Abstract

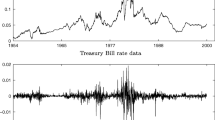

In this paper, we adapt recently developed simulation-based sequential algorithms to the problem concerning the Bayesian analysis of discretely observed diffusion processes. The estimation framework involves the introduction of m−1 latent data points between every pair of observations. Sequential MCMC methods are then used to sample the posterior distribution of the latent data and the model parameters on-line. The method is applied to the estimation of parameters in a simple stochastic volatility model (SV) of the U.S. short-term interest rate. We also provide a simulation study to validate our method, using synthetic data generated by the SV model with parameters calibrated to match weekly observations of the U.S. short-term interest rate.

Similar content being viewed by others

References

Amit Y. 1991. On rates of convergence of stochastic relaxation for Gaussian and non-Gaussian distributions. Journal of Multivariate Analysis 38: 82–99.

Andersen T.G. and Lund J. 1997. Estimating continuous-time stochastic volatility models of the short-term interest rate. Journal of Econometrics 77: 343–377.

Berzuini C., Best N.G., Gilks W.R., and Larizza C. 1997. Dynamic conditional independence models and Markov chain Monte Carlo methods. Journal of the American Statistical Association 92(440): 1403–1412.

Carpenter J., Clifford, P., and Fearnhead P. 1999. An improved particle filter for nonlinear problems. IEE Procedings—Radar, Sonar and Navigation 146: 2–7.

Chan K.C., Karolyi G.A., Longstaff F.A. and Sanders A.B. 1992. An empirical comparison of alternative models of the short-term interest. Journal of Finance 47: 1209–1228.

Chib S. and Greenberg E. 1995. Understanding the Metropolis-Hastings algorithms. The American Statistician 49: 327–335.

Chib S. and Shephard N. 2002. Comment on Numerical techniques for maximum likelihood estimation of continuous-time diffusion processes. Journal of Business and Economic Statistics 20: 279–316.

Chib S., Pitt M.K. and Shephard N. 2004. Likelihood based inference for diffusion driven models. In submission.

Del Moral P. and Jacod J. 2001. Interacting particle filtering with discrete observations. In: A. Doucet, N. de Freitas and N. Gordon (Eds.), Sequential Monte Carlo Methods in Practice. Springer Verlag.

Del Moral P., Jacod J., and Protter P. 2002. The Monte Carlo method for filtering with discrete-time observations. Probability Theory and Related Fields 120: 346–368.

Doucet A., Godsill S. and Andrieu C. 2000. On sequential Monte Carlo sampling methods for Bayesian filtering. Statistics and Computing 10: 197–208.

Durham G.B. and Gallant R.A. 2002. Numerical techniques for maximum likelihood estimation of continuous-time diffusion processes. Journal of Business and Economic Statistics 20: 279–316.

Elerian O., Chib S., and Shephard N. 2001. Likelihood inference for discretely observed nonlinear diffusions. Econometrica 69(4): 959–993.

Eraker B. 2001. MCMC analysis of diffusion models with application to finance. Journal of Business and Economic Statistics 19: 177–191.

Gamerman D. 1997. Markov Chain Monte Carlo: Stochastic Simulation for Bayesian Inference. Chapman and Hall, London, Texts in Statistical Science.

Golightly A. and Wilkinson D.J. 2005. Bayesian inference for stochastic kinetic models using a diffusion approximation. Biometrics 61(3): 781–788.

Golightly A. and Wilkinson D.J. 2006. Bayesian sequential inference for stochastic kinetic biochemical network models. Journal of Computational Biology 13(3): 838–851.

Gordon N.J., Salmond D.J., and Smith A.F.M. 1993. Novel approach to nonlinear/non-Gaussian Bayesian state estimation. IEE Proceedings-F 140: 107–113.

Handschin J.E. and Mayne D.Q. 1969. Monte Carlo techniques to estimate the conditional expectation in multi-stage non-linear filtering. Journal of Control 9: 547–559.

Johannes M.S., Poison N.G., and Stroud J.R. 2006. Optimal filtering of jump diffusions: Extracting latent states from asset prices.

Jones C. 1997. A simple Bayesian approach to the analysis of Markov diffusion processes. Technical report, The Wharton School, University of Pennsylvania.

Kim S., Shephard N., and Chib S. 1998. Stochastic volatility: Likelihood inference and comparison with ARCH models. Review of Economic Studies 65: 361–393.

Liu J. and West M. 2001. Combined parameter and state estimation in simulation-based filtering. In: A. Doucet, N. de Freitas and N. Gordon (Eds.), Sequential Monte Carlo Methods in Practice. Springer-Verlag.

Ø ksendal B. 1995. Stochastic Differential Equations: An Introduction with Applications, 6th edn. Springer-Verlag.

Papaspiliopolous O., Roberts G.O., and Skold M. 2003. Non-centered parameteri-sations for hierarchical models and data augmentation. In: J.M. Bernardo, M.J. Bayarri, J.O. Berger, A.P. Dawid, D. Heckerman, A.F.M. Smith, and M. West (Eds.), Bayesian Statistics 7, Oxford University Press, pp. 307–326.

Pedersen, A. 1995. A new approach to maximum likelihood estimation for stochastic differential equations based on discrete observations. Scandinavian Journal of Statistics 22: 55–71.

Pitt M.K. and Shephard N. 1999. Filtering via simulation: Auxiliary particle filters. Journal of the American Statistical Association 446(94): 590–599.

Roberts G.O. and Stramer O. 2001. On inference for partially observed nonlinear diffusion models using the Metropolis-Hastings algorithm. Biometrika 88(4): 603–621.

Shephard N. 2005. Are there discontinuities in financial prices?, In: A. Davison, Y. Dodge, and N. Wermuth (Eds.), Celebrating statistics: Papers in honour of Sir David Cox on his 80th birthday. Oxford University Press, pp. 213–231.

Shephard N. and Pitt M.K. 1997. Likelihood analysis of non-Gaussian measurement time series. Biometrika 84: 653–667.

Silverman B.W. 1986. Density Estimation for Statistics and Data Analysis. Chapman and Hall: London.

Stroud J.R., Poison N.G., and Muller P. 2004. Practical filtering for stochastic volatility models. In: A. Harvey, S.J. Koopman, and N. Shephard (Eds.), State Space and Unobserved Components Models. Cambridge Press, pp. 236–247.

Tanner M.A. and Wong W.H. 1987. The calculation of posterior distributions by data augmentation. Journal of the American Statistical Association 82(398): 528–540.

West M. 1993. Approximating posterior distributions by mixtures. Journal of Royal Statistical Society, Series B: Statistical Methodology 55: 409–422.

Wilkinson D.J. 2003. Disscussion to ‘Non centred parameterisations for hierarchical models and data augmentation’ by Papaspiliopoulos, Roberts and Skold. In: Bayesian Statistics 7, Oxford Science Publications, pp. 323–324.

Author information

Authors and Affiliations

Corresponding author

Rights and permissions

About this article

Cite this article

Golightly, A., Wilkinson, D.J. Bayesian sequential inference for nonlinear multivariate diffusions. Stat Comput 16, 323–338 (2006). https://doi.org/10.1007/s11222-006-9392-x

Received:

Accepted:

Issue Date:

DOI: https://doi.org/10.1007/s11222-006-9392-x