Abstract

A support vector machine (SVM) stable to data outliers is proposed in three closely related formulations, and relationships between those formulations are established. The SVM is based on the value-at-risk (VaR) measure, which discards a specified percentage of data viewed as outliers (extreme samples), and is referred to as \(\mathrm{VaR}\)-SVM. Computational experiments show that compared to the \(\nu \)-SVM, the VaR-SVM has a superior out-of-sample performance on datasets with outliers.

Similar content being viewed by others

Notes

A statistically robust SVM should not be confused with an SVM relying on methods of robust optimization (Ben-Tal et al. 2009): the former is unaffected if a certain percentage of the training data is changed, whereas the latter finds the separation hyperplane under the assumption that the training data are not clearly specified but rather are known to be from some set.

The approach can be readily extended to the case of arbitrary probabilities of outcomes: \(\mathrm{Pr}(\omega _i)=p_i, i=1,\dots ,l\).

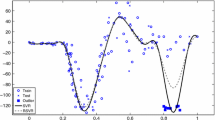

The dataset was taken from UCI Machine Learning Repository (http://archive.ics.uci.edu/ml/datasets.html).

References

Ben-Tal A, El Ghaoui L, Nemirovski A (2009) Robust optimization. Princeton University Press, Princeton

Boser B, Guyon I, Vapnik V (1992) A training algorithm for optimal margin classifiers. In: Proceedings of the fifth annual workshop on computational learning theory, ACM, pp 144–152

Byvatov E, Schneider G (2003) Support vector machine applications in bioinformatics. Appl Bioinformatics 2:67

Chapelle O (2007) Training a support vector machine in the primal. Neural Comput 19:1155–1178

Cortes C, Vapnik V (1995) Support-vector networks. Mach Learn 20:273–297

Crisp D, Burges C (2000) A geometric interpretation of v-SVM classifiers. Adv Neural Inf Process Syst 12(12):244

Cristianini N, Shawe-Taylor J (2000) An introduction to support vector machines and other kernel-based learning methods. Cambridge University Press, Cambridge

Duffie D, Pan J (1997) An overview of value at risk. J Deriv 4:7–49

Gaivoronski AA, Pflug G (2005) Value-at-risk in portfolio optimization: properties and computational approach. J Risk 7:1–31

Goto J, Takeda A (2005) Linear decision model based on conditional geometric score. In: Abstract collection of spring meeting for reading research paper by the Operations Research Society of Japan

Guo G, Li SZ, Chan K (2000) Face recognition by support vector machines. In: Proceedings of fourth IEEE international conference on automatic face and gesture recognition, pp 196–201

Huang C-L, Chen M-C, Wang C-J (2007) Credit scoring with a data mining approach based on support vector machines. Expert Syst Appl 33:847–856

Jorion P (1997) Value at risk: the new benchmark for controlling market risk, vol 2. McGraw-Hill, New York

Kazama J, Makino T, Ohta Y, Tsujii J (2002) Tuning support vector machines for biomedical named entity recognition. In: Proceedings of the ACL-02 workshop on natural language processing in the biomedical domain, vol 3. Association for Computational Linguistics, pp 1–8

Larsen N, Mausser H, Uryasev S (2002) Algorithms for optimization of value-at-risk. Appl Optim 70:19–46

Lin C, Wang S (2002) Fuzzy support vector machines. IEEE Trans Neural Netw 13:464–471

Pérez-Cruz F, Weston J, Herrmann D, Scholkopf B (2003) Extension of the nu-SVM range for classification. NATO Sci Ser III Comput Syst Sci 190:179–196

Rockafellar RT, Uryasev S (2000) Optimization of conditional value-at-risk. J Risk 2:21–42

Sakalauskas L, Tomasgard A, Wallace S (2012) Advanced risk measures in estimation and classification. Proceedings, Vilnius, pp 114–118

Schölkopf B, Smola A, Williamson R, Barlett P (2000) New support vector algorithms. Neural Comput 12:1207–1245

Schölkopf B, Smola A (2001) Learning with kernels: support vector machines, regularization, optimization, and beyond. MIT press, Cambridge

Song Q, Hu W, Xie W (2002) Robust support vector machine with bullet hole image classification. IEEE Trans Syst Man Cybern C Appl Rev 32:440–448

Takeda A, Sugiyama M (2008) \(\nu \)-support vector machine as conditional value-at-risk minimization. In: Proceedings of the 25th international conference on machine learning, ACM, pp 1056–1063

Trafalis TB, Gilbert RC (2006) Robust classification and regression using support vector machines. Eur J Oper Res 173:893–909

Vapnik V (1999) The nature of statistical learning theory. Springer, Berlin

Xanthopoulos P, Guarracino MR, Pardalos PM (2013a) Robust generalized eigenvalue classifier with ellipsoidal uncertainty. Ann Oper Res 1–16

Xanthopoulos P, Pardalos PPM, Trafalis TB (2013b) Robust data mining. Springer, New York

Yang X, Tao S, Liu R, Cai M (2002) Complexity of scenario-based portfolio optimization problem with VaR objective. Int J Found Comput Sci 13:671–679

Zabarankin M, Uryasev S (2013) Statistical decision problems: selected concepts and portfolio safeguard case studies. Springer, Berlin

Zhang X (1999) Using class-center vectors to build support vector machines. In: Neural networks for signal processing IX. Proceedings of the 1999 IEEE signal processing society workshop, pp 3–11

Zhang J, Wang Y (2008) A rough margin based support vector machine. Inf Sci 178:2204–2214

Acknowledgments

We are grateful to the referees for their comments and suggestions, which helped to improve the quality of the paper. This research was supported by AFOSR Grant FA9550-11-1-0258, New Developments in Uncertainty: Linking Risk Management, Reliability, Statistics and Stochastic Optimization.

Author information

Authors and Affiliations

Corresponding author

Appendix 1: A PSG meta-code for VaR-SVM

Appendix 1: A PSG meta-code for VaR-SVM

The PSG meta-code, data, and solutions for the optimization problem (13) are available at the University of Florida Optimization Test Problems webpage,Footnote 7 see Problem 1b. For convenience, the PSG meta-code is presented below.

\(1\) Problem: problem_var_svm, type = minimize |

\(2\) objective: objective_svm |

\(3\) quadratic_matrix_quadratic(matrix_quadratic) |

\(4\) var_risk_1(0.5,matrix_prior_scenarios) |

\(5\) box_of_variables: upperbounds =1,000, lowerbounds = \(-1{,}000\) |

\(6\) Solver: VAN, precision = 6, stages = 6 |

Command minimize instructs the solver that (13) is a minimization problem, whereas objective is a declaration of the objective function stated in lines 3 and 4: commands quadratic and var_risk_1 refer to the quadratic and VaR terms in (13), respectively, and matrix_quadratic and matrix_prior_scenarios are the names of text files (*.txt) that store corresponding data matrices. The coefficients \(C\) and \(\alpha \) are set to 0.5.

Rights and permissions

About this article

Cite this article

Tsyurmasto, P., Zabarankin, M. & Uryasev, S. Value-at-risk support vector machine: stability to outliers. J Comb Optim 28, 218–232 (2014). https://doi.org/10.1007/s10878-013-9678-9

Published:

Issue Date:

DOI: https://doi.org/10.1007/s10878-013-9678-9