Abstract

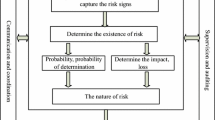

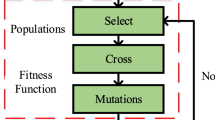

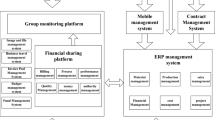

This paper presents an evaluation of the financial system risk quantitatively and a management information system designed to improve financial risk management. Based on the recognition of risk sources for all kinds of financial institutions and financial markets, we use a matrix covering financial risk probability and related damage to assess local risks and carry out risk classification, and use self-organizing mapping neural network model to evaluate the overall risks. Also, by means of radio frequency identification technology and big data analytics platform—Hadoop platform, a management information system is built which could perform three core functions: real-time monitor , analysis and evaluation, and automatic control, which would help regulators to realize the whole process and comprehensive intelligent management for financial risk sources.

Similar content being viewed by others

References

Chao, L., Lu, M.: Analytic hierarchy process and fuzzy assessment method in the application of the risk evaluation of electronic commerce. In: Conference: international conference on humanity and social science (ICHSS2016) (2016)

Li, C., Zhang, X., Geng, H., Yan, J.: Robustness analysis model for MADM methods based on cloud model. Procedia Comput. Sci. 107, 84–90 (2017)

Guo, Hui, Neely, Christopher J., Higbee, Jason: Foreign exchange volatility is priced in equities. Financial Manag. 37(4), 769–790 (2008)

Pavlova, Anna, Rigobon, Roberto: Asset prices and exchange rates. Rev. Financial Stud. 20(4), 1139–1181 (2007)

Chen, Nai-fu, Cuny, Charles J., Haugen, Robert A.: Stock volatility and the levels of the basis and open interest in futures contracts. J. Finance 50(1), 281–300 (1995)

Trolle, Anders B., Schwartz, Eduardo S.: Unspanned stochastic volatility and the pricing of commodity derivatives. Rev. Financial Stud. 22(11), 4423–4461 (2009)

Akinduko, A.A., Mirkes, E.M., Gorban, A.N.: SOM: Stochastic initialization versus principal components. Inf. Sci. 364–365, 213–221 (2016)

Acknowledgements

The authors acknowledge the National Social Science Foundation of China (Grant: 16FJL011) and China University of political Science and Law (Grant: 14ZFG79002).

Author information

Authors and Affiliations

Corresponding author

Rights and permissions

About this article

Cite this article

Li, Y. Design a management information system for financial risk control. Cluster Comput 22 (Suppl 4), 8783–8791 (2019). https://doi.org/10.1007/s10586-018-1969-6

Received:

Revised:

Accepted:

Published:

Issue Date:

DOI: https://doi.org/10.1007/s10586-018-1969-6