR), Conditional Value-at-Risk (CVaR), and Expected Shortfall (ES), although there are subtle differences between these terms.

Note that \([F_{X}^{-1}(\beta ),F_{X}^{-1}(\alpha ))\) is the empty set when \(\alpha \le \beta \).

References

Aliprantis, C. D., & Border, K. C. (2006). Infinite dimensional analysis (Third ed.). Berlin: Springer.

Aouni, B., Colapinto, C., & La Torre, D. (2014). Financial portfolio management through the goal programming model: Current state-of-the-art. European Journal of Operational Research, 234, 536–545.

Arrow, K. (1963). Uncertainty and the welfare economics of medical care. American Economic Review, 53, 941–973.

Asimit, A. V., Badescu, A. M., & Verdonck, T. (2013). Optimal risk transfer under quantile-based risk measurers. Insurance: Mathematics and Economics, 53, 252–265.

Assa, H. (2015). On optimal reinsurance policy with distortion risk measures and premiums. Insurance: Mathematics and Economics, 61, 70–75.

Borch, K. (1960). An attempt to determine the optimum amount of stop loss reinsurance. Transactions of the 16th International Congress of Actuaries, 1, 597–610.

Borch, K. (1969). The optimal reinsurance treaty. ASTIN Bulletin, 5, 293–297.

Cai, J., Fang, Y., Li, Z., & Willmot, G. E. (2013). Optimal reciprocal reinsurance treaties under the joint survival probability and the joint profitable probability. The Journal of Risk and Insurance, 80, 145–168.

Cai, J., Lemieux, C., & Liu, F. (2016). Optimal reinsurance from the perspectives of both an insurer and a reinsurer. ASTIN Bulletin, 46, 815–849.

Cai, J., Liu, H., & Wang, R. (2017). Pareto-optimal reinsurance arrangements under general model settings. Insurance: Mathematics and Economics, 77, 24–37.

Cai, J., & Tan, K. S. (2007). Optimal retention for a stop-loss reinsurance under the VaR and CTE risk measure. ASTIN Bulletin, 37, 93–112.

Cai, J., Tan, K. S., Weng, C., & Zhang, Y. (2008). Optimal reinsurance under VaR and CTE risk measures. Insurance: Mathematics and Economics, 43, 185–196.

Cheung, K. C., & Lo, A. (2017). Characterizations of optimal reinsurance treaties: A cost–benefit approach. Scandinavian Actuarial Journal, 2017, 1–28.

Chi, Y., & Tan, K. S. (2011). Optimal reinsurance under VaR and CVaR risk measures: A simplified approach. ASTIN Bulletin, 41, 487–509.

Cong, J., & Tan, K. S. (2016). Optimal VaR-based risk management with reinsurance. Annals of Operations Research, 237, 177–202.

Cui, W., Yang, J., & Wu, L. (2013). Optimal reinsurance minimizing the distortion risk measure under general reinsurance premium principles. Insurance: Mathematics and Economics, 53, 74–85.

Dhaene, J., Vanduffel, S., Goovaerts, M. J., Kaas, R., Tang, Q., & Vyncke, D. (2006). Risk measures and comonotonicity: A review. Stochastic Models, 22, 573–606.

Ehrgott, M. (2005). Multicriteria optimization (Second ed.). Berlin: Springer.

Gerber, H. U. (1979). An introduction to mathematical risk theory. Philadelphia: S. S. Huebner Foundation for Insurance Education, University of Pennsylvania.

Grechuk, B., & Zabarankin, M. (2012). Optimal risk sharing with general deviation measures. Annals of Operations Research, 200, 9–21.

Hürlimann, W. (2011). Optimal reinsurance revisited: Point of view of cedent and reinsurer. ASTIN Bulletin, 41, 547–574.

Jayaraman, R., Colapinto, C., La Torre, D., & Malik, T. (2015). Multi-criteria model for sustainable development using goal programming applied to the United Arab Emirates. Energy Policy, 87, 447–454.

Jiang, W., Ren, J., & Zitikis, R. (2017). Optimal reinsurance policies under the VaR risk measure when the interests of both the cedent and the reinsurer are taken into account. Risks, 5, 11.

La Torre, D. (2017). Preface: Multiple criteria optimization and goal programming in science, engineering, and social sciences. Annals of Operations Research, 251, 1–5.

Lo, A. (2016). How does reinsurance create value to an insurer? A cost–benefit analysis incorporating default risk. Risks, 4, 48.

Lo, A. (2017a). A Neyman–Pearson perspective on optimal reinsurance with constraints. ASTIN Bulletin, 47, 467–499.

Lo, A. (2017b). A unifying approach to risk-measure-based optimal reinsurance problems with practical constraints. Scandinavian Actuarial Journal, 2017(7), 584–605.

Ludkovski, M., & Young, V. R. (2009). Optimal risk sharing under distorted probabilities. Mathematics and Financial Economics, 2009, 87–105.

Maggis, M., & La Torre, D. (2012). A goal programming model with satisfaction function for risk management and optimal portfolio diversification. INFOR: Information Systems and Operational Research, 50, 117–126.

Wallenius, J., Dyer, J. S., Fishburn, P. C., Steuer, R. E., Zionts, S., & Deb, K. (2008). Multiple criteria decision making, multiattribute utility theory: Recent accomplishments and what lies ahead. Management Science, 54, 1336–1349.

Yaari, M. E. (1987). The dual theory of choice under risk. Econometrica, 55, 95–115.

Zarepisheh, M., & Pardalos, P. M. (2017). An equivalent transformation of multi-objective optimization problems. Annals of Operations Research, 249, 5–15.

Zhuang, S. C., Weng, C., Tan, K. S., & Assa, H. (2016). Marginal indemnification function formulation for optimal reinsurance. Insurance: Mathematics and Economics, 67, 65–76.

Zopounidis, C., & Pardalos, P. M. (Eds.). (2010). Handbook of multicriteria analysis. Berlin: Springer.

Acknowledgements

This work was supported by a start-up fund provided by the College of Liberal Arts and Sciences, The University of Iowa, and a Centers of Actuarial Excellence (CAE) Research Grant (2018-2021) from the Society of Actuaries (SOA). Any opinions, finding, and conclusions or recommendations expressed in this material are those of the authors and do not necessarily reflect the views of the SOA. The authors are also grateful to a Stanley International Travel Award from International Programs, The University of Iowa, and the anonymous reviewers for their careful reading and insightful comments.

Author information

Authors and Affiliations

Corresponding author

Rights and permissions

About this article

Cite this article

Lo, A., Tang, Z. Pareto-optimal reinsurance policies in the presence of individual risk constraints. Ann Oper Res 274, 395–423 (2019). https://doi.org/10.1007/s10479-018-2820-4

Published:

Issue Date:

DOI: https://doi.org/10.1007/s10479-018-2820-4