Abstract

With the enforcement of the removal system for distressed firms and the new Bankruptcy Law in China’s securities market in June 2007, the development of the bankruptcy process for firms in China is expected to create a huge impact. Therefore, identification of potential corporate distress and offering early warnings to investors, analysts, and regulators has become important. There are very distinct differences, in accounting procedures and quality of financial documents, between firms in China and those in the western world. Therefore, it may not be practical to directly apply those models or methodologies developed elsewhere to support identification of such potential distressed situations. Moreover, localized models are commonly superior to ones imported from other environments.

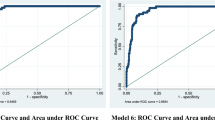

Based on the Z-score, we have developed a model called Z China score to support identification of potential distress firms in China. Our four-variable model is similar to the Z-score four-variable version, Emerging Market Scoring Model, developed in 1995. We found that our model was robust with a high accuracy. Our model has forecasting range of up to three years with 80 percent accuracy for those firms categorized as special treatment (ST); ST indicates that they are problematic firms. Applications of our model to determine a Chinese firm’s Credit Rating Equivalent are also demonstrated.

Similar content being viewed by others

References

Beaver W. Financial ratios as predictors of failure. Journal of Accounting Research, 1966, 4(suppl.): 71–111

Altman E I. Financial ratios, discriminant analysis and the prediction of corporate bankruptcy. Journal of Finance, 1968, 23(4): 189–209

Wilcox JW. A prediction of business failure using accounting data. Journal of Accounting Research, 1973, 11: 163–179

Merton R. On the pricing of corporate debt: the risk structure of interest rates. Journal of Finance, 1974, 29(2): 449–470

Corporation KMV. Introducing Credit monitor, Version 4 and the KMV EDF Credit Measure. 2000. San Francisco: KMV Corporation

Robert J, Lando D, Turnbull S. A Markov model for the term structures of credit spreads. Review of Financial studies, 1997, (10): 481–523

Altman E I. Measuring corporate bond mortality and performance. Journal of Finance, 1989, 44(4): 909–922

Asquith P, Mullins D W Jr, Woff E D. Original issue high yield bonds: aging analysis of defaults, exchanges and calls. Journal of Finance, 1989, 44(4): 923–953

Altman E I, Narayanan P. An international survey of business failure classification models. Financial Markets, Institutions and Instruments 2001, 6(2): 1–57

Dewing H S. The Financial Policy of Corporations. New York: Ronald Press, 1952

Lau A. A five-state financial distress prediction model. Journal of accounting research. 1987, 25(1): 127–138

Donaldson G. Strategy for Financial Mobility. Boston, Mass.: Harvard University Press, 1969

Newton G W. Bankruptcy and Insolvency Accounting. New York: The Ronald Press, 1975

Gilbert L R, Menon K, Schwartz K B. Predicting bankruptcy for firms in financial distress. Journal of Business Finance & Accounting, 1990, 17: 161–171

Ross S A, Westerfield RW, Jaffe J. Corporate Finance. 7th edition, McGraw-Hill Companies. 2005

Chen Q. Evidence analysis on financial distress of listing companies. Accounting Research, 1999, 4: 31–38 (in Chinese)

Chen X. Chen Z H. Corporate financial distress theory, methodology and application. Investment Study, 2000, 125–126 (in Chinese)

Zhang L. Financial distress early warning model. Quantitative and Technical Economics, 2000, (3): 49–51 (in Chinese)

Wu S, Lu X. Financial distress prediction model for chinese trading firms. Economic Research Journal., 2001, 6: 46–55 (in Chinese)

Jiang X H, Sun Z. A forecasting model of financial distress for listed companies. Forecasting, 2002, (3): 56–62

Zhang L, Chen S, Zhang X. Financial distress early warning based in MDA and ANN technique. Systems Engineering, 2005, (11): 50–58

Yang S E, Xu W G. Financial affairs in early warning model for listed companies-an empirical study on y Market’s model. China Soft Science Magazine, 2003, (1): 56–61

Chen J, Marshall B R, Zhang J. Financial distress prediction in China. Review of Pacific Basin Financial Markets and Policies, 2006, 9(2): 317–336

Hua Z, Wang Y, Xu X, Zhang B, Liang L. Predicting corporate financial distress based on integration of support vector machine and logistic regression. Expert Systems with Applications, 2007, 33(2): 434–440

Ailtman E I, Haldeman R G, Narayanan P. Zeta analysis, a new model to identify bankruptcy risk of corporations. Journal of Banking and Finance. June 1977, 29–54

Altman E I, Hotchkiss E. Corporate Financial Distress and Bankruptcy, 3rd ed., J. Wiley & Sons, England, 2005

Ministry of Finance. State Capital Share Performance Evaluation Standard. June, 1999

Shenzhen GuoTaiAn Information Technology and Tinysoft Finance Analysis Database

Basel II New Economy Accord (2004)

Author information

Authors and Affiliations

Corresponding author

Rights and permissions

About this article

Cite this article

Zhang, L., Altman, E.I. & Yen, J. Corporate financial distress diagnosis model and application in credit rating for listing firms in China. Front. Comput. Sci. China 4, 220–236 (2010). https://doi.org/10.1007/s11704-010-0505-5

Received:

Accepted:

Published:

Issue Date:

DOI: https://doi.org/10.1007/s11704-010-0505-5